Ameri credit research_report_winter_2003[1] (1)

•

1 like•1,583 views

First sell-side opinion to predict that this company would not go into bankruptcy. Discovered the true nature of the problem and prescribed the way out of the difficulty. The recovery of the company followed that path to a 'T'.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (17)

Similar to Ameri credit research_report_winter_2003[1] (1)

Similar to Ameri credit research_report_winter_2003[1] (1) (20)

More from Ned McDonnell III, CFA PMP

More from Ned McDonnell III, CFA PMP (20)

Recently uploaded

Recently uploaded (20)

Ameri credit research_report_winter_2003[1] (1)

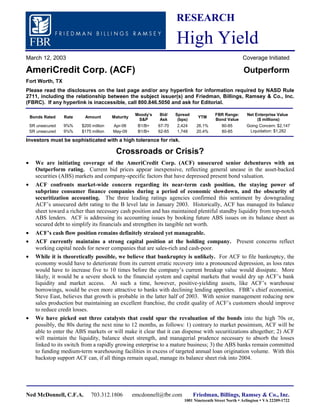

- 1. RESEARCH High Yield Ned McDonnell, C.F.A. 703.312.1806 emcdonnell@fbr.com Friedman, Billings, Ramsey & Co., Inc. 1001 Nineteenth Street North Ÿ Arlington Ÿ VA 22209-1722 March 12, 2003 Coverage Initiated AmeriCredit Corp. (ACF) Outperform Fort Worth, TX Please read the disclosures on the last page and/or any hyperlink for information required by NASD Rule 2711, including the relationship between the subject issuer(s) and Friedman, Billings, Ramsey & Co., Inc. (FBRC). If any hyperlink is inaccessible, call 800.846.5050 and ask for Editorial. Bonds Rated Rate Amount Maturity Moody’s S&P Bid/ Ask Spread (bps) YTM FBR Range: Bond Value Net Enterprise Value ($ millions) SR unsecured 9⅞% $200 million Apr-06 B1/B+ 67-70 2,424 26.1% 80-85 Going Concern: $2,147 SR unsecured 9¼% $175 million May-09 B1/B+ 62-65 1,748 20.4% 80-85 Liquidation: $1,282 Investors must be sophisticated with a high tolerance for risk. Crossroads or Crisis? • We are initiating coverage of the AmeriCredit Corp. (ACF) unsecured senior debentures with an Outperform rating. Current bid prices appear inexpensive, reflecting general unease in the asset-backed securities (ABS) markets and company-specific factors that have depressed present bond valuation. • ACF confronts market-wide concern regarding its near-term cash position, the staying power of subprime consumer finance companies during a period of economic slowdown, and the obscurity of securitization accounting. The three leading ratings agencies confirmed this sentiment by downgrading ACF’s unsecured debt rating to the B level late in January 2003. Historically, ACF has managed its balance sheet toward a richer than necessary cash position and has maintained plentiful standby liquidity from top-notch ABS lenders. ACF is addressing its accounting issues by booking future ABS issues on its balance sheet as secured debt to simplify its financials and strengthen its tangible net worth. • ACF’s cash flow position remains definitely strained yet manageable. • ACF currently maintains a strong capital position at the holding company. Present concerns reflect working capital needs for newer companies that are sales-rich and cash-poor. • While it is theoretically possible, we believe that bankruptcy is unlikely. For ACF to file bankruptcy, the economy would have to deteriorate from its current erratic recovery into a pronounced depression, as loss rates would have to increase five to 10 times before the company’s current breakup value would dissipate. More likely, it would be a severe shock to the financial system and capital markets that would dry up ACF’s bank liquidity and market access. At such a time, however, positive-yielding assets, like ACF’s warehouse borrowings, would be even more attractive to banks with declining lending appetites. FBR’s chief economist, Steve East, believes that growth is probable in the latter half of 2003. With senior management reducing new sales production but maintaining an excellent franchise, the credit quality of ACF’s customers should improve to reduce credit losses. • We have picked out three catalysts that could spur the revaluation of the bonds into the high 70s or, possibly, the 80s during the next nine to 12 months, as follows: 1) contrary to market pessimism, ACF will be able to enter the ABS markets or will make it clear that it can dispense with securitizations altogether; 2) ACF will maintain the liquidity, balance sheet strength, and managerial prudence necessary to absorb the losses linked to its switch from a rapidly growing enterprise to a mature business; 3) the ABS banks remain committed to funding medium-term warehousing facilities in excess of targeted annual loan origination volume. With this backstop support ACF can, if all things remain equal, manage its balance sheet risk into 2004.

- 2. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 2 Table of Contents Investment Thesis......................................................................................................................................................... 3 Catalysts for Repricing into the High 70s or 80s ......................................................................................................... 3 Company Description and Strategy.............................................................................................................................. 5 Recent History.............................................................................................................................................................. 5 Competition.................................................................................................................................................................. 7 Management................................................................................................................................................................. 8 Balance Sheet/Solvency Analysis ................................................................................................................................ 8 Investment Risks and Mitigants ................................................................................................................................. 11 Conclusion: Placing ACF’s Liquidity Hurdle into a Larger Perspective of Securitization Cash Flows.................... 14 Appendix I.................................................................................................................................................................. 16 Appendix I, Attachment A ......................................................................................................................................... 20 Appendix I, Attachment B.......................................................................................................................................... 21 Appendix I, Attachment C.......................................................................................................................................... 22 Appendix I, Attachment D ......................................................................................................................................... 23 Appendix I, Attachment E.......................................................................................................................................... 24 Financial Data............................................................................................................................................................. 25 Appendix II, Attachment A........................................................................................................................................ 26 Appendix II, Attachment B ........................................................................................................................................ 27 ¹ Note: this high yield analysis is conducted independently of ACF’s equity analysis issued by FBR’s equity analyst. FBR acted as the lead placement bank in ACF’s $500 million equity offering on September 26, 2002. For added insight, please refer to the recent opinion released by FBR equity analyst, Todd Pitsinger. Mr. Pitsinger’s stock analysis properly views ACF as a going concern with opportunities to accrue added value to stockholders. Any variance in the tone of these reports lies in their differing objectives and not in divergent opinions of ACF. Company Description ACF is a leading financier of automobiles, with a focus on the subprime sector. The company has over 250 branches and originates loans that transact directly and primarily with used car dealers. In 10 years of operation, ACF has built a customer base that exceeds 1 million people in the U.S. and Canada. By targeting consumers with checkered credit histories and utilizing risk-adjusted pricing, ACF has earned net interest margins of 12% against collateral that retains resale value over time. Furthermore, most individuals will default on everything else before their car loans (except for their home loans), providing ACF with a relatively stable customer base. Most of the company’s funding comes through the asset-backed securities market, as ACF factors loans with an average balance of $16,000 through to the capital markets. ACF successfully raised $500 million in an FBR-led equity offering in late September 2002. FBR’s equity analyst assigns an Outperform rating to the common stock.¹

- 3. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 3 Investment Thesis We are initiating coverage of ACF’s publicly issued, unsecured senior debentures with an Outperform rating. We believe that cash redundancies embedded in the balance sheet, in addition to the longer-term sustainability of the company’s new, steady-state strategy, enable ACF to make bond investors whole either in liquidation or as an ongoing concern. With collateral recovery values declining and the economy not yet growing consistently, ACF has taken the following steps to protect its bondholders: • In September 2002, FBR placed $500 million of fresh equity for ACF. • ACF is ramping up initial collateral margins to 2x to 3x the historical annual net charge-off rate and is reducing the lag time between an ABS issuance and the company’s receipt of excess cash flows by two- thirds. • The company is in discussions with AA- and AAA-rated bond insurers in an effort to reduce funding costs and maintain its access to the capital markets. • ACF is making its financial statements more transparent by booking new securitizations as secured loans on the balance sheet, as opposed to accounting for them as “sales” to single-purpose/off-balance-sheet entities (SPEs). • Requirements for new loan approvals are tightening as a result of the declining credit performance of ACF’s target market and the reduced loan origination capacity imposed by stricter credit enhancements on securitizations. ACF has announced that it will reduce loan production by 67%, from $9 billion to $3 billion per year, effective immediately (please refer to Appendix I, Attachments A–E, for a primer on ABS mechanics as they relate to ACF). Catalysts for Repricing into the High 70s or 80s ACF recently announced that Financial Security Assurance, Inc. (FSA), its lead credit support provider, will not insure any more ABS issues, at least in 2003. Market sentiment indicates a lack of confidence in ACF’s ability to bring a securitization to the ABS market. We differ with this view for three reasons. First, FSA’s decision appears to be related more to business pressures elsewhere (primarily related to its parent and FSA’s reinsurers) than to credit-quality concerns at ACF. FSA has not revoked the strong statement of support that it gave to ACF in September 2002. We believe that FSA would do so if ACF were really in trouble in order to avoid potential liabilities related to what might be construed in court as a misleading statement, particularly to reinsurers that provide support to FSA on the ACF policies. Second, ACF revised its collateral structure from 3% upfront and 9% deferred over 12 to 18 months to 10% upfront and 5% or 6% deferred over six months. ACF did have a reason to change its collateral structure for the second time in four months; the $1.7 billion MBIA- insured transaction of October 2002 was a one-off structure with the entire 12% upfront. We believe that this newest structure is what key stakeholders—the ABS banks, the ratings agencies, and/or prospective bond insurers—require to market an ABS issue. From the standpoint of ABS investors, such a structure make sense. If the company must wait six months before collecting any excess spread, ACF will be less inclined toward relaxing credit standards, thereby leaving an underperforming portfolio to the ABS investors in order to generate immediate fee income. Third, we estimate that ACF’s operating liquidity hurdle falls within the $50 million to $75 million range. While this amount is noticeable in light of the company’s recent equity issue, we believe that it is manageable, especially with cash flow already ACF has maintained the liquidity, balance sheet strength, and managerial prudence necessary to absorb the losses linked to its switch in operating strategy and its accounting clarification. Contrary to market pessimism, ACF will be able to enter into the ABS markets or will make it clear that it can dispense with securitizations for the time being.

- 4. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 4 accruing from the October 2002 MBIA transaction. In our view, the recent $45 million net loss for the second quarter of FY(Jun)03 and ACF’s candid view of the business environment for 2003 do not anticipate insolvency. By booking securitizations as secured debt, ACF will demonstrate the capacity of its balance sheet to absorb external shocks. This accounting transparency, as well as ACF’s larger initial collateral contributions, should increase the company’s medium-term/long-term financial flexibility. Strict, seemingly onerous protections imposed by the ABS banks and by FSA confer a spillover benefit upon bondholders. ACF likely had no choice in submitting to these restrictions, but it has made a virtue of necessity. Other subprime lenders have lapsed into a death spiral of declining asset quality and ebbing liquidity, both accelerated and obscured by gain-on-sale accounting. Its lasting prudence has provided ACF with some resiliency to the economic cycle. ACF’s operating and bank liquidity remain solid, notwithstanding recent losses. ACF has also secured bank lines that exceed $5 billion ($1.8 billion outstanding) from liquidity banks, led by Merrill Lynch & Co., Deutsche Bank AG, Crédit Suisse First Boston LLC, J.P. Morgan Chase & Co., and Barclays Group, plc. ACF will trim these lines to $3.4 billion, primarily in the fourth quarter of 2003; none of the lines rolling off have borrowings outstanding. The remaining lines of $3,415 million are committed until June 2004 (22%), February 2005 (18%), and March 2005 (63%). ACF’s reduction in bank lines will follow from its nonrenewal of a short-term line. In truth, however, the bank involved will welcome the termination, notwithstanding the current confidence expressed by its peers. These lines cannot be terminated after their usual six-month borrowing period, according to ACF’s management. Instead, an amortization period begins, and the ABS banks, in effect, become the owners of a privately placed ABS issue; there is no acceleration of principal payments. Because these lines are likely to be distributed to participants of banking syndicates and because any automatically amortizing loans can be placed in off-balance-sheet investment vehicles sponsored by these banks, the terming out of a warehouse loan does not present an undue burden for ACF’s banks. Additionally, the company remains in compliance with its financial covenants. Should ACF term out its warehouse loans, or if economic conditions remain inhospitable, ACF will have to wind down operations in an orderly runoff of the existing portfolio, perhaps in receivership. Because ACF would continue to earn interest from the loans still being repaid throughout the runoff period, we calculate a runoff value of $1.3 billion by discounting after-tax cash flows (we discuss these results fully below). Finally, we calculate a company-based enterprise value of $2.15 billion, based on management guidance given during a conference call in mid February 2003 and on ACF’s historical performance (we cite specific assumptions in the section below that discusses enterprise value). The discount rate applied to these cash flows exerts, by far, the most influence over the enterprise or eventual bond resale values. Specifically, we apply the following discount rates in our scenarios: • 11.5% for the ACF base case/enterprise value, or the average yield (to maturity) for B-rated bonds in the Goldman Sachs high yield index, as listed in the March 4, 2003, edition of the Prospect News High Yield Daily. • 16.5% for the runoff/liquidation scenario, or the approximate midpoint between the discount rates implied by the weighted average yields for B-rated and CCC-rated bonds in the Goldman Sachs index. The blended B/CCC “FBR discount rate” is roughly 10 percentage points above the yields to maturity for the BBB-rated bonds of similar maturities issued by GMAC and Ford Motor Credit. As long as commercial and investment banks remain committed to funding term warehousing lines, ACF can manage its balance sheet risk into 2004.

- 5. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 5 Company Description and Strategy ACF has historically been a monoline auto financier. Over its decade of active business, ACF has assumed leadership in the U.S. independent subprime automobile loan market and has built a customer base that exceeds 1 million people. The company has approximately 20,000 distribution points throughout the U.S. and Canada. The FICO scores (credit scores compiled by Fair, Isaacs & Company) of ACF’s customers lie squarely within the subprime category. A quoting protocol through the “Dealer-Track” system—an online service pioneered by ACF—enables car dealers to submit an application for a customer’s loan and receive a response quickly. Such responsiveness has established firm distribution relationships. ACF’s simple, effective strategy is as follows: 1) to penetrate the market and choose a better than average risk pool, 2) to earn a rich spread on the loans to absorb higher loss rates from subprime borrowers, and 3) to distribute the product efficiently. ACF has executed this strategy successfully, as detailed by performance data in the chart below. Historical Summary: June 2000 through December 2002 Relative to Managed Assets Last 12 months FY(Jun)02 FY(Jun)01 FY(Jun)00 Originations (average life of 2¼ years) $9.2 billion $8.9 billion $6.4 million $4.4 billion Pretax income (incl. securitization gains) $375 million $565 million $362 million $190 million Average loan balance* (*as of Sep 2002) $13,224* $13,129 $12,384 $11,706 Number of contracts outstanding* 1,190,830* 1,124,388 823,919 568,099 Number of dealers N.A. 19,401 16,280 14,076 Number of sales offices N.A. 251 232 196 Number of employees 20% being laid off 5,250 4,392 3,048 Net interest margin, pre-credit losses 12.5% 12.3% 12.0% 12.0% Net charge-offs 5.4% 4.6% 4.3% 4.0% Expense ratio 3.1% 3.4% 3.7% 4.2% Dollar origination volume per dealer N.A. $460,234 $391,830 $314,578 Approximate loans executed per sales office* 1,058 loans* 1,197 loans 1,102 loans 1,030 loans Source: Company financials Recent History On January 17, 2003, and on February 13, 2003, ACF released disappointing financial results for the December 2002 quarter. Its quarterly loss of $45 million, or ($0.20) per share, was worse than expected and followed declining performance during the preceding quarter. Operating ratios deteriorated across the board, with annualized net charge-offs reaching as high as 5.8% (6.5% including repossessed but unsold cars) or a full percentage point above average years. Falling recovery rates on the repossessed cars increased these credit losses. The stock price fell from a range of $7 to $8 per share, already historically low levels, to a level below $2 per share. Short interest is high at 22.9 million shares (16.3% of the public float), yet it has improved by one- third from late 2002. More than a dozen class action lawsuits have been filed against the company and its senior management for allegedly misleading investors. The pattern seems frighteningly familiar in its resemblance to recent insolvencies of leveraged subprime lenders. However, ACF’s case is fundamentally different. While rising income figures per employee might suggest that revenues and earnings were inflated in the short-run due to lax credit standards, we do not endorse the viewpoint that ACF faces an asset-quality crisis for the reasons discussed below.

- 6. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 6 • ACF had already announced its intention to change its business culture from that of a high-growth revenue producer to that of a mature institution disciplined in its expense and credit management. On February 13, 2003, management detailed a plan for this change in strategy: 1. Reduce annual originations by two-thirds to $3 billion and close 60% of the sales offices, leaving only 92 in place. 2. Terminate unprofitable relationships with used car dealers that are responsible for disproportionately high levels of credit losses. 3. Take a $40 million to $50 million one-time charge in 2003 to expense severance costs that will be paid over the next six to 12 months. 4. Ratchet up the average consumer FICO scores to the near-prime level of 650 to 660, versus current levels that are below 600 (with prime starting at 720). • In the past, ACF has operated at GAAP profitability of breakeven or better, excluding the distortions of gain-on-sale accounting, which is better than average for consumer credit companies reliant upon securitization. • Current GAAP profitability is flagging, but the company is operating at a break-even level for the quarter, excluding noncash write-downs of securitization residuals. • The company’s 12-month net interest income was up 17% to $237 million as of December 2002 (versus $203 million as of FY(Jun)02), with quarterly revenues increasing 30% year over year. • While operating cash flows recently turned negative, exceeding ($50 million) for the December 2002 quarter, ACF has still generated over $500 million in positive operating cash flows over the last 12 months. (Please note that we reclassify loan originations and repayments as investment cash flows and almost all securitization cash flows as financing.) • In September 2002, FBR placed a $500 million issue of fresh equity for ACF. • By applying at least 45% of the equity proceeds toward ABS collateral, ACF has doubled the amount of free cash on its balance sheet, largely through a one-off MBIA-insured ABS issue of $1.7 billion in October 2002, in which the company posted the 12% required collateral upfront in order to collect excess spreads immediately. Below, we plot out the historical timeline of the 9⅞% bond and ACF’s common stock over the past 18 months, detailing what we believe were the turning points in the value of ACF. The values of both securities have dropped noticeably in recent weeks. Nonetheless, we view the adversity confronting ACF’s investors largely as a consequence of a bear market, the growing distrust of corporate practices (especially the use of special- purpose/bankruptcy-remote entities willfully to understate debt), and popular disgust with the predatory lending practices of certain consumer finance companies (not ACF). Additionally, an erratic economic recovery threatens a double-dip recession, which would hurt the type of consumer that fits ACF’s customer profile.

- 7. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 7 Source: Bloomberg and ACF statements Competition Although having a narrow product mix as a consumer finance company that pursues people with average (or below-average) credit histories has imposed its burdens in recent months, ACF has carved out a defensible niche as the largest independent “middle-market” (a.k.a. subprime) auto financier in the U.S., with growing operations in Canada. ACF has emerged as a survivor in a sector marked by challenges for new entrants (e.g., Capital One) as well as by difficulties for direct competitors (e.g., Union Acceptance Corp.). Below, we present a peer review in which ACF compares satisfactorily with other subprime lenders in overall profitability. S&P downgraded ACF’s senior debt to B+/negative on January 29, 2003, following a two-notch downgrade by Fitch to the same level on January 30, 2003, and a “ditto” by Moody’s on January 31, 2003. The ratings agencies cited the decline in consumer credit quality and the slippage in automobile resale values as catalysts for their downgrades. In its downgrade notice, Fitch expressed a timely concern about the possibility of imminent covenant violations under the credit agreements. It is quite possible, even likely, that some ratio covenants will be violated. Fortunately, ACF’s ABS banks are deeply versed in ABS mechanics and will view such technical, nonpayment defaults as a way to get management to provide the banks with the full story. In fact, these banks have indicated their ongoing support of ACF. While these sentiments are nothing new, the urgency cited by Fitch—largely considered as the best versed among the ratings agencies on ABS issues—is disturbing in that it could influence the actions of already-anxious creditors toward ACF. U.S. personal bankruptcies remain at all-time-high levels—1.6 million cases for an 8% increase over the past year alone. Further, the Manheim Index (named for the largest auctioneer of repossessed automobiles), a measure of the firmness of used car prices, is bumping along at its weakest level in two years, implying a 12% depreciation in used car pricing. Recent leveling off of that index may indicate that the price $0 $20 $40 $60 $80 $100 $120 ACF’s Historical Stock/Bond Pricing Performance for the Past 18 Months New Year’s Day 2002 FBR-led issue clears at $7.50 on 9/26/02 8/02: Union Acceptance & Conseco start their final death spirals with downgrades and lock- outs from ABS mkts. So, who’s next? 1/17/03, 2/13/03: ACF’s 2nd qtr loss. Will FSA stay or go away? 4/26/02; Consumer confidence up; high point of the rally that really wasn’t…yet $62.31 @ 10-Aug-01 stock price $2.50 11-Sep-01 3/11/02; ACF announces Deutsche committed warehousing syndicate; 25% increase to $4.9 billion; 2/3 greater than 1 year bid of 57 9/16/02: PRIOR to imminent equity issue, ACF announces relaxed trigger points on FSA- insured ABS issues; ACF also cuts profits Bid of 9⅞ Bid of 106 7/02; Capital One, Metris, & PNC each hassled by regulators over SPEs or subprime loans; wariness toward securitizing banks. 6/02; $300 million bond issue under- subscribed by 40%

- 8. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 8 slippage for used cars is slowing. Nonetheless, the “firming levels” of the index (currently at 104) remain well below those of the peak in 2000. A larger factor is the willingness of large automakers to continue deflationary product pricing through subsidized auto financing and rebate packages. Trailing 12 months S&P / Stk Pr.-to- Managed Total Net Net Int. Net Charge-off 30+ day Debt-to- Company ($million) Moody's Book Val. Assets Debt Worth EBIDTA Margin Income Rate (net) Delinq. EBIDTA RoE AmeriCredit B+/Ba3 0.1 $18,545 $3,991 $1,917 $408 12.5% $232 5.8% 14.7% 9.8 12.1% Peer Group Average BBB / A- 3.0 $72,845 $43,415 $4,441 $5,639 6.2% $372 2.2% 3.1% 7.7 9.7% MEDIAN BB- / Ba3 0.9 $11,147 $4,099 $864 $683 8.6% $54 10.6% 7.2% 5.6x 8.4% G.M.A.C. BBB / A2 3.3 $283,881 $170,066 $17,492 $17,159 5.8% $1,781 0.8% 4.0% 9.9 10.2% Ford Credit BBB / A3 3.3 $245,086 $153,728 $13,600 $23,081 5.1% $1,234 1.5% 0.7% 6.7 9.1% Providian BB- / Ba2 0.9 $27,170 $14,129 $2,131 $3,226 14.7% ($173) 14.7% 11.1% 4.4 N.M. Metris B / B3 0.1 $12,138 $1,455 $1,114 $594 16.0% $86 15.9% 9.9% 2.4 7.7% WFS Financial BB- / B1 1.2 $10,156 $6,743 $613 $771 6.4% $77 2.5% 3.7% 8.7 12.6% Union Acceptance Ch-11 0.2 $2,647 $568 $112 $30 4.2% ($63) 6.4% 4.5% 18.9 N.M. C.A.C.C. N.R. / Ba3 0.8 $987 $134 $318 $47 10.7% $31 15.8% 23.4% 2.9 9.7% Ugly Duckling CCC / N.R. N.A. $695 $494 $151 $200 20.2% ($1) 25.9% 34.5% 2.5 N.M. Note: the delinquency percentage for AmeriCredit includes automobiles repossessed of 1.4% as of December 2002. Source: Publicly filed SEC statements and Bloomberg Critics voice a valid concern by observing that ACF’s chosen arena of automobile financing is dominated by “six-hundred-pound gorillas” that act more like loss-leading marketing arms of manufacturing enterprises. The large balance sheets of Ford Credit and GMAC overshadow ACF’s sustained performance in a targeted segment eschewed by the two leaders. On the other hand, were the auto company financiers merely the marketing primates from Detroit, their asset quality ratios would likely be worse than those reported above. We also note that ACF’s debt-to-EBITDA ratio is exaggerated by the inclusion of securitizations booked on the balance sheet as debt. The removal of these liabilities from debt reduces the ratio to approximately 5x; senior unsecured debt- to-EBITDA for ACF has been as low as 1.5x. ACF’s balance sheet leverage—i.e., holding company debt to net worth of 23%—compares favorably to that of its peers—WFS (75%–80%), Providian (51%), Ford Credit (estimated at 42%), Metris (31%), and Credit Acceptance (30%). Management ACF’s management has been present throughout its 10-year operating history and is as follows: Clifton H. Morris, Jr. Michael R. Barrington Chairman President and CEO Founder; handed over presidency in 1991 and CEO position in 2001 Vice chairman; joined ACF in 1991 Daniel E. Berce Edward H. Esstman Chief financial officer Chief operating officer Vice chairman; joined ACF in 1990 Vice chairman; joined ACF in 1992 Balance Sheet/Solvency Analysis Enterprise Value (i.e., as a going concern) Below, we present the summary findings of our view of ACF’s projections. Whenever possible, we have applied the assumptions verbatim from ACF’s February 13, 2003, conference call. Otherwise, we have assumed a gradual reversion to ACF’s historical averages. Specifically, these company assumptions are as follows: a) a reduction of loan originations to $3.5 billion in 2003, b) a cap on originations at $3 billion in out-years, c) the expensing of $40 million in severance costs (i.e., the lower bound) in 2003, d) the trapping of $140 million in cash on the FSA transactions, e) the restoration of credit experience and recovery rates to historical levels over the next four to five years, f) the reduction of the expense ratio (to loans serviced) by 30%, g) the securitization of 80% of originations through the ABS market, and h) the posting of $25 million additional collateral due on derivatives transactions, as well as on losses on cancelled trades due to ACF’s recent downgrades. From this

- 9. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 9 forecast, reconfigured on a calendar-year basis (versus the June fiscal year normally presented), we calculate ACF’s enterprise value of $1.7 billion. Because we are discounting after-tax cash flows, we do not subtract the $450 million of holding company debt from the enterprise value. ACF Base Case $2.15 Billion Enterprise Value Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Previous Year-End Gross Receivables $16,209 $13,674 $10,510 $7,726 $5,811 $5,542 $6,730 New Loans Booked During Year $3,500 $3,000 $3,000 $3,000 $3,000 $3,000 $3,000 Growth Rate -61.8% -14.3% 0.0% 0.0% 0.0% 0.0% 0.0% Managed Receivables; Year-End $13,674 $10,510 $7,726 $5,811 $5,542 $6,730 $8,917 Attrition $4,951 $5,436 $5,301 $4,563 $2,980 $1,506 $432 Net Charge-Offs $1,084 $728 $484 $352 $289 $306 $381 Managed Receivables; Year-End $13,674 $10,510 $7,726 $5,811 $5,542 $6,730 $8,917 Holding Company Cash Balance $232 $128 $698 $737 $1,019 $1,230 $1,062 Delinquency Rate 12.1% 11.0% 10.4% 10.3% 10.5% 10.7% 11.6% Gross Charge-off Rate 11.4% 9.7% 8.7% 8.7% 8.7% 8.7% 8.7% Recovery Rate 36.6% 37.7% 38.9% 40.0% 41.2% 42.5% 43.7% Net Charge-offs % of Recbles 7.3% 6.0% 5.3% 5.2% 5.1% 5.0% 4.9% Cumulative Loss Rate 8.9% 10.3% 10.8% 11.8% 12.3% 12.9% 13.6% Interest Coverage Managed 2.61 2.09 3.29 3.75 3.78 3.72 3.19 Net Interest Margin 9.6% 9.6% 10.0% 10.3% 9.0% 9.1% 9.2% Owned Income Statement Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 REVENUES $645 $736 $438 $442 $332 $227 $186 Net Income ($161) $240 $104 $136 $95 $25 $20 Operating Cash Flow/Managed $16 $608 $276 $299 $229 $24 ($70) Terminal Value: Release of O/C into Income $2,325 Year-End Debt $450 $375 $375 $175 $175 $175 $0 SR debt revalued at the FBR discount rate: of 16.5% = 80-89 range SR debt revalued at the Goldman Index "CCC" rate (Mar-03) of 21.2% = 70-82 range SR debt revalued at the "B" risk-adjusted bank capital charge of 33% = 51-69 range Source: Company financials ACF expects to recover approximately half of this trapped or lost cash in 2004. We also forecast results through December 2009, the scheduled maturity of the 9¼% bonds. This enterprise value is not a liquidation value because its underlying premise is that ACF will continue its operations. We have calculated separate liquidation values on a breakup and runoff basis. The breakup scenario examines the balance sheet as reported at December 2002 and assigns breakup values to the various asset classes, estimating an amount for which each could be sold immediately. Valuing the Balance Sheet Versus Runoff Liquidation Values Balance sheet, or “breakup,” valuations tend to be conservative because the haircuts applied to assets embody “worst-case” assumptions, such as loss rates at multiples of past levels or little, if any, recovery values. These worst-case assumptions often reflect the belief that the assets of financial institutions tend to be unavailable when one needs them the most. Below, we present a comparison of two valuations, one based on the balance sheet and one based on runoff values. We begin with a line-by-line asset revaluation of ACF’s “owned” balance sheet. The owned balance sheet excludes those receivables securitized off the balance sheet; this amount is small compared to the total assets managed. All things being equal, the owned balance sheet of a specialty finance company that is active in the ABS market is not terribly important, as what is off the balance sheet really determines what one sees on it. Presently, however, all things are not equal; ACF’s stock trades under $2 per share, and the pricing of the bonds is drifting toward prebankruptcy levels. Should ACF collapse financially— again, an outcome we consider to be highly unlikely—the company’s creditors will only have recourse to the owned balance sheet.

- 10. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 10 Assets: Actual Reconciliation / Comment Liquidation Cash & liquid investments $216 excess spread from MBIA ABS issue $250 Automobile Finance Receivables $3,998.0 offsets debt dollar for dollar netted vs LESS : Reserve for Credit Losses ($218.0) ignored for cash valuation liabilities Interest-Only Bond (ABS excess cash-flow) $357 10% loss / 36% recovery; after-tax $114 Invts in Trust Receivables (ABS dfd collateral) $791.0 losses 1st vs I/O then cash then invts $791 Restricted Cash (supporting securitizations) $414.0 near-cash / protected $414 Restricted Cash (ABS warehouse sinking fund) $267 net amount of earning assets left $267 PP&E / Other Owned Assets $465 real property, net of synthetic lease $87 $6,290 $1,923 Liabilities: Funding Payable & Other Liabilities $407 accrued taxes + 1.5% expense rate $209 Warehouse Line $1,750 netted Senior Notes $380 par value $380 Other Notes $70 par value $70 Securitization Notes (non-recourse) $1,792 netted Shareholder's Equity $1,891 Net Asset Value $1,264 NOTE: Managed Receivables total $16 billion $8.26/share NOTE: Value derived from discounted cash-flow projections of liquidation: $1.3 billion; $8.68 per share. Market Cap's ($) / Price-to-Book Value (x) $243 million / 0.13x Cash-flow based entreprise value of $2 billion. Balance Sheet; Liquidation Value NOTE: U.S.$millions, except per share amounts Source: Company financials On the other hand, a runoff value represents a liquidation that is permitted over time and in an orderly manner as loan balances pay down. The runoff is the usual path to liquidation for financial institutions, (for example, Finova Capital Corp., Reliance Group Holdings, Inc., and Comdisco, Inc.) since they are ordinarily liquidated in receivership. The runoff permits a revaluation of expected cash flows in the repricing of assets. When analysts view the credit enhancement assets as “near cash,” they are referring to a runoff scenario, specifically to collateral technically owned by ACF but controlled by the ABS Trustee or FSA until repayment of the corresponding receivables. In our separate runoff scenario, ACF winds down its book of business in adverse market conditions but pares back its expense ratio by 60% since it does not engage in any new business development. If after-tax cash flows are discounted at 16.5%, this would generate a separate liquidation value of $1.3 billion. The relative proximity of the balance sheet value to the runoff liquidation value ($1,264 million versus $1,282 million) increases our confidence in the veracity of ACF’s financial statements and in the stable values of the interest-only security (I/O) and credit-enhancement assets. Further, these results arguably support the assertion that the securitization assets on the owned balance sheet are indeed “near cash” assets. Although the convergence inevitably reflects our familiarity with those financials, we have calculated these values independently. (Please refer to Appendix II, Attachment B for the complete runoff projections.)

- 11. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 11 $1,282 million FBR liquidation value Dec-03 Dec-04 Dec-05 Dec-06 Previous year-end Gross Receivables $16,209 $11,712 $5,602 $235 New Loans booked during Year $1,466 $0 $0 $0 Attrition $4,951 $5,579 $5,207 $235 Net Charge-offs $1,013 $531 $161 $6 Managed Receivables; year-end $11,712 $5,602 $235 $0 Holding Company cash balance $306 $74 $217 $158 Delinquency Rate 14.0% 18.2% 7.7% 3.7% Gross Charge-off Rate 11.3% 9.5% 8.5% 8.3% Recovery Rate 35.6% 35.6% 35.6% 35.6% Net Charge-offs % of Recbles 7.3% 6.1% 5.5% 5.4% Cumulative Loss Rate 9.3% 11.2% 11.8% 11.8% Financing Rate 17.30% 17.30% 17.30% 17.30% Net Interest Margin 9.5% 9.7% 11.3% N.M. Interest Coverage Managed 1.54 1.48 1.36 N.M. REVENUES $1,472 $915 $279 $114 Net Income $455 $476 $140 $50 Operating cash flow / managed ($88) $253 ($118) ($92) Releases from Cash Collateral Accounts $25 $0 $50 $28 Terminal Value: Release of O/C into income $1,485 Principal Payments $200 $150 $100 $0 Year-end debt $250 $100 $0 $0 Source: Company financials Investment Risks and Mitigants External Factors • The insecure recovery may slip back into recession; so little money, so little time. The current recession is already two years old, despite the occasional firming of economic indicators. It has been brutal, even deflationary, for the working class, ACF’s primary market. Personal bankruptcies and defaults remain high, and Americans carry a heavier credit load than at almost any other time in history. Although auto payments are among the last on which consumers default, ACF’s borrowers may be too far behind on other obligations for delinquencies to turn around quickly. Accordingly, ACF’s problem loan rates remain roughly 25% above historical levels, with delinquencies of 30 days or more approaching 15% and with loan deferrals extended to more than 20% of the active accounts. When permitted in a disciplined manner, such deferrals can reduce default rates and subsequent losses. Mitigants include: 1) No commitments to lend, and very few previously approved but unfunded loans to customers, permitting immediate extrication into liquidation. 2) Clear-cut eligibility parameters on 30-day loan deferments to avoid understatement of delinquencies to reduce loss rates by 50% to 60%. 3) An equity issue netting $480 million of cash to support loss reserves for the ABS issues and new business. 4) More than $3 billion of bank warehousing capacity in place for two years. 5) A superior market franchise that still produced $2 billion of loans during the turbulent December 2002 quarter. • Downgrades and lawsuits may accelerate investor overreaction into panic; appearances may become reality as guilt by association could hurt credibility. “Securitization” and “special purpose entity” now have negative connotations, and these words have historically been associated with ACF. We believe that the market’s wariness toward institutions that rely upon securitizations—following negative press related to Enron Corp., Dynegy, Inc., PNC Bank Corp., Conseco, Inc., J.P. Morgan/Chase Corp., and Citicorp—has

- 12. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 12 spilled over onto ACF. Thus, the criticism and shareholder class action lawsuits that are weighing on ACF obscure its break-even operating performance for the December 2002 (second) quarter. Mitigants include: 1) The increased transparency of securitization accounting to clarify the depth of ACF’s cash redundancy. 2) A balance sheet that is already improving, with ACF’s tangible net worth already stronger than that of most credit card issuers. 3) ACF’s visible commitment to cost efficiency, as proven by recently announced staff reductions (20% of headcount; 60% of the sales offices) and facilitated by lower volumes of loan originations, presumably to higher-quality customers. 4) Little market reaction, initially reflected in an unchanged stock price, subsequent to the one-notch S&P downgrade and the two-notch Fitch & Moody’s downgrades in ACF’s debt ratings to the same level of B+ and B1/negative. • War may be less. A U.S.-led attack against Iraq could exert a downward supply shock on global oil production, which would elevate gas prices quickly. Many lower-income consumers with tight budgets would face increased financial pressures. Compounding these increasing expenses, subsequent wage deflation or outright unemployment for lower-skilled manufacturing jobs could accelerate expected deterioration in credit performance. Mitigants include: 1) Restraints on new business development, supplemented by stricter lending standards in the future. 2) Plans to increase selectivity of new accounts. • Dependence upon outside credit support providers. ACF recently announced that FSA will not provide financial guaranty policies for any securitizations, presumably for the remainder of 2003. Since FSA publicly expressed its confidence in ACF and its management in September 2002 (i.e., at the time that it waived the triggers for cash-trapping under its issued insurance policies) and since FSA has not rescinded the vote of confidence, we suspect that FSA’s decision lies in factors other than ACF and its current challenges. FSA’s parent, Dexia, S.A., is laboring under adverse publicity and a €4.5 billion lawsuit in Europe related to a selling scandal. FSA’s exposure to ACF had been mentioned in public criticisms of Dexia. Additionally, FSA’s reinsurers on the ACF policies have mounted pressure on the bond insurer to back away from insuring future ACF transactions until credit performance shows sustained improvement. Mitigants include: 1) The recent decision to fund two-thirds of the excess collateral reserves upfront and to cut the deferral period from 18 months to six months prior to receiving excess ABS cash flows receipts. 2) Two ABS series in the past year that total $1.2 billion without the aid of external credit support. 3) MBIA’s recent backing of a $1.7 billion ABS issue, with a one-off 12% deposit structure, to reduce funding costs and throw off much-needed short-term cash. 4) Strong risk-adjusted net interest margins over time, indicative of consistent risk/collateral management. 5) ACF’s vigilance against slackening credit safeguards, as mandated by FSA, MBIA, the ABS banks, and the ratings agencies through ongoing covenant compliance, cross-collateralization, and continual due diligence. Internal Factors • A holding company’s financial leverage and liquidity are concerns for most financial institutions, particularly those chasing subprime retail borrowers. Mitigants include: 1) EBIDTA for the past 12 (recessionary) months, exceeding the amount of the debentures under review. 2) The absence of bank subsidiaries at ACF, which could diminish the importance of regulatory risk.

- 13. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 13 3) EBIDTA annualized from the infamous December 2002 quarter may be able to service the senior debt in two years. • Collateral resale values are declining with a glut of new car supplies. Consumers are trading in relatively new models to auto dealers and availing themselves of new autos financed with 0% or deferred payment loans. These rates and other enticements reduce sticker prices by 10% or more. Such deflationary new product pricing will probably constrain recovery rates for at least the next year, as resale prices are already down by one-third in six months. Management states openly that they are restructuring the company’s risk-scoring model to account for this unanticipated cyclicality in resale values with that of a choppy, unstable recovery. Mitigants include: 1) Softening new car sales in January and February, possibly implying that a reduction of the used car glut from trade-ins will follow over the next few months. 2) Tentative firming of a popular used car pricing index. 3) Enhanced credit selection to reduce the number of defaults and diminish the importance of recovery values. 4) All other (presently painful) things being equal, a company runoff value of $519 million if recovery rates drop to ZERO. • The willful neglect of business practices and accounting standards (in other words, the last-resort measures of companies sliding toward insolvency) is not a concern in view of management’s consistent integrity in facing adverse conditions in the past. One area that we have examined over time has been that of deferred loans. Troubled specialty finance companies, often those with a history of securitization, have used loan deferments to hide asset quality problems. In past years, ACF has managed temporary cash flow problems of (ordinarily) better-paying clients by allowing one, or perhaps two, monthly payments to be deferred over a given year. This program has been beneficial both to the company and to its customers. ACF’s use of deferrals was negligible until five years ago when the percentage of customers for whom the company deferred a loan payment for one month spiked up to 4% per quarter. For the December 2002 quarter, deferrals were 5.5%, or 22% on an annualized basis. Fitch reports that at least one bank has tightened its covenant on the amount of deferrals to 2% per quarter, or 8% per annum. Mitigants include: 1) Clear-cut eligibility and duration parameters on 30-day loan deferments to avoid understatement of delinquencies (e.g., by declaring a loan as delinquent after 30 days, granting a deferral to “cure” the delinquency, declaring the loan delinquent after another 30 days, granting another deferral, and so on). 2) The switch to simpler and, therefore, more transparent accounting practices for securitizations. 3) ACF’s accountability to the warehousing banks, documented under periodic covenant compliance reports. 4) ACF’s submission to transaction-specific due diligence by FSA and MBIA, usually followed by that of the ratings agencies. 5) High levels of financial disclosure continuing through to the December 2002 quarter. • A busted business model would become a recipe for ACF’s prolonged adversity, especially with a permanent reduction in recovery values of collateral. Mitigants include: 1) A simple, intelligible, and intelligent business strategy. 2) ACF’s ability to step back quickly from failed initiatives (e.g., the quick and digestible $10 million exit from a mortgage banking experiment two to three years ago). 3) ACF’s understanding of its product and business life cycle to adapt to changing conditions. • Computer chaos or econometric forecasting, including “proprietary risk-scoring models,” is sharp and elegant but quite often inaccurate. Beyond the typical problems of sensitivities to initial conditions and garbage-in/garbage-out, the capital markets have witnessed the fall from grace of “rocket scientists” for

- 14. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 14 whom “one-in-22-standard deviation” phenomena occurred with an annoying frequency sufficient to become the standard rather than the deviation. ACF and its risk models are not automatically exempt form these pitfalls. Mitigants include: 1) The redundancy of ACF’s balance sheet to absorb the unexpected. 2) The ability of ACF to withstand previous market shakeouts among securitizing subprime lenders. 3) The strength shown by ACF to break even during an unusually challenging business environment. 4) ACF’s periodic review and reforming of its risk-scoring models with the aid of outside experts, such as Fair, Isaacs & Company. Conclusion: Placing ACF’s Liquidity Hurdle into a Larger Perspective of Securitization Cash Flows Due to the current economic conditions and declining resale values, ACF’s period of deferral prior to the receipt of excess cash spread is longer than anyone anticipated at 18 months, as opposed to 12 months. Aggravating this near-term absence of cash flow are another $140 million in cash receivable from older pools that FSA has trapped through cross-collateralization protections, probably for the life of all of the insured programs because the new level of over-collateralization basically doubles to 25%. FSA has purchased bond insurance to cover losses on these pools; such policies are known as “wraps.” FSA has wrapped 15 of 19 securitizations. This convergence of an additional six months in the money lag on new securitizations and the absence of cash that ACF would normally be receiving from older trusts presents a real and immediate challenge to the company’s ongoing operations. Liquidity remains scarce for non-investment-grade companies in general and for non-investment-grade subprime lenders in particular. ACF will probably need to rely on outside bank lines, which will remain “at the ready” to manage short-term liquidity. ACF is ending its practice of deferring the majority of its initial deposits by depositing 10% upfront out of the proceeds of each new securitization and by deferring 5%, versus its former practice of depositing 3% upfront and deferring 9%. In the future, ACF will be getting its excess spread a year earlier at the expense of lending capacity that it never intends to use. For example, after four months, ACF has already collected $62 million in fees from the October 2002 $1.7 billion securitization, and 85% of this amount was in excess of the 2.25% management fee. This particular ABS transaction is an accelerated one-off structure, whereas the newer structures will allow these flows after six months. Nevertheless, the $1.7 billion transaction will grant liquidity to allow an anticipated ABS, as well as subsequent issues, to surpass cash flow thresholds. The cash to be trapped by FSA, however, will lie beyond the company’s control. ACF ordinarily receives the bulk of its excess spread from a given securitization on the tail end of its average life (i.e., during months 18 through 30), when no part of the cash stream is diverted into collateral accounts and when a lower portion is paid to investors. The money that ACF had expected to receive from these older (“seasoned”) pools still exists, but not in the company’s coffers. (For a simplified description of how these transactions work, please refer to Appendix A.) Below are two tables; one ages the securitizations and the other tracks the expected receipts of I/O silver over the next four years. By their asymmetry, these tables demonstrate that recent loan origination volumes, subsequently securitized, do not determine the subsequent stream of excess cash flows. NOTE: The tables below measure cumulative ABS issues and the cumulative receipt of I/O income. The percentage values within, or next to, each column correspond to specific portions of the overall amounts issued and outstanding, or of income to be received, in specific years.

- 15. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 15 Distribution of Securitizations '98-02 0 25 50 75 100 At F.Y.E. Jun-98 At F.Y.E. Jun-99 At F.Y.E. Jun-2000 At F.Y.E. Jun-01 At F.Y.E. Jun-02 Percent 3% 1% Source: Company financials Intuitively, we expect a much larger portion of the I/O to be paid off in 2003 because most of the securitization activity took place in 2001 and 2002, and a disproportionate majority of outstanding ABS issues resides in these same years. Were I/O income driven by volume from the current ABS issues, the income from the transactions (illustrated below) would skew more to the left. Rate of I/O Accumulation 0 25 50 75 100 F.Y.E. Jun-03 F.Y.E. Jun-04 F.Y.E. Jun-05 F.Y.E. Jun-06 Cumulative Receipts Expected under I/O Percent Source: Company financials This phenomenon of increasing out-year fees makes sense. The blended rate of the tranches is one-third of the 17.3% rate on the auto loans. Car owners make level monthly payments. As the level payments arrive, the trustee bank pays principal and interest first, as well as operating fees; residual amounts either flow into an underfunded collateral account to ABS investors entitled to prepayments or to ACF as excess spread. As the principal portion of these level payments declines over time, so do the interest payments to the ABS investors, leaving more and more funds flowing into excess spread. In this sense, ACF is being rewarded—or penalized— for the subsequent performance of the loan pool that it originated. Nonpayments, deferred collateral account funding, and resale values complicate the timing and the details, but the overall picture remains essentially the same. PV of future receipts = $514 million at June 2002 $20.6 billion of securitizations issued since 1998 $12.1 billion still outstanding 18% 27% 34% 33% 6% 6% 22% 17% 38% 45% 19% 31%

- 16. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 16 Appendix I Primer on Asset-Backed Securities (ABS/ABS Issues) The conceptual framework: like any exotic financial instrument, an ABS security combines simple building blocks to create a complex, if not mysterious, structure. ABS issues amalgamate the following fundamental elements: [a] Receivables factoring. [b] Asset management. [c] Standardized terms for secondary market trading. [d] The multiplier effect. [e] GAAP accounting for the “true” sale of assets. The structure reflects the requirements of the capital markets for standardized and clear trading terms, and the complexity arises because sponsors act in two different roles. The anxiety that many exhibit towards securitization emerges over concerns of leverage “blowing up” the company that is originating the ABS securities—the “securitizer” or “sponsor”—as well as the heroic applications of GAAP’s “true” sale convention. The latter concern has not been resolved adequately over time, and, therefore, many securitizers, including ACF, are dispensing with gain-on-(true?)-sale accounting. The fear over leverage displays a forgetfulness regarding the basic economics underlying financial intermediation, as discussed in detail below. Trustees reduce potential conflicts of interest by acting on behalf of the ABS investors. Further, the proper implementation of the compensation to be earned over the life of the issue by its sponsor—and reviewed by the trustee—assuages the conflict of interest by paying the issuer for conveying selectively underwritten assets (i.e., receivables) to the special-purpose/bankruptcy-remote entity (SPE). Specific eligibility criteria for the receivables sold resemble investment guidelines imposed on any closed-end investment manager. Subsequent portfolio performance above certain benchmarks rewards the sponsor as investment manager. In ACF’s case, these benchmarks are minimum collateral set-asides and interest payments to investors. The originator that monetizes its assets factors the accounts receivable directly to the capital markets with the aid of an investment bank. As the “seller” of the pooled assets, the securitizer conveys its ownership interest in the assets to a SPE managed by a trustee on behalf of the ABS investors. The SPE then issues notes and uses the proceeds to purchase the in-flowing assets at some discount. ABS structures typically rely upon sequenced repayments among several tranches. Under this “waterfall” approach, each tranche pays out completely at or ahead of its scheduled maturity, as well as prior to all others junior to it. The sponsor “buys,” or assumes, an equity/residual interest in the ABS issue. Oftentimes, (e.g., in the instance of ACF), the securitizer’s position breaks out into two securities. One is funded after the issuance with the first 5% to 10% of excess cash flows received. The other represents a nominal gain on sale of the receivables for the sponsor, arising from the low coupon rates for the investment-grade ABS notes and the much higher interest charged by the sponsor on the underlying customer loans. These two tranches comprise the first-loss position of the ABS issue, borne by the sponsor. The investment banks taking the issue to market, and working closely with the ratings agencies, set this first-loss position at a level high enough for every other tranche to be rated investment-grade, with the most senior pieces (representing 10% to 20% of the advanced amount) earning an AAA rating.

- 17. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 17 ACF’s two retained ABS securities are as follows: 1) a slightly higher-ranking, slightly structured security akin to a preferred stock, “investment in trust receivable” ($791 million as of December 2002), and 2) a pure residual booked as a gain on sale of the receivables. The first 5% of cash flow in excess of fixed charges, including the 2.25% “base” management fee owed to ACF, pays for the investment in trust receivable. The common equity residual appears on the balance sheet of the securitizer as an interest-only (I/O) security because it quantifies and discounts the future income that will accrue on ACF's investment in the trust receivable. The sponsor acts in two discrete capacities: 1) as the seller of owned receivables at a small discount off of face value (i.e., the haircut) and 2) as an asset manager of selected assets (i.e., receivables conveyed to the SPE), with compensation based on a fixed-asset management fee, payable per annum, plus a subsequent performance bonus realized through the I/O or “investments in trust receivable.” After the funding of the cash component of the first-loss position, additional cash trapping (i.e., excess spread held by the trustee to replenish or increase collateral accounts) may be unexpected and unwelcome but not unthinkable. As the seller, the ABS sponsor continues to collect the payments due from its customers, instructing customers to send their checks to a bank-sponsored lockbox; the bank that sponsors the lockbox then forwards these receipts to the trust account managed by an outside trustee (often, Wilmington Trust Corp.; Bank of New York Company; U.S. Trust Corp.; or, State Street Corp.). The trustee amasses funds during specific intervals (e.g., calendar quarters) and releases them as interest and principal (re)payments to various ABS investors per a specified waterfall, as follows: • Cash interest due on all rated tranches actually sold in the market, ACF's “base” asset management fee of 2.25%, and fixed administrative expenses (e.g., fee to the trustee, etc.). • Principal due to the AAA senior tranche investors. • When applicable, fees to third-party credit support providers (e.g., bond insurers) for additional enhancement. • Deposits into “rainy day” funds (i.e., the first-loss position detailed above). • Any principal remaining on the A2 tranche (once the AAA tranche is repaid), subject to items such as minimum hold periods with the remaining investment-grade tranches. Following these specified waterfalls, interest and principal due to the sponsor will assume the first-loss position, which will be paid with the final cash flows in the pool, as well as with released collateral. A simple example demonstrates the power of securitization. For example, suppose that a sponsor has raised $1.00 from the issue of stock and has subsequently extended $1.00 of consumer loans to individuals with low credit ratings. The sponsor pools these loans totaling $1.00 and sells them to a special-purpose entity at $0.98 per dollar. After buying a junior security with the first $0.08 of excess spread, the sponsor recoups only $0.90 in cash.. The sponsor now has $0.90 of fresh funds for new loans, which it extends. With the $0.90 of receivables on hand, the securitizer sponsors another ABS issue with the same characteristics, generating $0.81 of new funds and so forth. This cash carousel is nothing more mysterious than a privatized version of the “multiplier effect” learned in macroeconomics 101. As long as lending standards remain the same, this sponsor can originate up to $10.00 in loans from the $1.00 of equity raised (i.e., $1.00 ÷ 10%). This upper limit of loans generated from the original dollar represents a sponsor’s lending capacity.

- 18. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 18 The Case of AmeriCredit ACF, as a sponsor, has traditionally faced substantial opportunity costs imposed by earning 1½% money market rates on inactive collateral accounts while foregoing historical net interest margins of 12% during its period of rapid growth of loan originations. To monetize the collateral represented by $791 million of “interests in investment trusts” as of December 2002, ACF has typically purchased bond insurance to cover losses on these pools; such policies are known as “wraps.” These wraps have enabled ACF to recycle higher percentages of its receivables as new car loans profitably. ACF has developed a close working relationship with AAA-rated Financial Security Assurance, Inc., which is now a unit of Brussels-based Dexia, S.A. FSA’s challenge has been to ensure that ACF does not relax its credit discipline. To accomplish this end, FSA has required cross-collateralization of its many wraps (currently 15 of 18 securitizations outstanding). With relatively level amounts of cash flowing in from pools of monthly amortizing car loans, each layer of the waterfall repays predictably over the two- to four-year life of a given securitization. Consequently, the age of the ABS transaction correlates with the level of cash that accrues to ACF; older transactions enable higher levels of cash to accrue to ACF as released collateral or excess spread. Without cross-collateralization, or something similar, ACF would have less incentive to maintain credit standards on subsequent securitizations. ACF’s increased accountability to FSA under the cross-collateralization creates an incentive for ACF to remain prudent with regard to its lending standards so that it can reap the benefits of these growing cash flows. If losses mount more quickly than expected, FSA may invoke the cross- collateral protection to quarantine cash that is due to ACF. ACF is currently confronting this issue. Although this situation is serious, it is not fatal. Many of the alarmist reactions of market commentators tend to overlook ACF’s dual role as the seller/originator of the assets conveyed to the SPE for which it booked a gain (i.e., its recompense for the sale) and as an asset manager selecting and managing certain assets (i.e., subprime car loans) on behalf of ABS investors. In the present situation, ACF is losing opportunity value, similar to an asset manager failing to earn a performance bonus (except that ACF may still receive that cash flow at a much later date). The true difficulty remains the fact that, on many wrapped transactions, ACF will not obtain control of the cash for up to two years. Should loss rates level off and performance stabilize, ACF will eventually receive this withheld cash as the last of the cross- collateralized transactions mature. ACF has three strengths vital to its continued growth: 1) a willingness to reduce the amount advanced against sold receivables from current levels of 92%–97% to 90% (with 5% to 6% still being deferred); 2) a recognition that its basic business is mature enough for it to reduce the need for large lending capacity; and 3) a strong track record during other difficult markets (e.g., 1997–1998). These strengths will enable ACF to continue without third-party enhancement but with the aid of deeper collateral support, if necessary. Another View of AmeriCredit’s Equity Investments in Trust Receivables and Excess Spreads Before proceeding with our explanation, we state, once again, that the equity in the trust receivables enjoys a claim senior to that of the I/O security. In fact, these equity investments represent the principal on which the excess spread, discounted into the I/O security, accrues as income. We now cast ACF in a third role, an equity investor, in addition to those of originator and investment manager, buying into an investment pool through the use of margin. When ACF was busy building its franchise, it lacked the cash to pay for all of its investments upfront. ACF temporarily relinquished 8% to 12% of a securitization pool’s asset value (i.e., the first-loss/collateral requirement) to buy into the pool itself. This leveraged investment enabled a securitization to proceed. As explained earlier, if ACF did not redeploy this deferred

- 19. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 19 margin for new loans and, instead, paid it in as collateral, it would be much less profitable than the alternative of generating an additional 17% in auto loans with the proceeds. By working with FSA and investment banks, ACF was able to buy that larger stake in the securitization with a 25% down payment. ACF provided 3% of the proceeds and paid for the remaining 9% out of future excess spreads (i.e., “money on the come”). The tradeoff made sense, but ACF now had to wait for slightly more than a year before it saw any excess spread in cash. As the pooled loans successfully ran off over two or three years, the 12% placed into the collateral account (i.e., the initial equity investment) would then revert to ACF. Therefore, as a result of this investment, ACF earned the excess spread and the deposit with a favorable 34% to 44% implied return and, crucially, a return with back-ended cash receipts. The attachments that follow Appendix I provide a simplified, step-by-step view of the mechanics of a securitization and how it generates income on its residuals. Please note that some text is crossed-out; this etching is deliberate. The strike-through emphasizes the fact that these are complex structures with several moving parts in which the same institutions play various roles throughout the life of a given transaction. The strikethroughs represent the proverbial “hat” not worn in that stage of an ABS issue. For example, the warehouse bank and the advising investment bank are quite often one in the same, acting under the unspoken rationale of “you give us your balance sheet, we’ll give you our gravy.”

- 20. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 20 Appendix I, Attachment A AmeriCredit As the Originating/Fronting Financier AmeriCredit: Acts in three capacities: § Loan originator fronting for capital markets, eventually as the “seller” 1. Borrows from warehouse bank, pledging loan contracts in settlement 2. Advance of 95% of contracts’ face value 3. ACF funds other 5% through its own resources § Asset manager for the ABS investors and primary collector of monthly payments – through a “lockbox” bank from sun-prime debtors as the “servicer” § Active investor in a pool of levered assets through “investment-in-trusts,” income capitalized as I/O Warehouse Banks: Deutsche Bank, J.P. Morgan/Chase, Bank- 1, Barclays Capital, Merrill Lynch, Lehman, Crédit Suisse-First Boston, and Wachovia. TOTAL CAPACITY: $3,400 for 2–3 years. WORKING CAPITAL to build presecuritization inventory; interest rate of 5%. 75,000 Consumer Debtors: § $45,000 income/year § Perhaps one bankruptcy in the past § 600 FICO score (score for prime borrowers starts at 720 out of 800) § Referred over “Dealer-Track” Internet site by a used car salesman § For a loan of $13,333, pays $387 per month at 17.3% for four years § 99% of balances pay each month due to delinquency, 1-month deferral or charge-off § 1.75% management fee § net / risk-adj. Spread of 6% $950 millionRights to 75,000 loans; documents assigned to banks 19,401 auto dealers with whom ACF does business $1 billion Used cars Contract, pledging auto, first-born, etc. as collateral

- 21. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 21 Appendix I, Attachment B AmeriCredit As Active Equity Investor The day before closing of the “pass-through” securitization AmeriCredit: Acts in three capacities: § Loan originator fronting for capital markets, eventually as the “seller” 1. Borrows from warehouse bank, pledging loan contracts-in-settlement 2. Advance of 95% of contracts’ face value 3. ACF funds other 5% through its own resources § Asset manager for the ABS investors and primary collector of monthly payments – through a ‘lockbox’ bank from sun-prime debtors as the “servicer” § Active investor in a pool of levered assets through “investment in trusts” (i.e., SPEs); income capitalized as I/O Trustee: State Street; Wilmington Trust or USTrust; Bank of NY, et al.: § Acts as atty-in-fact for SPE, holding perfected right to loans receivable sold by ACF § Receives pass-through funds of debtors § Pays execution fees to… 1. Itself (10 basis points) 2. Lockbox bank (5 b.p.s) 3. Credit support provider (20) § Execution cost of 35 bps § Effective interest of 5% § Sets up collateral deposit account with another bank Lockbox bank receives payments from debtors; at close of ABS, instructed by ACF to remit cash received to the trustee. Consumer Debtors: § $45,000 income/year § Perhaps one bankruptcy in past § 600 FICO score (score for prime borrowers starts at 720 out of 800) § Referred over “Dealer-Track” Internet site by a used car salesman § Pays $400 month at 17% for 5 yrs § 99% of balances pay each month due to delinquency, 1-month deferral or charge-off § 1.75% management fee § net/risk-adj. Spread of 6% Third-Party Credit Support Provider; Either a bond insurer (FSA or MBIA) or letter-of-credit bank § Guarantees accelerated payments from collateral account; § Guarantees payment of debt service as contractually scheduled § Deepens penetration ACF-sponsored ABS issue § AAA rating reduces blended coupon rate by 20% Investment Bank: Deutsche Bank, J.P. Morgan/Chase, Merrill Lynch, Lehman & Crédit Suisse-First Boston. Advisory role in structuring transaction; best-efforts placement in ABS market. ACF instructs customers to remit monthly payments to lockbox bank Monthly loan payments to lock-box bank account in name of trustee $2 million $2 million Coordinates key stake- holders; deal is “good to go”$1 million; advisory fee (10 b.p.s) Checks the cap-marts to price the securitization & verify appetite

- 22. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 22 Appendix I, Attachment C AmeriCredit As Asset Seller Closing date of the “pass-through” securitization ABS Investors: $150 AAA @ 3.5% $250 AAA @ 4.0% $300 AA @ 5.0% $220 BBB @ 7.4% $50 equity @ excess * blended rate of 4.65% *held by ACF and quantified in I/O Warehouse Banks: Deutsche Bank, J.P. Morgan/Chase, Bank- 1, Barclays Capital, Merrill Lynch, Lehman, Crédit Suisse-First Boston, and Wachovia. TOTAL CAPACITY: $3,400 for 2–3 years. WORKING CAPITAL to build presecuritization inventory; interest rate of 5% Investment Bank: Deutsche Bank, J.P. Morgan/Chase, Merrill Lynch, Lehman & Crédit Suisse-First Boston. Advisory role in structuring transaction; best-efforts placement in ABS market. AmeriCredit: Acts in three capacities: § Loan originator fronting for capital markets, eventually as the “seller” 1. Borrows from warehouse bank, pledging loan contracts-in-settlement 2. Advance of 95% of contracts’ face value 3. ACF funds other 5% through its own resources § Asset manager for the ABS investors and primary collector of monthly payments – through a ‘lockbox’ bank from sun-prime debtors as the “servicer” § Active investor in a pool of levered assets through “investment-in-trusts” (i.e., SPEs); income capitalized as I/O Trustee: State Street, Wilmington Trust or USTrust, Bank/NY, et al.: § Acts as atty-in-fact for SPE by holding perfected right to loans receivable sold by ACF § Receives funds of debtors § Pays execution fees to… 1. Itself (10 basis points) 2. Lockbox bank (5 bps) 3. cCedit support provider (20) § Execution cost of 35 bps. § Effective interest of 5% § Sets up collateral deposit account with another bank Special Purpose Entity (“SPE”): Required under a true-sale securitization… § ACF holds nominal ownership § Bankruptcy-remote (no recourse to ACF) § Account flows controlled by trustee § Places 5% of proceeds in deposit account with collateral bank Collateral Bank § Retains initial collateral from issue date § Captures all excess spread equal to 9% of the par amount of ABS issue § After 12% of first-loss position is funded, remits excess spread to ACF… 1. Incentive/performance-based comp as asset manager AND/OR 1. Dividends on leveraged “equity-in-trust receivables” investment Places multi- tranche ABS issue $950 million; ACF pays for its $50 million investment through haircut 2% of $1 billion face amount of issue; or, $20 million for placing the ABS issue 3% initial collateral; or, $30 million $950 million $950 million + $12 million in interest Releases lien on collateral* *75,000 auto loan contracts—face amount: $1 billion— and rights under those contracts (i.e., the “collateral”) collateral*

- 23. FRIEDMAN, BILLINGS, RAMSEY & CO., INC. Institutional Brokerage, Research and Investment Banking Page 23 Appendix I, Attachment D AmeriCredit As Passive Asset Manager Example: The first payment date after one month Note: This is an ABS “pass-through.” Principal received from the debtors becomes principal paid to the ABS investors, and interest received is interest paid. 1) Assumes all loans are performing for the first month and that each contract is exactly 48 months. 2) Any payments not received from debtors nets against excess spread. 3) If this were an older ABS program with the auto loan portfolio defaulting at current nonperformance rates, the $10.6 million placed into the excess account would be reduced by 70% to 75%, pending recovery of repossessed vehicles, which implies one year’s worth of seasoning. The first month of the ABS program should have no problems. 4) Historical (i.e., base case) default rate cut the excess spread in half. 5) With asset quality at historical levels, ACF’s collateral account would fund in 14 months; under the currently adverse conditions, the 9% excess collateral will fund fully after 21 or 22 months. ABS Investors: $150 AAA @ 3.5% due 1 year $250 AAA @ 4.0% due 2 years $300 AA @ 5.0% due 3 years $220 BBB @ 7.4% due 4 years $50 equity @ excess * due????? blended rate of 4.65% *held by ACF and quantified in I/O Collateral Bank: § Retains initial collateral from issue date § Captures all excess spread equal to 9% of the par amount of ABS issue § After 12% first-loss position funded remits excess spread to ACF… 1. Incentive/performance-based comp as asset manager AND/OR 2. Dividends on leveraged “equity-in-trust receivables” investment Lockbox bank receives payments from debtors; at close of ABS, instructed by ACF to remit cash received to the Trustee Trustee: State Street; Wilmington Trust or USTrust; Bank/NY, et al.: § Acts as atty-in-fact for SPE, holding perfected lien on loans receivable sold by ACF § Receives pass-through funds of debtors from SPE at instruction of lock-box bank § Pays execution fees to… 1. Itself (10 basis points) 2. Lockbox bank (5 bps) 3. Credit support provider (20) § Execution cost of 35 bps § Effective interest of 5% § Sets up collateral deposit account with another bank 75,000 Consumer Debtors: § $45,000 income/yr § Perhaps one bankruptcy in past § 600 FICO score (score for prime borrowers starts at 720 out of 800) § Preferred over “Dealer-Track” Internet site by a used car salesman § For a loan of $13,333, pays $387 per month at 17.3% for four years § 99% of balances pay each month due to delinquency, 1-month deferral or charge-off § 1.75% management fee § Net/risk-adj. spread of 6% $28,968,819: $41,667 custodial fee deducted Collateral Bank deducts $62,500 fee (7.5 bps) and places $10,528,818 into collateral deposit account of ACF; balance remaining to be deposited: $79,458,021 deposit int. of 1 month slightly reduces balance to be paid. Payments to ABS investors: § $14.8 million to 1 yr AAA 1. $14.4 million principal 2. $0.4 million interest remaining tranches get int.: § $0.8 million to 2 yr AAA § $1.25 million to AA § $1.4 million to BBB TOTAL payments (incl. fees) of $18.4 million Excess spread of $10.6 million