Consumer perceptions of the UK financial services revealed, 1:5 bitter & hostile

Viewpoint_Issue_4

1. Keeping you connected to today’s UK financial services market

Welcome to the fourth edition

of viewpoint, Harris Interactive’s

UK financial services newsletter.

In this edition we focus on retirement,

the levels of pension provision people

have made, and how they feel about

their life in later years.

We hope you find this newsletter

informative and useful. If you wish to

find out more about the work we do

within the financial services industry

please get in touch.

Frances Green: Financial Services

Director

On 12th January, the new

Pensions Bill 2011 was introduced

to the House of Lords which will

abolish the default retirement age

and bring forward the increase in

the state pension age.

With the inevitable impact on the

Financial Services market, in this

edition of viewpoint, we examine

the challenges consumers face

getting to grips with the pensions

market, how prepared consumers

are for retirement and what this

means for financial organisations.

Would you pass a moral

character test?

In 1908 the government

introduced the first state pension.

It was a non-contributory scheme

subject to means and 'moral

character' tests. Given the

prejudice of the time I wonder

how many working within our

sector would pass that test today?

Every government since has tried

to make its mark. With an

ever-aging population it has

become increasingly important for

people to provide for their own

retirement rather than have an

over reliance on the state.

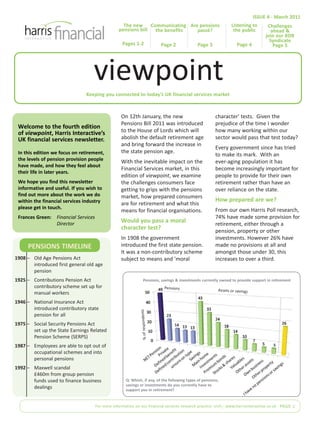

How prepared are we?

From our own Harris Poll research,

74% have made some provision for

retirement, either through a

pension, property or other

investments. However 26% have

made no provisions at all and

amongst those under 30, this

increases to over a third.

For more information on our financial services research practice visit:| www.harrisinteractive.co.uk PAGE 1

ISSUE 4 - March 2011

viewpoint

The new

pensions bill

Pages 1-2

Challenges

ahead &

join our RDR

Syndicate

Page 5

Are pensions

passé?

Page 3

Communicating

the benefits

Page 2

Listening to

the public

Page 4

Q: Which, if any, of the following types of pensions,

savings or investments do you currently have to

support you in retirement?

1908 – Old Age Pensions Act

introduced first general old age

pension

1925 – Contributions Pension Act

contributory scheme set up for

manual workers

1946 – National Insurance Act

introduced contributory state

pension for all

1975 – Social Security Pensions Act

set up the State Earnings Related

Pension Scheme (SERPS)

1987 – Employees are able to opt out of

occupational schemes and into

personal pensions

1992 – Maxwell scandal

£460m from group pension

funds used to finance business

dealings

Pensions, savings & investments currently owned to provide support in retirement

Pensions Assets or savings

%ofrespondents

PENSIONS TIMELINE

2. Issue 4 | March 2011

For more information on our financial services research practice visit: www.harrisinteractive.co.uk | PAGE 2

viewpointContinued from page 1...

Q: When thinking about retirement, which words

come to mind to describe how you feel?

With such a reliance on the State

pension it is worrying that few are

aware of the value of this - over a

quarter say that the maximum of

£97.65 per week is less than

expected, so is it any surprise that

many are filled with fear at the

thought of retirement?

So why are so many not preparing

for their retirement? I believe the

sector and the government are

really not helping themselves. The

market clearly is too complex, using

terminology consumers quite simply

do not understand.

There are also a multitude of

different types of pensions:

Contributory, Non Contributory,

Stakeholder, Personal, Defined

Benefit etc. With National

Employment Savings Trusts (NESTs)

joining this mélange from 2012, it is

understandable why consumers are

confused and are not engaging with

schemes designed to support them

in their golden years.

Many people, quite rightly state that

affordability is a major issue, though

I do sympathise with that point of

view, I also feel that the government

and financial organisations have

both failed to communicate the

benefits (emotionally and rationally)

of preparing for retirement and have

helped to create a society of

consumers living for the here and

now. Why should I save? Especially

when the government will provide

for my later life and I’d rather be

tottering around in those new

Jimmy Choo’s (which surely are an

investment in themselves?!)

Communicating the benefits

Those who are confident in their

retirement plans are happier about

their concept of retirement, using

words such as ‘freedom’, ‘free’,

‘relaxed’, and ‘happy’. Personally

as I am writing this, the thought of

1995 – Pensions Act

response to Maxwell, set up

regulatory and compensation

schemes

1999 – Introduction of Minimum

Income Guarantee, income

support for poorest pensioners

2001 – Introduction of stakeholder

pensions

2002 – Switch from SERPS to State

Second Pension

2003 – Introduction of the Pension

Credit, bringing pensioners into

means-testing

2007 – Pensions Act 2007

the creation of the PADA

(Personal Accounts Delivery

Authority)

2010 – PADA announced that NEST

(National Employment Savings

Trust) will be the permanent

name for the personal accounts

scheme

2011 – State pension age for women

to increase to 65

2012 – Workplace pensions reforms

due to come into effect

2020 – State pension age increasing

to 66

2036 – State pension age increasing

to 67

2046 – State pension age increasing

to 68

Those confident in their retirement provision

Compiled from multiple sources:

BBC News

The Pensions Advisory Service

National Employment Saving’s Trust

PENSIONS TIMELINE

3. Issue 4 | March 2011

For more information on our financial services research practice visit: www.harrisinteractive.co.uk | PAGE 3

retirement is nothing but a distant

glimmer. With the unshakeable

January blues, I’d love to take the

eternal holiday in Eastbourne after a

lifetime of hard work with a

well-earned G’n’T.

Realistically though, I know that

after I’d taught myself to crochet, I’d

be looking for something to do... but

that’s not even thinking about how

I’d afford it.

However, the word ‘retirement’ now

instils dread in many with almost

half feeling unconfident about the

amount of provision they have

made. Feelings of worry, being

scared, and uncertainty now enter

the fray, so much so that 31% expect

to have to work out of necessity

when they come to retire.

Inexplicably, despite this clear lack of

preparation almost half of working

people also expect their standard of

living to increase or at least remain

the same when they retire, so how

can we help people plan ahead,

increase confidence and make the

world a happier place?

We do have to remember

retirement planning doesn’t

necessarily mean ‘pensions’. Four in

five hold other savings or assets

such as building society accounts,

their main home and around a

quarter have other investment plans

such as ISAs.

What is evident is the lack of

confidence people have in pensions

themselves. When asked to rate

confidence in providing a

guaranteed source of income for

retirement, property and ISAs rank

higher than a designated pension

scheme, perhaps due to the current

volatile times but also perhaps

because those now planning their

retirement lived through the

pension mis-selling of the 80s

and 90s.

viewpoint

Q: How confident are you that your current retirement provision will provide

you with a large enough income to support you throughout your retirement?

Confidence in current provision to provide support throughout retirement

90%

0%

10%

20%

30%

40%

50%

60%

70%

80%

100%

5

13

27

26

20

9

Don’t know

Very confident

Very unconfident

Fairly unconfident

Neither

Fairly confident

Those not confident in

their retirement provision

Q: When thinking about retirement, which words

come to mind to describe how you feel?

4. Issue 4 | March 2011

For more information on our financial services research practice visit: www.harrisinteractive.co.uk | PAGE 4

Continued on page 5...

viewpoint

Are pensions passé?

Due to the complexity of the

pensions market, consumers seem

unwilling to invest the time to

understand the market. Employers,

providers and the government need

to do more to promote the benefits

of pensions and explain how

consumers can take more of an

active role managing rather than

opting for the default fund.

Even during these turbulent times

less than half have reviewed their

pension fund in the last 12 months

and just under a quarter have never

reviewed their funds. That doesn’t

mean that Mr General Public can’t

understand, but there is a reliance

on someone else to advise, followed

by a ‘head-in sand’ approach until

the nest-egg incubation period is

over.

Any way to reassure customers they

can understand will encourage

better planning. People may have

more confidence in property or cash

ISAs but that’s simply because they

generally have more interaction and

understanding, they forget about the

tax breaks with pensions as well as

the possible ‘employer’ contribution.

Given what’s happening within the

property market at the minute and

cash ISA levels, are they really the

better investment?

ISAs or property have such appeal to

customers because they want more

flexibility to choose when and how

benefits can be drawn. Whilst the

benefits of such investment-led

schemes are sound in theory,

generally people see savings with a

guaranteed interest as more inviting

and secure at this moment.

The lack of pro-activity also

contributes to non-take up of

company pension schemes. When

starting a new job, feedback

indicates that this is the last thing on

the minds of new employees. NESTs

go some way to resolve this through

auto-enrolment, and a third of the

public agree this is a positive

initiative, but is enforcement really

the answer when it does not

promote a greater understanding?

Interestingly, NEST has recently

published a handy phrase book

which gives the terms that ensure

clarity and encourage take up in

schemes: http://nestpensions.org.uk

/documents/NEST_phrasebook.pdf

This will help instil greater levels of

consumer confidence and provide a

greater understanding, but we still

need to address the confidence in

the industry as a whole.

The introduction of the Retail

Distribution Review will also help to

reassure consumers that financial

advisors aren’t in fact the

devil-incarnate, selling in their own

interest, but people that provide

sound advice. Though, as consumers

struggle to place any intrinsic value

upon the advice they receive, I

suspect the impact on the

consumer’s pocket of paying £670

(the cost of full advice) will deter

those who are less engaged even

further.

Q: Please rank the following ways of investing or saving money in order of the confidence

you have in them to provide you with a guaranteed source of income for your retirement

Confidence in providing guaranteed source of income for retirement

Property

ISAs

Pension schemes

Other savings

Bonds

Stocks and shares

Investments in jewellery

Investments in antiques

1st

2nd

3rd

5. Issue 4 | March 2011

For further information related to this article, such as the background data, or to suggest new topics for

inclusion please email financial@harrisinteractive.net or call +44 (0)161 615 2300

This edition was

researched and writ-

ten by Lynn

Tweedale, Senior

Research Manager,

Financial Services

Research Team.

Continued from page 4...

To share the latest thoughts

and options of financial

services team, visit our pages

at:

www.harrisinteractive.co.uk

Here you will find recent case

studies, visit our blog, post your

comments, download recent

reports, and access the archive

of viewpoint newsletters.

Join our RDR

Investor Syndicate

Harris Interactive invites you to

participate in our new Investor

Syndicate focusing on the Retail

Distribution Review.

The syndicate offers a cost-

effective way of regularly

monitoring investor awareness

and attitudes towards the

changes proposed by the RDR,

likelihood to use advice when

taking out investment

products and with what level

of advice. The next wave will be

taking place in April.

For further details, contact:

Frances Green:

fgreen@harrisinteractive.com or

Michael Worledge:

mworledge@harrisinteractive.com

viewpoint

The yellow brick road forward

So, how can institutions overcome the

challenges and meet needs of

customers in the modern retirement

landscape?

There is always the possibility of using

scare-tactics of ‘what-if’s’. However

painting a picture of ‘freedom’,

‘relaxation’, ‘happy’, ‘excited’ and

perhaps even a G ‘n’T will help people

to get engaged and using simple

terminology to empower them is

undoubtedly the key.

Financial advisors and employers are

the key touch-point for many.

Providers need to ensure that

appropriate marketing support is made

available using clear terminology and

imagery.

Employers also need to ensure they

allow employees the time to talk

through their options with advisors,

helping them to plan on a regular

basis.

Targeting those who currently reside in

the default fund would be a great

start, are they really in the right fund

for them? Are they investing the right

amount given their hope and dreams?

Demonstrating the online tools that

many schemes now have will also help

people to feel empowered.

We do have to remember that

traditional pension schemes aren’t

relevant to everyone, but for many

they are still the right investment

vehicle. With so many seemingly

unable to afford a pension, many are

missing out on the contributions of

their employer as well the associated

tax benefits. The government really

does need to try and change this

living-just-for-today attitude.

But ultimately, for all the encouraging

changes in legislation and

hand-holding through the pensions

maze as with all things financial, we

will need to wait a generation for

customers to reap the benefits of the

changes happening now…

and by then… science may have found

the fountain of eternal youth.