1. The State Of ECHO

he unprecedented rise in domestic crude oil production

has created tremendous change for the U.S. Gulf Coast

refining market, including an advantageous position for

some midstream logistics companies.

With U.S. domestic production at 7 million barrels

(bbl.) per day, as well as increased Canadian production,

there’s an increasing flood of inland crude creating a bot-

tleneck at the Cushing, Oklahoma, trading hub that

needs alleviation. Many in the industry anticipate a host

of pipeline projects will bring more than 3 million bbl.

per day from Cushing and South Texas to the Gulf Coast,

helping relieve the crude oil stockpile.

But it is possible “the Cushing backlog will essentially

just transfer to Houston,” Sandy Fielden, director of an-

alytics at RBN Energy, tells Midstream Business.

And, Fielden says, terminal operators are currently ex-

panding or building storage terminals equipped with

nearly 19 million bbl. of capacity.

“Some facilities are older, some are new. Some are in

Houston and some are in Louisiana,” he says. “They are

all trying to address the same issue. Someone is going to

need to redistribute the incoming crude, and there is a

lot of money to be made if they are in the right place.”

Expected demand

Aiming to capitalize on this expected demand, Enterprise

Products Partners LP is in the midst of constructing the

ECHO crude oil storage and terminal facility,located out-

side Houston in southeast Harris County, Texas. Of that

expected 19 million bbl. of capacity, Enterprise estimates

that the ECHO facility could have as much as 6 million

bbl. of crude oil storage capacity when completed.

The terminal will be connected to both the Enterprise-

owned Eagle Ford crude pipeline from South Texas and

the Seaway line that runs between Cushing and Freeport,

Texas, once the company completes an ECHO-to-Jones

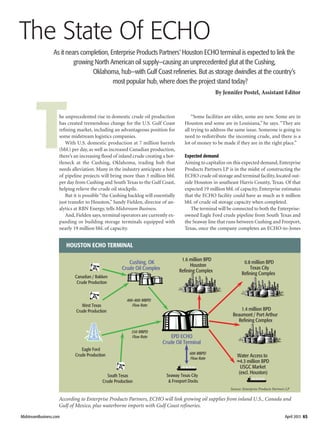

As it nears completion, Enterprise Products Partners’ Houston ECHO terminal is expected to link the

growing North American oil supply—causing an unprecedented glut at the Cushing,

Oklahoma, hub—with Gulf Coast refineries. But as storage dwindles at the country’s

most popular hub, where does the project stand today?

By Jennifer Postel, Assistant Editor

MidstreamBusiness.com April 2013 65

EPD ECHO

Crude Oil Terminal

Cushing, OK

Crude Oil Complex

West Texas

Crude Production

Eagle Ford

Crude Production

South Texas

Crude Production

1.6 million BPD

Houston

Refining Complex

Water Access to

≈4.3 million BPD

USGC Market

(excl. Houston)

Seaway Texas City

& Freeport Docks

Canadian / Bakken

Crude Production

0.8 million BPD

Texas City

Refining Complex

1.4 million BPD

Beaumont / Port Arthur

Refining Complex

400–800 MBPD

Flow Rate

350 MBPD

Flow Rate

600 MBPD

Flow Rate

According to Enterprise Products Partners, ECHO will link growing oil supplies from inland U.S., Canada and

Gulf of Mexico, plus waterborne imports with Gulf Coast refineries.

HOUSTON ECHO TERMINAL

Source: Enterprise Products Partners LP

65-68 Logistics_The State of Echo 3/25/13 12:03 PM Page 65

2. April 2013 MidstreamBusiness.com66

Creek, Texas, pipeline in the third quarter of 2013. Jones

Creek, outside Feeport, is Seaway’s southern terminus.

Once completed, the ECHO terminal will offer ac-

cess to major Texas Gulf Coast refining centers in Texas

City, Pasadena/Deer Park, Baytown and along the Hous-

ton Ship Channel. ECHO will also be connected to the

Enterprise marine terminal at Morgan’s Point on the

ship channel.

“The neat thing about ECHO is it is a pipeline con-

nected to every major refinery in the Houston,Beaumont,

Port Arthur areas and the entire Gulf and East Coasts

through waterborne,” A.J. “Jim” Teague, executive vice

president and chief operating officer of Enterprise’s gen-

eral partner, recently told the Houston Producers Forum.

Enterprise announced in November 2012 that the ini-

tial phase of the storage facility was complete and receiv-

ing deliveries of crude oil.At press time, the facility’s first

three tanks have a total 750,000 bbl. of storage capacity.

And, according to the company, the next expansion phase

is expected to add as much as 900,000 bbl. of storage ca-

pacity, which could be in service as early as the first quar-

ter of 2014. That could bring large potential benefits to

both Enterprise and refiners, according to RBN’s Fielden.

“For Enterprise, the huge potential benefit from the

ECHO terminal, which they have yet to realize, is they

will be able to offer customers a throughput from Sea-

way to Houston and then once in Houston, they will be

able to offer customers a redistribution point to refiners

around the area or an access point to the Houston Ship

Channel, for marine transport,” he says. “For refiners,

storage facilities like ECHO offer a useful staging post to

reliably provide a given amount of crude feedstock on a

consistent basis.”

Light vs. sour

According to Fielden, in the recent past Gulf Coast refin-

ers spent billions of dollars reconfiguring their refineries

to“live on a diet of heavy sour crude.”The influx of com-

petitively priced inland light crude is not really suitable

for these refineries.

“You can run lighter crude, but it produces too much

light distillate that overwhelms the refinery capacity forc-

ing a reduced throughput,” he says. “One way for Hous-

ton refineries to consume more of the competitively

priced light crude is to blend it with heavier grades. And

one of the advantages of having access to storage termi-

nals like ECHO is its blending capabilities.”

Due to the backlog experienced in Cushing, inland

crude prices are depressed, with a price spread of as much

as $20 between West Texas Intermediate (WTI) crude

and North Sea Brent crude. Many in the market, Fielden

says, once believed that ECHO, along with the Seaway

and Keystone pipelines, would miraculously bring inland

prices “back in line with Brent.” But, pricing predictions

can be difficult and, Fielden explains, the old rule of

thought is looking unlikely.

“The market, at the moment, is waiting with bated

breath for new capacity to open up between Cushing and

Houston to reduce the stockpile at Cushing, but so far it

has been a bumpy ride,” he says. “There was a hiccup re-

cently when Enterprise announced a constraint on the Sea-

way pipeline because the takeaway capacity at the Houston

end is restricted until Enterprise completes the Jones Creek-

to-ECHO pipeline.”According to analysts, recent develop-

ments have had an impact on the unpredictability of inland

crude prices, which are set by the WTI-Cushing bench-

mark. There is no guarantee what potential effect the new

terminal will have on pricing,according to Larry Schwartz,

an independent energy and petrochemical consultant.

“Conceptually, if everything is just connected by

pipeline, it should just be pipeline tariff as the differential

plus maybe a little bit for handling,” he tells Midstream

Business. “So what you have is WTI, which is stranded

MidCon; Eagle Ford which is either a parity or above

WTI, and they are competing and trying to get LLS

[Louisiana Light Sweet] prices.”

“The next two years will indeed be challenging for

midstream crude logistics in the Gulf Coast region.

The pace of the changes that have already been

made is remarkable.”

—Sandy Fielden, director of analytics, RBN Energy

65-68 Logistics_The State of Echo 3/25/13 12:03 PM Page 66

3. MidstreamBusiness.com April 2013 67

Traffic congestion

Fielden emphasizes that transfer of Cushing’s congestion

to the Houston-Gulf Coast region is a distinct possibility.

“All of this stuff is just going to come down the line

and then backup in Houston. Right now, Cushing has

roughly 50 million bbl. stored,”he says.“ECHO has 6 mil-

lion bbl., which will not be ready until the end of this year

at the earliest. So with simple math, things are likely to

get backed up in Houston.

“These places must have connectivity, as Enterprise

has found out. If your terminal is not connected to any-

thing then it pretty quickly fills up.”

To alleviate these concerns, Enterprise is working to

complete the line between its Jones Creek terminal and

the ECHO terminal. For now, Fielden says, the crude is

expected to be routed into Houston through the Rancho

Pipeline, which runs from Sealy, Texas, to Houston and

intersects with Seaway at Jones Creek.

Despite these challenges, the future of ECHO and

other Gulf Coast storage terminals appears bright, given

the soaring domestic crude market.

“The next two years will be very challenging for mid-

stream crude logistics in the Gulf Coast region. The pace of

the changes that have already been made is remarkable,”

FieldenexplainedinanRBNEnergyarticletitled,“Gulf Coast

Crude Oil Flood Preparations: The Terminal Operators.”

“Crude terminal operators in the right location with

the right facilities look set to benefit significantly from

the process of rewiring and blending supplies to Gulf

Coast refineries. Hopefully the preparations that these

operators have made in expanded infrastructure will

prove capable of handling the flood of new crude,” ac-

cording to the report. ■

Jennifer Postel can be reached at

jpostel@hartenergy.com or 713-260-5205.

Port Arthur

ECHO Crude Oil Terminal

Connects Eagle Ford, Bakken, Permian,

Midcontinent and imports with Gulf Coast

area refineries and water access

representing more than 8 million barrels

per day of capacity

Build-out up to 6 million barrels of storage

Being considered by NYMEX as a

regional pricing point for Gulf Coast

market

The Seaway Pipeline, which is supported by commitments for as long as 20 years, will have its capacity expanded to a maximum of

850,000 barrels per day of service in the first quarter of 2014.

Source: Enterprise Products Partners LP

65-68 Logistics_The State of Echo 3/25/13 12:03 PM Page 67

![April 2013 MidstreamBusiness.com66

Creek, Texas, pipeline in the third quarter of 2013. Jones

Creek, outside Feeport, is Seaway’s southern terminus.

Once completed, the ECHO terminal will offer ac-

cess to major Texas Gulf Coast refining centers in Texas

City, Pasadena/Deer Park, Baytown and along the Hous-

ton Ship Channel. ECHO will also be connected to the

Enterprise marine terminal at Morgan’s Point on the

ship channel.

“The neat thing about ECHO is it is a pipeline con-

nected to every major refinery in the Houston,Beaumont,

Port Arthur areas and the entire Gulf and East Coasts

through waterborne,” A.J. “Jim” Teague, executive vice

president and chief operating officer of Enterprise’s gen-

eral partner, recently told the Houston Producers Forum.

Enterprise announced in November 2012 that the ini-

tial phase of the storage facility was complete and receiv-

ing deliveries of crude oil.At press time, the facility’s first

three tanks have a total 750,000 bbl. of storage capacity.

And, according to the company, the next expansion phase

is expected to add as much as 900,000 bbl. of storage ca-

pacity, which could be in service as early as the first quar-

ter of 2014. That could bring large potential benefits to

both Enterprise and refiners, according to RBN’s Fielden.

“For Enterprise, the huge potential benefit from the

ECHO terminal, which they have yet to realize, is they

will be able to offer customers a throughput from Sea-

way to Houston and then once in Houston, they will be

able to offer customers a redistribution point to refiners

around the area or an access point to the Houston Ship

Channel, for marine transport,” he says. “For refiners,

storage facilities like ECHO offer a useful staging post to

reliably provide a given amount of crude feedstock on a

consistent basis.”

Light vs. sour

According to Fielden, in the recent past Gulf Coast refin-

ers spent billions of dollars reconfiguring their refineries

to“live on a diet of heavy sour crude.”The influx of com-

petitively priced inland light crude is not really suitable

for these refineries.

“You can run lighter crude, but it produces too much

light distillate that overwhelms the refinery capacity forc-

ing a reduced throughput,” he says. “One way for Hous-

ton refineries to consume more of the competitively

priced light crude is to blend it with heavier grades. And

one of the advantages of having access to storage termi-

nals like ECHO is its blending capabilities.”

Due to the backlog experienced in Cushing, inland

crude prices are depressed, with a price spread of as much

as $20 between West Texas Intermediate (WTI) crude

and North Sea Brent crude. Many in the market, Fielden

says, once believed that ECHO, along with the Seaway

and Keystone pipelines, would miraculously bring inland

prices “back in line with Brent.” But, pricing predictions

can be difficult and, Fielden explains, the old rule of

thought is looking unlikely.

“The market, at the moment, is waiting with bated

breath for new capacity to open up between Cushing and

Houston to reduce the stockpile at Cushing, but so far it

has been a bumpy ride,” he says. “There was a hiccup re-

cently when Enterprise announced a constraint on the Sea-

way pipeline because the takeaway capacity at the Houston

end is restricted until Enterprise completes the Jones Creek-

to-ECHO pipeline.”According to analysts, recent develop-

ments have had an impact on the unpredictability of inland

crude prices, which are set by the WTI-Cushing bench-

mark. There is no guarantee what potential effect the new

terminal will have on pricing,according to Larry Schwartz,

an independent energy and petrochemical consultant.

“Conceptually, if everything is just connected by

pipeline, it should just be pipeline tariff as the differential

plus maybe a little bit for handling,” he tells Midstream

Business. “So what you have is WTI, which is stranded

MidCon; Eagle Ford which is either a parity or above

WTI, and they are competing and trying to get LLS

[Louisiana Light Sweet] prices.”

“The next two years will indeed be challenging for

midstream crude logistics in the Gulf Coast region.

The pace of the changes that have already been

made is remarkable.”

—Sandy Fielden, director of analytics, RBN Energy

65-68 Logistics_The State of Echo 3/25/13 12:03 PM Page 66](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)