Recommended

More Related Content

What's hot

What's hot (19)

Similar to Gold correction represents buying opportunity skyrocketing u s federal debt the catalyst litwiniuk

Similar to Gold correction represents buying opportunity skyrocketing u s federal debt the catalyst litwiniuk (20)

Recently uploaded

Recently uploaded (20)

Gold correction represents buying opportunity skyrocketing u s federal debt the catalyst litwiniuk

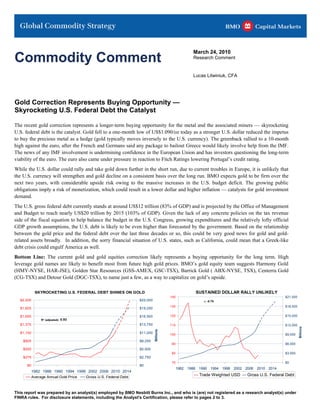

- 1. Commodity Comment March 24, 2010 Research Comment Lucas Litwiniuk, CFA Gold Correction Represents Buying Opportunity — Skyrocketing U.S. Federal Debt the Catalyst The recent gold correction represents a longer-term buying opportunity for the metal and the associated miners — skyrocketing U.S. federal debt is the catalyst. Gold fell to a one-month low of US$1.090/oz today as a stronger U.S. dollar reduced the impetus to buy the precious metal as a hedge (gold typically moves inversely to the U.S. currency). The greenback rallied to a 10-month high against the euro, after the French and Germans said any package to bailout Greece would likely involve help from the IMF. The news of any IMF involvement is undermining confidence in the European Union and has investors questioning the long-term viability of the euro. The euro also came under pressure in reaction to Fitch Ratings lowering Portugal’s credit rating. While the U.S. dollar could rally and take gold down further in the short run, due to current troubles in Europe, it is unlikely that the U.S. currency will strengthen and gold decline on a consistent basis over the long run. BMO expects gold to be firm over the next two years, with considerable upside risk owing to the massive increases in the U.S. budget deficit. The growing public obligations imply a risk of monetization, which could result in a lower dollar and higher inflation — catalysts for gold investment demand. The U.S. gross federal debt currently stands at around US$12 trillion (83% of GDP) and is projected by the Office of Management and Budget to reach nearly US$20 trillion by 2015 (103% of GDP). Given the lack of any concrete policies on the tax revenue side of the fiscal equation to help balance the budget in the U.S. Congress, growing expenditures and the relatively lofty official GDP growth assumptions, the U.S. debt is likely to be even higher than forecasted by the government. Based on the relationship between the gold price and the federal debt over the last three decades or so, this could be very good news for gold and gold- related assets broadly. In addition, the sorry financial situation of U.S. states, such as California, could mean that a Greek-like debt crisis could engulf America as well. Bottom Line: The current gold and gold equities correction likely represents a buying opportunity for the long term. High leverage gold names are likely to benefit most from future high gold prices. BMO’s gold equity team suggests Harmony Gold (HMY-NYSE, HAR-JSE), Golden Star Resources (GSS-AMEX, GSC-TSX), Barrick Gold ( ABX-NYSE, TSX), Centerra Gold (CG-TSX) and Detour Gold (DGC-TSX), to name just a few, as a way to capitalize on gold’s upside. SKYROCKETING U.S. FEDERAL DEBT SHINES ON GOLD SUSTAINED DOLLAR RALLY UNLIKELY 140 $21,000 $2,200 $22,000 r: -0.70 130 $18,000 $1,925 $19,250 $1,650 $16,500 120 $15,000 R² (adjusted): 0.93 $1,375 $13,750 110 $12,000 Billions Billions $1,100 $11,000 100 $9,000 $825 $8,250 90 $6,000 $550 $5,500 80 $3,000 $275 $2,750 70 $0 $0 $0 1982 1986 1990 1994 1998 2002 2006 2010 2014 1982 1986 1990 1994 1998 2002 2006 2010 2014 Average Annual Gold Price Gross U.S. Federal Debt Trade Weighted USD Gross U.S. Federal Debt This report was prepared by an analyst(s) employed by BMO Nesbitt Burns Inc., and who is (are) not registered as a research analyst(s) under FINRA rules. For disclosure statements, including the Analyst's Certification, please refer to pages 2 to 3.