1. Ongoing Feedback Review

FY14 Ongoing Feedback - MTS YE Audit -- Anderson, Eric M

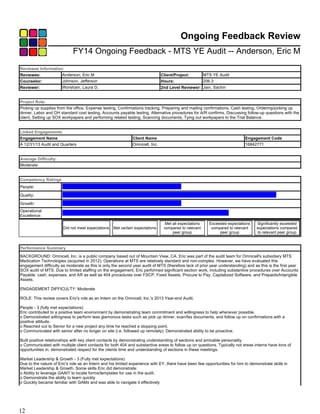

Reviewee Information

Reviewee: Anderson, Eric M Client/Project: MTS YE Audit

Counselor: Johnson, Jefferson Hours: 206.3

Reviewer: Worsham, Laura D. 2nd Level Reviewer: Jain, Sachin

Project Role:

Picking up supplies from the office, Expense testing, Confirmations tracking, Preparing and mailing confirmations, Cash testing, Ordering/picking up

dinner, Labor and OH standard cost testing, Accounts payable testing, Alternative procedures for A/R confirms, Discussing follow-up questions with the

client, Setting up SOX workpapers and performing related testing, Scanning documents, Tying out workpapers to the Trial Balance.

Linked Engagements

Engagement Name Client Name Engagement Code

A 12/31/13 Audit and Quarters Omnicell, Inc. 16842771

Average Difficulty:

Moderate

Competency Ratings

People:

Quality:

Growth:

Operational

Excellence:

Did not meet expectations Met certain expectations

Met all expectations

compared to relevant

peer group

Exceeded expectations

compared to relevant

peer group

Significantly exceeded

expectations compared

to relevant peer group

Performance Summary

BACKGROUND: Omnicell, Inc. is a public company based out of Mountain View, CA. Eric was part of the audit team for Omnicell's subsidiary MTS

Medication Technologies (acquired in 2012). Operations at MTS are relatively standard and non-complex. However, we have evaluated this

engagement difficulty as moderate as this is only the second year audit of MTS (therefore lack of prior year understanding) and as this is the first year

SOX audit of MTS. Due to limited staffing on the engagement, Eric performed significant section work, including substantive procedures over Accounts

Payable, cash, expenses, and AR as well as 404 procedures over FSCP, Fixed Assets, Procure to Pay, Capitalized Software, and Prepaids/Intangible

Assets.

ENGAGEMENT DIFFICULTY: Moderate

ROLE: This review covers Eric's role as an Intern on the Omnicell, Inc.'s 2013 Year-end Audit.

People - 3 (fully met expectations)

Eric contributed to a positive team environment by demonstrating team commitment and willingness to help whenever possible.

o Demonstrated willingness to perform less glamorous tasks such as pick up dinner, scan/fax documents, and follow up on confirmations with a

positive attitude.

o Reached out to Senior for a new project any time he reached a stopping point.

o Communicated with senior after no longer on site (i.e. followed up remotely). Demonstrated ability to be proactive.

Built positive relationships with key client contacts by demonstrating understanding of sections and amicable personality.

o Communicated with multiple client contacts for both 404 and substantive areas to follow up on questions. Typically not areas interns have tons of

opportunities in; demonstrated respect for the clients time and understanding of sections in these meetings.

Market Leadership & Growth - 3 (Fully met expectations)

Due to the nature of Eric's role as an Intern and his limited experience with EY, there have been few opportunities for him to demonstrate skills in

Market Leadership & Growth. Some skills Eric did demonstrate:

o Ability to leverage GAAIT to locate forms/templates for use in the audit.

o Demonstrate the ability to learn quickly

o Quickly became familiar with GAMx and was able to navigate it effectively

12

2. o Understood the purpose/procedures behind a task quickly. Rarely did the senior have to give the same review note twice. For example, when

discussing new EY guidance on testing controls & substantive procedures, the senior discussed the key procedures used to test (inquiry, inspection,

observation, and reperformance). Eric took this discussion and adapted his documentation to ensure it meets EY quality standards. In this he further

demonstrates an understanding of the EY audit methodology that exceeds that of other members of his relevant peer class.

Quality- 5 (Significantly exceeded expectations)

Consistently delivered high-quality work papers with limited supervision; worked on complex areas and consistently produced high quality deliverables.

o As mentioned in the Background section above, Eric completed the Phase 2 SOX testing on multiple sections for MTS. This is a first year SOX audit,

therefore there were no prior period workpapers to use as an example. There was significant executive focus on the quality of testing and

documentation in 404 in current year due to increased regulatory and inspection activities.

• Eric demonstrated his ability to understand the control in question, evaluate the sufficiency of the support, ask relevant questions to the client, and

document his work in a clear manner; his efforts in this area exceed the expectations of those in his peer class.

• Eric was able to demonstrate his comprehension of our audit documentation standards by carrying through initial review comments on one area of

work (FSCP) through to his other controls testing documentation to ensure consistency in quality of his deliverables. Also, he was able to reflect on the

required documentation and point out to his senior places where he believed client evidence provided may be insufficient based on earlier comments

provided.

o Documented tickmark explanations in a clear and concise manner with only brief explanations from the senior. Quickly grasped the purpose of a

procedure and completed documentation to communicate this.

o Accurately identified problems and exceptions. Appropriately escalated problems to supervisor. Was able to clearly communicate/articulate potential

issues.

• Explained potential issues in SURL testing to the senior after the senior left the Tampa location. Even through phone call and without support present,

Eric was able to articulate the potential exceptions to the senior and the client's explanations. Given the limited experience Eric has, this exceeded our

expectations.

• Communicated flagged issues on Expense Testing as well as SURL testing to the senior and then to the Assistant Controller of MTS in a clear

manner. Despite limited experience, Eric was willing to attend and speak up in the client meeting to discuss exceptions we flagged. Was able to answer

follow up questions from both the senior and client promptly, demonstrating an understanding and familiarity of the sections he was assigned.

• Identified several errors in Expense sample testing (inappropriately included some 2012 charges in 2013 expenses), SURL testing (several 2013

liabilities were not accrued as of 12/31/2013), and AR Confirmation alternative procedures (some items in which payment was made before year-end

but the AR balance was still included in AR at year-end).

• In all cases Eric identified the potential issue and immediately raised the items to the senior's attention. In almost all cases, these questions were then

followed up with the client to obtain an explanation of the unusual items. In a couple of these cases, there was a true issue that Eric documented as

such in the workpapers; although none of these errors were above the nominal posting level, Eric's attention to detail and timely follow up allowed the

team to investigate the error and verify it did not prevent a more serious/robust issue. This ability to identify items that require more urgent follow up

impressed the senior and significantly exceeds our expectations of an Intern.

o Eric repeatedly produced work of high quality with limited instruction from the senior. Documented work in a manner that required minimal review

notes and for which it was clear what open items were still being followed up with the client on. Having only a couple of weeks of experience, Eric's

attention to detail and documentation highly impressed the senior.

• Documented detailed expense testing (over 60 samples) after only a brief explanation from the senior. Flagged items for follow up (see section above)

and ensured all other documentation was up to EY standards. Performed similar procedures of SURL, AP, and AR Confirmations/Alternative

Procedures.

• Performed Payroll analytical procedures and payroll reconciliation and documented the steps behind; these procedures require very clear

documentation. Eric's work required minimal review notes and only initial explanations from the seniors.

• In performing cash testing, identified some checks that were marked as "Cleared" in the December 2013 bank statement but still showed up on the

Outstanding Checks in the reconciliation. As a result of Eric's testing, we followed up with the Company on this and gained an understanding of their

"Positive Pay" system with their bank (in which checks not approved by the Company will show as cleared but also backed out if the Company does not

approve the check as a valid check)

• Eric clearly documented this understanding in the Cash workbook so that we can carry forward this understanding to our next year workpapers.

Managed multiple sections assigned to him

o Due to limited staffing on the engagement Eric was one of 2 team members, aside from the senior, responsible for preparing the majority of section

work. Although Eric had many sections assigned to them, and some of them were ongoing throughout (e.g. following up on AR confirmations and

performing SURL testing), Eric approached the workload calmly. Eric discussed tasks assigned with the senior to identify items of priority. Additionally,

Eric proactively reached out to the senior regarding a section if it had not been addressed for some time. One particular example of this pertains to AR

Confirmations. Eric sent out all AR Confirmations and continued to receive responses and update documentation (both for confirmations and alternative

procedures) even after the time he was rolling off the engagement. This exceeded our expectations of the abilities and responsibility of an intern.

On-the-Job Coaching

Given Eric's role and that he has only been with EY for a short period of time, he has had limited opportunities for on the job coaching.

Future Development

Taking into consideration Eric's performance meets or exceeds expectations, we encourage Eric to continue to be proactive and seek out opportunities

to develop his technical knowledge and knowledge of EY GAM. We also encourage Eric to pursue opportunities to expand his knowledge of the client

by getting to understand the nature of the business as well as how it fits in with the parent.

Acknowledgments

Name Signature Date

Reviewer Worsham, Laura D. ELECTRONIC 3/5/2014

2nd Level Reviewer Jain, Sachin ELECTRONIC 3/5/2014

comments: Thanks Eric for your support and dedicated efforts in completing the MTS audit. Looking forward to work with you again.

Reviewee Anderson, Eric M

22