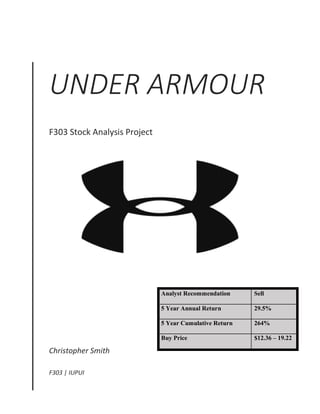

1. Analyst Recommendation Sell

5 Year Annual Return 29.5%

5 Year Cumulative Return 264%

Buy Price $12.36 – 19.22

UNDER ARMOUR

F303 Stock Analysis Project

Christopher Smith

F303 | IUPUI

2. Smith 2

Under Armour (UA) does not currently pay a dividend. Calculated FCFE for 2015 is

$0.46 per share, while for 2014 was $1.59 per share. The greatest differences that caused this

effect were a decrease in Working Capital (2014: $1127.8mm; 2015: $1020.0mm) and a much

higher Capital Spending per share (2014: $0.33, 2015: $0.69). The company has been able to

add to their bottom line for several of the past years, as noted later. Management has been able

to use those profits to purchase more assets, which in turn generate more profit. By not paying

out any dividends, UA has produced new lines of business that are continuously growing

globally.

The intrinsic value is $2.65 per share. With a price of $38.30 as of 10/28/2016, this price

seems very high. Further recommendation will be made after more data is analyzed from both

Under Armour and its competitors.

Under Armour’s mission is to “make all athletes better through passion, design, and the

relentless pursuit of innovation” (Under Armour, Inc.). CEO Kevin Plank opened shop in 1996

as a maker of premium quality compression t-shirts. After going public, revenues soared in the

high-performance apparel, footwear, and accessories line, making Under Armour a global

competitor.

Sources of revenue stem from retailors worldwide, but the largest amount of sales occur

at Dick’s Sporting Goods (ticker: DKS), bringing in over $3.1bb in sales during 2015. This is

bolstered with trendy advertising through sponsorships with big name players, such as Stephen

Curry, Jordan Spieth, Tom Brady, and Clayton Kershaw. These sponsorships dually enhance the

brand by maintaining relationships with younger customers.

3. Smith 3

Under Armour has a bright outlook. Revenues have a track record of increasing 20%

year-over-year, thereby leaving large room for error in expenditures. UA has pressure to spend

more for their premium materials, which lowers the bottom line. They are currently opening

stores, signing new and maintaining current endorsement deals, entering new market niches, and

launching new products, which places them as a growth company in the business cycle. A major

concern is a trailing P/E of 74.4. This can be viewed as a high price to pay for a company, but

investors seem not to mind considering that the stock has a history of trading for a high multiple.

Investors are optimistic about the leadership and direction of Under Armour and can expect years

of revenues and endorsement deals ahead. There is plenty of room to grow in footwear, direct-

to-consumer distribution, overseas expansion, and women and children lines. While the

executive staff is focused on American adult male athletes, there are a plethora of opportunities

throughout the world where their products are desired.

Under Armour’s main competitors are Nike (NKE), Adidas (ADDYY), and Lululemon

(LULU). The competitors are in the late growth and early maturity stages of the business

lifecycle, and while the industry itself is growing, they are losing market share to UA. They are,

however, more cost effective compared to UA, thereby providing lower prices on many products,

reducing prices to customers, and passing the savings on to shareholders. With much of the

competition already in footwear, direct-to-consumer distribution, overseas expansion, and

women and children lines, UA has a runway of growth to catch up and become the sole global

leader in the industry.

Capital expenditures over the previous three years have grown substantially. From 2013

through 2015 UA capex spending per share was $0.21, 0.33, and 0.69. This is an average

increase of nearly 64% each year, far exceeding the 20% revenue growth the company has

4. Smith 4

sustained over the same period. The projected capital expenditures for 2016 are $0.85 per share,

a meager 23% over last year. This can be attributed to the 50 current sponsorships and

expansion into new lines of business and geographical areas. Overseas sales are seeing difficulty

in converting cash back to USD since the dollar is very strong compared to other currencies

(Value Line). This is resulting in a decline in bottom-line for investors as it would be the

equivalent to marking down prices in the US.

Lululemon has lowered profit margins by creating return business in gyms and yoga

studios, as well as increasing sales and sponsorships to little league and local teams (Walsh).

Nike dominates the industry with a large advertising budget, endorsements of 46 of the 65

college major football teams, and the sole uniform manufacturer for the NFL. Adidas also

signed some big names in endorsement deals, such as Lionel Messi, Derrick Rose, and Damian

Lilliard (Total).

The endorsement deals are having a positive effect on both top and bottom lines, but it is

difficult to determine the direct effect since the data is not publicly published. Overseas sales are

increasing; therefore, it is necessary to invest in overseas stores and awareness. As international

partners, it is necessary to sponsor more organizations and athletes worldwide.

Using the DuPont Analysis method with 2015 data, ROE for UA is 14%; NKE is 31%;

and LULU is 26% (Yahoo! Finance). Under Armour is well below the industry average, which

means they need to either boost their bottom line or reduce their equity. From 2013 through

2015, cumulative changes in ROE are as follows: UA -1%, NKE +6%, LULU 0%. UA is

struggling to improve its bottom line, even though its revenues are increasing at roughly 20% per

year. UA has been increasing its net income and equity almost proportionately, which results in

a flat line for earnings per share. How high can the price per share go before investors decide

5. Smith 5

that they are paying too much for the same EPS year after year? This is now an interpretation of

price-to-earnings, which are as follows as of 10/28/2016: UA is trading at 77.4 times earnings;

NKE at 23.68; and LULU at 29.41 (Yahoo Finance). Simply looking at ROE would say that

there is more growth potential than Nike; however, a peek at the P/E shows how expensive the

stock really is. On the flip side, Nike has had tremendous growth in comparison, and the stock

price is trading at a much cheaper multiple. Lululemon is sitting in the middle of both. There

seem to be tremendous growth opportunities for both UA and LULU in the coming years

compared to NKE. This stock is overpriced, even though there is skepticism around the

tremendous growth potential. However, a few good deals could send any of these companies’

top and bottom lines soaring.

PEG shows the price of a stock in relation to its earnings growth. UA is valued at a PEG

of 252.20, while NKE is 401.36 and LULU is 216.25. Looking to forward earnings, this would

imply that LULU is the cheapest by this measure and NKE is the most expensive. UA falls in

the middle for the industry.

VRE shows a picture opposite in this case. The return on equity for the price should be

relatively high. The VRE for Nike is nearly 7 times and Lululemon approximately 6.7 times that

of Under Armour. This makes both competitors much more attractive in terms of future return

rates. UA would need to either boost its ROE or investors would need to pay a much smaller

multiple of earnings for the stock. On the other hand, NKE and LULU are cheap and have a

much larger upside potential in the short-term. This supports an argument that Under Armour is

overpriced.

6. Smith 6

After analyzing Under Armour as a company, analyst recommendations is sell.

The high price cannot be compensated with a speculative high growth potential. A control of the

high-end and performance segments of athleisure wear will eventually control more cash flow

than the low-end segment, as the old premium becomes the new norm. Under Armour has the

products to accomplish this, but the costs of materials are weighing heavily on their bottom line.

Until management can reduce costs while maintaining the growth in revenues, this stock is

overvalued, even though it is overweight. Value Line sees target estimates of 45 – 70 for the

years 2019 through 2021, which is a simple cumulative return of just 7.7% to 77.5%. While

there is exceptional upside potential, there are also other options that give similar returns at a less

expensive price.

7. Smith 7

Works Cited

“LULU Key statistics | lululemon athletica inc. Stock - Yahoo finance.” Yahoo! Finance. 01

Dec. 2016. Web. 1 Dec. 2016. <http://finance.yahoo.com/quote/LULU/key-

statistics?p=LULU>.

“NKE key statistics | Nike, Inc. Common stock stock - Yahoo finance.” Yahoo! Finance. 01 Dec.

2016. Web. 1 Dec. 2016. <http://finance.yahoo.com/quote/NKE/key-statistics?p=NKE>.

Totalsportek2. "Biggest Athlete Endorsement Deals In Sports History." TOTAL SPORTEK.

2016. Web. 01 Dec. 2016. <http://www.totalsportek.com/money/biggest-endorsement-

deals-sports-history>.

“UA Income Statement.” NASDAQ.com. Web. 01 Dec. 2016.

<http://www.nasdaq.com/symbol/ua/financials?query=income-statement>.

“Under Armour, Inc. – About Under Armour.” Under Armour, Inc. – About Under Armour.

Web. 01 Dec. 2016. <http://www.uabiz.com/company/about.cfm>.

Value Line. "Value Line - The Most Trusted Name in Investment Research." Value Line - The

Most Trusted Name in Investment Research. Web. 01 Dec. 2016.

<https://research.valueline.com/secure/research#list=recent&sec=company&sym=ua>.

Walsh, Tamara. "3 Surprising Ways Lululemon Athletica Is Driving Sales Growth Today." The

Motley Fool. 2014. Web. 01 Dec. 2016.

<http://www.fool.com/investing/general/2014/08/28/3-surprising-ways-lululemon-

athletica-is-driving-s.aspx>.