Recommended

More Related Content

Similar to Mapa de ideas principales y secundarias del IFAC ingles

Similar to Mapa de ideas principales y secundarias del IFAC ingles (20)

Recently uploaded

Recently uploaded (20)

Mapa de ideas principales y secundarias del IFAC ingles

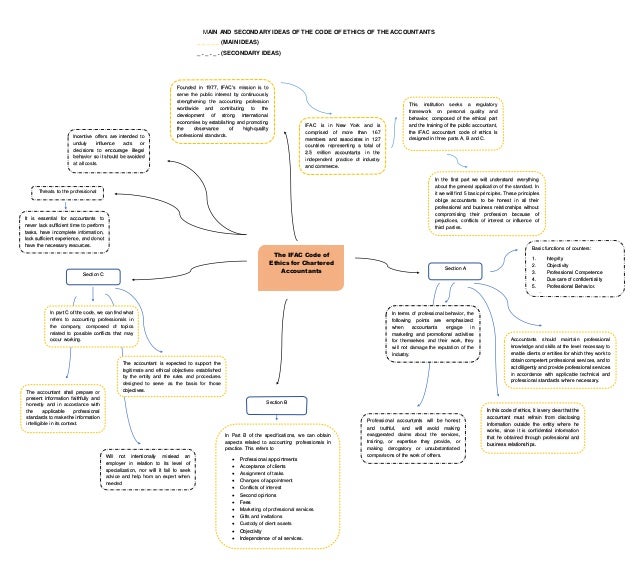

- 1. MAIN AND SECONDARY IDEAS OF THE CODE OF ETHICS OF THE ACCOUNTANTS _ _ _ _ _ (MAIN IDEAS) _ . _ . _ . (SECONDARY IDEAS) The IFAC Code of Ethics for Chartered Accountants Founded in 1977, IFAC’s mission is to serve the public interest by continuously strengthening the accounting profession worldwide and contributing to the development of strong international economies by establishing and promoting the observance of high-quality professional standards. Basic functions of counters: 1. Integrity 2. Objectivity 3. Professional Competence 4. Due care of confidentiality 5. Professional Behavior. In the first part we will understand everything about the general application of the standard. In it we will find 5 basic principles. These principles oblige accountants to be honest in all their professional and business relationships without compromising their profession because of prejudices, conflicts of interest or influence of third parties. This institution seeks a regulatory framework on personal quality and behavior, composed of the ethical part and the training of the public accountant, the IFAC accountant code of ethics is designed in three parts A, B and C. IFAC is in New York and is comprised of more than 167 members and associates in 127 countries representing a total of 2.5 million accountants in the independent practice of industry and commerce. Section B In this code of ethics, it is very clear that the accountant must refrain from disclosing information outside the entity where he works, since it is confidential information that he obtained through professional and business relationships. In terms of professional behavior, the following points are emphasized: when accountants engage in marketing and promotional activities for themselves and their work, they will not damage the reputation of the industry. Professional accountants will be honest and truthful, and will avoid making exaggerated claims about the services, training, or expertise they provide, or making derogatory or unsubstantiated comparisons of the work of others. Accountants should maintain professional knowledge and skills at the level necessary to enable clients or entities for which they work to obtain competent professional services, and to act diligently and provide professional services in accordance with applicable technical and professional standards where necessary. Section A It is essential for accountants to never lack sufficient time to perform tasks, have incomplete information, lack sufficient experience, and do not have the necessary resources. In part C of the code, we can find what refers to accounting professionals in the company, composed of topics related to possible conflicts that may occur working. The accountant is expected to support the legitimate and ethical objectives established by the entity and the rules and procedures designed to serve as the basis for those objectives. Section C In Part B of the specifications, we can obtain aspects related to accounting professionals in practice. This refers to Professional appointments Acceptance of clients Assignment of tasks Changes of appointment Conflicts of interest Second opinions Fees Marketing of professional services Gifts and invitations Custody of client assets Objectivity Independence of all services. Will not intentionally mislead an employer in relation to its level of specialization, nor will it fail to seek advice and help from an expert when needed The accountant shall prepare or present information faithfully and honestly and in accordance with the applicable professional standards to make the information intelligible in its context. Threats to the professional Incentive offers are intended to unduly influence acts or decisions to encourage illegal behavior so it should be avoided at all costs.