1. Streamflow Analysis References and Acknowledgements:

Comparing Intermittent Streams with a Cointegration Approach

Dexen Xi, Charmaine Dean, Lihua Li

University of Western Ontario, Statistical and Actuarial Sciences

Unit Root TestsIntroduction of the Study

• Intermittent streams are formed seasonally from melting snow

and rainfall. They are common in the southern Canadian Prairie

Provinces and have significant agricultural and ecological

purposes.

• A current research topic is to classify (or regionalize) the

intermittent streams into groups by using records from

Environmental Canada, so that the flow of streams can be

compared for hydrological purposes.

• Two major challenges are:

1. daily flows are dependent and expected to be AR(1)

2. Tests related to methods of classification may have poor

performance

Cointegrated Time Series

• Working with Robert Engle, Clive Granger won the Noble Prize in

2003 for the development of the concept of cointegration

• Intuitively, if the residuals (denoted by 𝑧𝑡) obtained from the linear

combination of two time series (𝑥𝑡 and 𝑦𝑡) are stationary, then the

two time series are cointegrated and thus vary similarly.

• The stationarity of the residuals can be tested by various unit root

tests.

Objectives

• Investigate into various unit root tests used in cointegration

analysis that assesses whether two time series vary similarly.

• Identify whether the streamflows of any two intermittent streams

from the Reference Hydrometric Basin Network (RHBN) on the

Canadian Prairies are cointegrated in a given year.

• Let ∆𝑧𝑡 = 𝑧𝑡 − 𝑧𝑡−1. To test that an AR(1) time

series 𝑧𝑡 is non- stationary several tests are

considered.

• Consider ∆𝑧𝑡 = 𝜋𝑧𝑡−1 + 𝜀𝑡. The Dickey-Fuller

test constructs a test of:

𝐻0: 𝜋 = 0

𝐻1: 𝜋 < 0

• The augmented Dickey-Fuller (ADF) test

improves the test by including more lags

∆𝑧𝑡 = 𝜋𝑧𝑡−1 +

𝑗=1

𝑘

𝛾𝑗∆𝑧𝑡−𝑗 + 𝜀𝑡

• An extreme test statistic will suggest that

𝜋 < 0. We reject the null and thus conclude

that 𝑧𝑡 is stationary, which means that 𝑥𝑡 and

𝑦𝑡 are cointegrated.

• A non-extreme test statistic will suggest that

𝜋 = 0. We fail to reject the null and thus

conclude (have no evidence against) 𝑥𝑡 and

𝑦𝑡 are not cointegrated.

• The augmented Dickey-Fuller (ADF) test is the

foundation of three other unit root tests

discussed in the study, namely:

PP: The Phillips-Perron test

ERS: The Elliott-Rothenberg-Stock test

SP: The Schmidt-Phillips test

• A simulation study is conducted to study the

properties of the ADF test and the three tests

listed above.

Simulation Setup:

1. Generate 3 time series of length 1000

𝑇1 from ARIMA(1,1,0)

𝑇2 from ARIMA(1,1,0) + a white noise

𝑇3 by adding a white noise to 𝑇1

2. Test if 𝑇1 is cointegrated with 𝑇2 or 𝑇3 and

compute the proportions of cointegrated

pairs in 500 repetitions, with the alpha level

set at 0.01, 0.05 and 0.1.

3. Examine the variations of the proportions by

increasing the standard deviation of the

white noise from 1 to 50.

• The data used in the analysis contain the

daily flows (𝑚3

/𝑠𝑒𝑐) during Mar to Oct of 16

RHBN streams from 1975 to 2010.

• All 16*36 = 576 series are compared in pairs

to assess cointegration using the ERS test.

• Test statistics for all comparisons of all other

streams with stream 4 (Figure 3) and

streamflows of streams 4, 3, and 6 in 1986

(Figure 4) are provided as examples of

comparisons conducted.

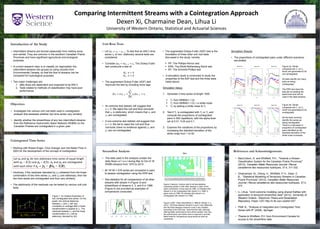

Figure 1: An intuitive illustration of

two cointegrated time series. On the

graph, the vertical distances

between 𝑥𝑡 and 𝑦𝑡 will vary

constantly on average after a linear-

transformation is applied to 𝑥𝑡. The

residuals between 𝑦𝑡 and the linear

transformation of 𝑥𝑡 will be

stationary, denoted by I(0).

Simulation Results:

• The proportions of cointegrated pairs under different scenarios

are plotted.

Figure 2b: Series

compared are 𝑇1 vs 𝑇3,

which are generated to be

cointegrated.

All the tests correctly

identify the series as

being cointegrated.

There is a decrease in

proportion of cointegrated

pairs identified as the

standard deviation of the

white noise increases.

Figure 2a: Series

compared are 𝑇1 vs 𝑇2,

which are generated to be

not cointegrated.

All tests identify too many

pairs as being

cointegrated.

The ERS test does the

best job at meeting the

alpha level and will be

used in the data analysis.

Figure 3 (above): Contour plot for all test statistics

comparing stream 4 with other streams in each of the

years considered. A blue area at (1986, 3) indicates that

stream 4 is not cointegrated with stream 3 in 1986. A

green area at (1986, 6) indicates that stream 4 is

cointegrated with stream 6 in 1986.

Figure 4 (left) : Daily streamflows in 1986 for stream 4, 3,

and 6. The flows between streams 4 and 3 vary differently,

and the flows between streams 4 and 5 vary similarly

according to the ERS test. Note that this test, although

offering better performance than others studied, has only

fair performance and further work is required to provide

better tests for comparisons using series as short as

considered.

Let 𝒙 𝒕 and 𝒚 𝒕 be non-stationary time series of equal length

with 𝒙 𝒕 ~ 𝑰(𝟏) and 𝒚 𝒕 ~ 𝑰(𝟏). 𝒙 𝒕 and 𝒚 𝒕 are cointegrated

with each other if 𝒛 𝒕 = 𝒚 𝒕 − 𝜷𝒙 𝒕 ~ 𝑰(𝟎).

• MacCulloch, G. and Whitfield, P.H., "Towards a Stream

Classification System for the Canadian Prairie Provinces"

(2012). Canadian Water Resources Journal / Revue

canadienne des ressources hydriques, 37:4, 311-332

• Ghahramani, M., Zheng, H., Whitfield, P. H., Dean, C.

B., "Statistical Modelling of Temporary Streams in Canadian

Prairie Provinces" (2012). Canadian Water Resources

Journal / Revue canadienne des ressources hydriques, 37:4,

373

• Li, Lihua, "Joint outcome modeling using shared frailties with

application to temporal streamflow data" (2013). University of

Western Ontario - Electronic Thesis and Dissertation

Repository. Paper 1257.http://ir.lib.uwo.ca/etd/1257

• Pfaff, B., "Analysis of Integrated and Cointegrated Time

Series with R" (2008). Springer.

• Thanks to Whitfield, P.H. from Environment Canada for

access to the streamflow data.