1. 1 www.areopa.com

The Challenge

The foundations of all of the economies of the West

have now shifted from an industrial base to a service

and knowledge base. This shift is nearly complete,

and it is irreversible. Economic theories have begun

to reflect this, but theory has been slow to be

translated into practice. There is currently a lack of

consensus around intellectual capital definitions,

management practices and accounting. This Spotlight

focuses on the issues that must be addressed in an

uncertain world and complex business environment

to enable the enterprise to be successful in

implementing intellectual capital management (ICM)

practices.

What is Intellectual Capital Management?

We have defined it as the disciplined approach to the

identification and productive employment of

intellectual capital in the creation of economic value

for the enterprise. It incorporates the management of

intellectual assets, human capital and intellectual

property (IP). It is related to knowledge management,

but emphasizes the valuation and productive

employment of intellectual capital.

Intellectual capital management gives executives a

way of turning "people are our best asset" from lip

service into reality.

Innovation accounts for more than half of

productivity growth worldwide and IC is

the mother of innovation. As a key driver

of economic value for every company, IC

must be identified, managed, measured

and protected.

Source: Gartner Research

Positioning IC Calculation

The importance of financial assets in the

determination of a company’s market value is

decreasing fast and it is equally recognised that non-

financial (or intangible) assets are now the main

drivers of performance and market value. To date

however there exist little or no objective quantitative

measures of intangible assets, and where they are

claimed to exist (e.g. in the valuation of brands,

intellectual property, patents, etc.) they are very

specific and limited in scope.

AREOPA has developed a model for identifying and

quantifying intangibles as components of intellectual

capital (IC). This model serves to evaluate a

company’s return on all the capital it employs, helping

to explain the difference between book and market

value. It also provides guidance as to how and where

management should put its attention to grow the

organisation’s overall IC.

AREOPA positions intellectual capital calculation as a

management tool and not as a simple financial

calculation of the intangible assets of the organization

and thus explaining the difference between book

value and market value. Management wants to

understand the value of the intellectual capital of the

organization. By giving a monetary value to the

intellectual capital, management starts to understand

the value and the impact.

AREOPA’s 4-Leaf Model®

identifies the sources of

added value and competitive advantage in

businesses and in particular of virtual organizations -

collaborative networks of otherwise independent

economic entities - that build their business models

around the internet using minimal financial assets.

The Four IC Classes

The four base classes are Human, Customer and

Structural Capital, plus Strategic Alliance Capital.

The latter gives recognition to the fact that

partnerships, alliances and networks are increasingly

AREOPA

Provoking Innovative Intelligence

Intellectual Capital Management

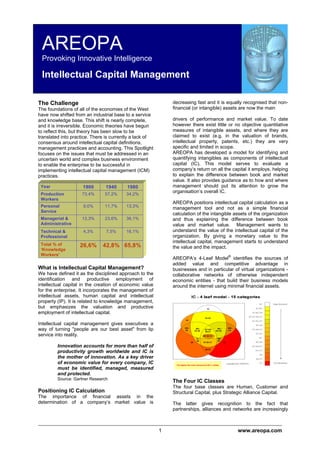

65,8%42,8%26,6%Total % of

‘Knowledge

Workers’

16,1%7,5%4,3%Technical &

Professional

36,1%23,6%13,3%Managerial &

Administrative

13,3%11,7%9,0%Personal

Service

34,2%57,2%73,4%Production

Workers

198019401900Year

65,8%42,8%26,6%Total % of

‘Knowledge

Workers’

16,1%7,5%4,3%Technical &

Professional

36,1%23,6%13,3%Managerial &

Administrative

13,3%11,7%9,0%Personal

Service

34,2%57,2%73,4%Production

Workers

198019401900Year

2. 2 www.areopa.com

important factors of business in the New Economy.

The strength of the alliance or network significantly

impacts the leverage any one company may have in

its market, and therefore affects its value. Think of

how Dell Computers made it big by leveraging on its

suppliers such as Intel, HP, etc. . And Cisco has built

its entire business model around the internet, and

heavily relies on outsourced service providers to fullfil

its business cycles from ordering over manufacturing

to delivery and billing. Although its partners may not

take the front stage, they are nevertheless crucial in

assuring the quality that Cisco sells to its customers.

A second crucial observation is that, apart from

Structural Capital, the base IC classes are in fact

shared capital (Stewart, 1997). For instance, Human

Capital (HC) is shared with its ‘owners’: when the

person leaves, he/she takes his/her skills &

competences, reputation and potential along. Similar

rules apply to both Customer Capital (CC) and

Strategic Alliance Capital (SAC): when the customer

takes his business elsewhere or an alliance breaks

up, the customer’s revenue potential and

partnership’s leverage are lost and a “zero-sum

game” relationship is restored.

However, not all may be lost in such extreme but

realistic scenarios since at least the customers’ name

may remain on the company’ reference list, and a

former partner may still perform as arm’s length

supplier: these indicate that some CC and SAC has

become structural, and is therefore unaffected by the

departure of a customer, respectively strategic

alliance.

The consequence of this is that Intellectual Capital

may flow from one region into another (neighbouring)

region ! And this is where the management of IC

comes into play. It is important for companies to

realize where their IC is situated, and which actions

need to be taken to convert IC that is at risk of being

lost into IC that has become structural; i.e. to

structuralize its Human, Customer and Strategic

Alliance Capital to the maximum extent possible.

IC Building Blocks, elements, variables and

indicators

Studies around IC have managed to reach a

consencus around the building blocks. There seems

to be an agreement that human capital and structural

capital are two of the corner stones, although the

term organisational capital is often used for the latter.

Talking about relational capital the ideas seem to

become a little bit more confused: customer capital is

certainly one of the aspects here, where in some

publications this chapter also comprises allicance and

partner capital. Trying to capture the entire picture,

social and even cultural capital are added to the list.

Once the main blocks are defined, the specialists

descend one step further into the depths of the IC

secrets, summing up all the elements that are part of

the inventory of each major sphere.

The ideas become more dispersed here, but carefull

harvesting yields a list of 100 to 150 elements.

The next development concentrates on the attributes,

variables and parameters that are linked to or

charateristic for the element at stake.

And that is where it stops. IC reporting is primarily

limited to indicators, leading to pertinent question:

“What’s the use of all this?”

Some managers that are confronted with the (sales)

talks from IC promoters are ‘lured’ into starting an IC

exercise, often called: the putting together of an IC

Balance Sheet (Wissensbilanz in Germany and

Austria). All of these projects start with the listing of

chapters and elements and generate or calculate

indicators at best. In many cases these ‘IC Balance

Sheets’ are then used for internal and/or external

communications, i.e. as show pieces to show the

3. 3 www.areopa.com

innovative spirit of the management. And then there

is silence …

What is missing? The answer is simple and twofold:

1. The value of IC assets needs to be expressed in

ONE and the same common denominator, so

that values can be added up and compared, i.e.

money, the only measure known and understood

by everyone;

2. The report format needs to be clear, known and

understood by the average manager. Maybe a

classical (financial) balance sheet format might

fulfil this requirement.

Designing a report in a balance sheet format is

simple. Everybody talks about IC assets, which

means that ordering IC assets in a similar manner as

financial assets on a balance sheet is easy. Financial

assets are financed with equity (shareholder’s

capital) and external funds (banks, financial

institutions, suppliers, creditors, etc.). The ‘financing’

or IC assets can be approached in exactly the same

way. IC assets are either owned by the company

(explicit), whereas other assets are ‘borrowed’ to the

company (tacit). This presentation leads to the

liabilities side of the IC balance sheet.

IC Accounting

If the IC balance sheet is what we want to get to, then

we have to decide what we need to do in order to get

to this report. Applying the basic accounting rules

seems to get us quite far:

1. Designing an IC Chart of Accounts (CoA) is not

complicated because the asset list pretty clear

and complete;

2. IC accounting rules are a bit more complicated,

but looking for the ‘events’ that drive IC value in

line with ‘events’ that drive general accounting

such as incoming invoices and bankstatements

for example should get us there;

3. IC valuation rules are the core of the matter. In

general accounting rules have been defined to

calculate the value of stock, bad debts, foreign

exchange values, and depreciation rates of fixed

assets. Financial accounting is a picture of the

past. IC accounting looks into the future.

The main challenge is to come up with a valuation

system which is transparant, auditable, repeatable

(objective), and … simple. The basic principle is

based on two components:

1. A component covering the bookvalue of the

element, based on items such as acquisition or

contruction costs, depreciation and amortization;

2. A component covering the future potential value

of the element, probably the net present value of

future cash streams.

The former follows the same principles used for

tangible assets, e.g. the building of a new plant

(which is comparable to building knowledge in a staff

member). The latter requires more complex

econometrical formulas based on parameters and

variables typical for each element.

Double Counting

One of the main points of concern in IC accounting is

the question of avoiding double counting. Human

Capital is needed to realise Customer Capital. Adding

up both values may result in double counting the

same potential. The 4-leaf model helps in visualising

this phenomenon.

Are Human Capital Euros equal to Structural

Capital Euros?

Another major concern is the equality of the unit of

measurement used, i.e. the monetary unit of all the

asset values. Expressing all values in Euros for

example does not mean that all these values are of

the same nature. Special care has to be taken to

assure comparability.

Conclusion

A lot has been done, but all remains to be done.

Unless we manage to translate IC into the language

and the format of the manager, the intrest in this area

will remain primarily academic.

Auditors will have to be convinced that IC valuations

are based on sound rules that are transparant,

objective and auditable. But auditors will have to

‘open up’ to the need of the knowledge economy

where the majority of the assets utilised in a company

are no longer to be found on the balance sheet.

AREOPA

Koningin Astridlaan 201 B5

B-2800 MECHELEN

TEL ++32 15 43.32.17

e-mail : info@areopa.com