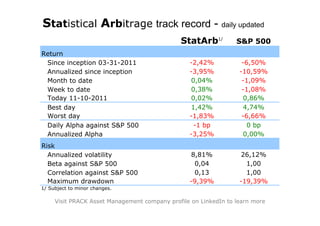

The statistical arbitrage strategy has underperformed the S&P 500 since inception in March 2011, with lower annualized returns and higher volatility. However, it has experienced smaller drawdowns than the market and has a near-zero correlation and beta to the S&P 500, demonstrating its ability to act as a hedge against general market moves.

1. Statistical Arbitrage track record - daily updated

StatArb1/ S&P 500

Return

Since inception 03-31-2011 -2,42% -6,50%

Annualized since inception -3,95% -10,59%

Month to date 0,04% -1,09%

Week to date 0,38% -1,08%

Today 11-10-2011 0,02% 0,86%

Best day 1,42% 4,74%

Worst day -1,83% -6,66%

Daily Alpha against S&P 500 -1 bp 0 bp

Annualized Alpha -3,25% 0,00%

Risk

Annualized volatility 8,81% 26,12%

Beta against S&P 500 0,04 1,00

Correlation against S&P 500 0,13 1,00

Maximum drawdown -9,39% -19,39%

1/ Subject to minor changes.

Visit PRACK Asset Management company profile on LinkedIn to learn more