More Related Content Similar to WA_Koss and Lucier in Global Trade Magazine online_04 11 16 (20) 1. 4/12/2016 PrintFriendly.com: Print web pages, create PDFs

http://www.printfriendly.com/print?url=http%3A%2F%2Fwww.globaltrademag.com%2Fglobaltradedaily%2Fcommentary%2Fusexportershaveyouconside… 1/2

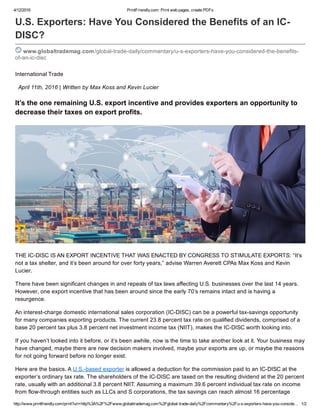

U.S. Exporters: Have You Considered the Benefits of an IC

DISC?

www.globaltrademag.com/globaltradedaily/commentary/usexportershaveyouconsideredthebenefits

ofanicdisc

International Trade

April 11th, 2016 | Written by Max Koss and Kevin Lucier

It’s the one remaining U.S. export incentive and provides exporters an opportunity to

decrease their taxes on export profits.

THE ICDISC IS AN EXPORT INCENTIVE THAT WAS ENACTED BY CONGRESS TO STIMULATE EXPORTS: “It’s

not a tax shelter, and it’s been around for over forty years,” advise Warren Averett CPAs Max Koss and Kevin

Lucier.

There have been significant changes in and repeals of tax laws affecting U.S. businesses over the last 14 years.

However, one export incentive that has been around since the early 70’s remains intact and is having a

resurgence.

An interestcharge domestic international sales corporation (ICDISC) can be a powerful taxsavings opportunity

for many companies exporting products. The current 23.8 percent tax rate on qualified dividends, comprised of a

base 20 percent tax plus 3.8 percent net investment income tax (NIIT), makes the ICDISC worth looking into.

If you haven’t looked into it before, or it’s been awhile, now is the time to take another look at it. Your business may

have changed, maybe there are new decision makers involved, maybe your exports are up, or maybe the reasons

for not going forward before no longer exist.

Here are the basics. A U.S.based exporter is allowed a deduction for the commission paid to an ICDISC at the

exporter’s ordinary tax rate. The shareholders of the ICDISC are taxed on the resulting dividend at the 20 percent

rate, usually with an additional 3.8 percent NIIT. Assuming a maximum 39.6 percent individual tax rate on income

from flowthrough entities such as LLCs and S corporations, the tax savings can reach almost 16 percentage

2. 4/12/2016 PrintFriendly.com: Print web pages, create PDFs

http://www.printfriendly.com/print?url=http%3A%2F%2Fwww.globaltrademag.com%2Fglobaltradedaily%2Fcommentary%2Fusexportershaveyouconside… 2/2

points.

The ICDISC, in most cases, is a paper entity, a U.S. corporation that is paid a commission by the related supplier

—the exporter—on its export sales. Keep in mind, this is an export incentive that was enacted by Congress to

stimulate exports. It’s not a tax shelter, and it’s been around for over forty years.

The commission paid to an ICDISC is generally the greater of 50 percent of the net profits, or four percent of the

gross receipts, but not more than 100 percent of the net profits, on exports of products that are manufactured,

grown, or extracted in the United States.

The products must be manufactured, grown, or extracted in the United States by an entity other than the ICDISC.

The products must be held primarily for sale, lease, or rental for direct use, consumption or disposition outside the

United States. Up to 50 percent of the fair market value of the export property can be attributable to foreign

content.

An ICDISC must also be a domestic corporation; have at least $2,500 in capital; have only a single class of stock;

file a timely election to be treated as an ICDISC; and must meet a 95 percent qualified export asset test and a 95

percent qualified gross receipts test.

An ICDISC is not subject to U.S. income tax. It is more like a partnership, LLC, or S corporation in that its

shareholders are subject to U.S. income tax on their share of the ICDISC’s income. The exporter, its

shareholders, its management, its employees, family members or any combination thereof can own the ICDISC.

For example, the ICDISC can be used to generate incentive bonuses for management or employees, or facilitate

succession planning. Alternatively, the funds accumulated in the ICDISC can be distributed to the shareholders

and loaned or contributed back to the exporter if the cash is needed.

The ICDISC regime is the one remaining U.S. export incentive and provides U.S.based exporters an opportunity

to decrease their U.S. taxes on export profits by almost 16 percentage points. It’s worth considering, or

reconsidering, as the case may be.

Max A. Koss, CPA, is the Director of International Tax at Warren Averett CPAs and Advisors and is based in the

firm’s Birmingham, Ala. office. He may be contacted at max.koss@warrenaverett.com. Kevin C. Lucier, CPA, is a

Member in the firm’s Atlanta office, and may be contacted at kevin.lucier@warrenaverett.com.

Videos

Informative Articles from top Companies