1. (1)

(2004.3) (PROFILE OF INFORMAL SECTOR)

__________________________________________________________________________

MEDIA RELEASE FOR RELEASE ON: 2004-02-11

___________________________________________________________________________

SIZE, STRUCTURE AND PROFILE OF THE INFORMAL RETAIL SECTOR IN

SOUTH AFRICA

The informal retail sector in South Africa is increasingly being acknowledged by

manufacturers and wholesalers as an important delivery channel of goods to consumers. A

report compiled by Prof André Ligthelm of the Bureau of Market Research (BMR) of Unisa

on the characteristics of the informal retail sector, estimated the share of informal trade sector

at approximately R32 billion in 2002. This represents approximately 10 % of retail trade

sales in South Africa.

In contrast with the oftenly expressed notion that the informal and formal sector operates as

two separate ‘economies’ with limited linkages, the study finds considerable linkages

between these two sectors. Linkages are manifested in various ways through, inter alia,

increased product delivery to informal retailers, promotion sales available to them and even

the availability of supplier credit to especially township general dealers. The linkages

contribute considerably to the survival potential of small informal retailers especially due to

the availability of merchandise at more affordable prices, which in essence, allows them to

continue with their trading businesses (the lack of trading stock is often reported as the single

most serious problem encountered by informal retailers).

MORE……

2. (2)

(2004.3) (PROFILE OF INFORMAL SECTOR)

Table 1 shows the type of support received by informal township retailers from suppliers.

Almost nine in every ten informal retailers received deliveries of merchandise. Other types

of support include promotion material, signboards, shop equipment, discount prices and

credit.

TABLE 1

TYPE OF SUPPORT RECEIVED FROM SUPPLIERS

Spaza/tuck

shop

Hawker/

street vendor

General dealer

Type of support in township

% % %

Deliveries 87,9 86,7 89,6

Promotion material 60,8 21,1 53,7

Name on signboard 48,6 4,4 62,7

Shop equipment 32,1 16,7 43,3

Discount prices 19,0 17,8 34,3

Credit 8,6 0,0 13,4

The picture emerging from the research depicts a continuum of informal retailers ranging

from fairly developed businesses to enterprises purely established for household survival

purposes. This wide array of informal retailers creates an excellent foundation for advancing

entrepreneurship and allowing some of the businesses to gradually upgrade to more formal

business structures. At the same time, it should be noted that a large percentage of informal

businesses were established in a nonlucrative business environment and are therefore

operating at a bare survival level.

MORE……

3. (3)

(2004.3) (PROFILE OF INFORMAL SECTOR)

This continuum of fairly established to survivalist businesses is clearly identifiable by type of

business. The following three types were identified in the study, namely township general

dealers, spaza shops and hawkers. Township general dealers seem to be far more established

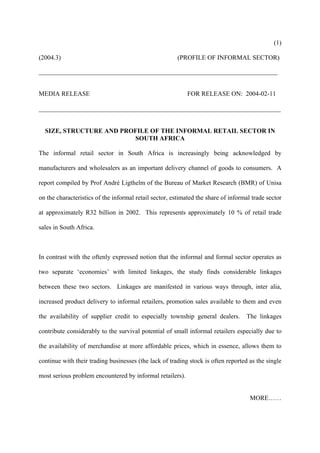

than hawkers. Spaza shops occupy more or less a middle position. Figure 1 shows the

response to the question ‘Will you accept a job in the formal sector if offered today?’

Interesting to note that more than a third (36,6 %) of hawkers perceived their business

endeavour as a permanent career path. The figure for township general dealers is 76,8 % and

for spaza owners 57,2 %.

FIGURE 1

PERCENTAGE OF OWNERS WHO WOULD NOT ACCEPT A JOB IN THE

FORMAL SECTOR

76.8

57.2

36.6

0 20 40 60 80 100

Hawker/street

vendor

Spaza shop

General dealer

Percentage

The relative stability in the informal trade sector is also confirmed by the survival rate of

various types of businesses. The percentage of retailers in operation for longer than five

years are:

MORE……

4. (4)

(2004.3) (PROFILE OF INFORMAL SECTOR)

• General dealers : 63,7 %

• Spaza shops : 36,0 %

• Hawkers/street vendors : 19,0 %

SIZE, STRUCTURE AND PROFILE OF THE INFORMAL RETAIL SECTOR IN

SOUTH AFRICA (Research Report no 323) was compiled by Prof André Ligthelm of the

Bureau of Market Research. The report of 90 pages is obtainable from the BMR, P O Box

392, Unisa, 0003.

END

Date of release: 2004-02-11

___________________________________________________________________________

Professional enquiries: Other enquiries

Prof AA Ligthelm Mrs M Lamb

Bureau of Market Research Bureau of Market Research

University of South Africa University of South Africa

PO Box 392 P O Box 392

UNISA UNISA

0003 0003

Tel (012) 429-3151 Tel (012) 429-3070

Fax (012) 429-3170 Fax (012) 429-3170

E-mail: ligthaa@unisa.ac.za E-mail: lambm@unisa.ac.za