1.

Tanger Factory Outlets (NYSE: SKT) Mohit Hajarnis & Carter Chen

1

Tanger Factory Outlets owns and operates, or has

part ownership in, 46 outlet malls in 26 states and

Canada, located along highways or near popular

tourist destination. Tanger is the only pure-play

outlet center REIT, and the outlet format offers

unique advantages to tenants and their customers,

and by extension, Tanger’s investors.

Investment Thesis

• Tanger is a well-run business with strong brand

value, superior corporate strategy, and

management.

• Tanger has stewarded capital well in comparison

to its competitors: a low DSCR and debt/equity

ratio give Tanger room to grow using extra debt

without compromising shareholder’s equity.

• Demand for outlet space has increased

dramatically since 2008 because retailers have

come to view outlets as part of their market

segmentation strategy, not just a channel to off-

load extra inventory.

• Tanger’s long-lived leases are locked-in at low

historical rates, but a historical premium of 20%

for renewals and 70%+ premium for re-tenanted

leases will drive revenue through 2018.

• Tanger’s intrinsic value is obscured by

accounting and valuation intricacies.

Recommendation: Long-term Buy

2

Key Drivers

• Outlet sales have grown at 10% CAGR since

2008, and rent has grown at 3.1% CAGR

• Tanger generates revenues across economic

cycles: recessions drive consumers to seek

discounts at outlet stores.

• Tanger’s rents represent ~ 5% of tenant costs

(2Q2014), compared to mall rents, which

represent ~ 12% of tenant costs.

• Tanger benefits from economic moats arising

from barriers to entry and brand value.

Bulls Say

• Tanger is focusing on saturating the US outlet

market while competitors Simon and GGP are

focusing on saving their mall franchises.

• Tanger has maintained 95%+ occupancy for the

past 10 years.

• Tanger has a strong pipeline of ~1.5M square

feet GLA in the next five years, which is already

financed and will require no additional debt.

Bears Say

• Tanager faces threats from e-commerce sites

like Gilt.com, which offers similar discount sales

on luxury goods.

• Discounting luxury merchandise is an

unsustainable business because it damages

brand value and cannibalizes sales.

Summary

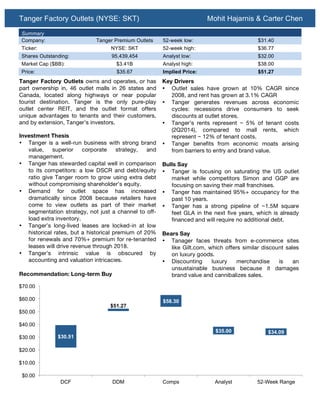

Company: Tanger Premium Outlets 52-week low: $31.40

Ticker: NYSE: SKT 52-week high: $36.77

Shares Outstanding: 95,439,454 Analyst low: $32.00

Market Cap ($BB): $3.41B Analyst high: $38.00

Price: $35.67 Implied Price: $51.27

$30.51

$51.27

$58.30

$35.00 $34.09

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

DCF DDM Comps Analyst 52-Week Range

2.

Tanger Factory Outlets (NYSE: SKT) Mohit Hajarnis & Carter Chen

3

Business Overview & Analysis

Business Model

Tanger generates revenues by collecting base rents,

percentage rents, and expense reimbursement from

its tenants. Base rents represent minimum rent

charged per square foot to tenants. The average

base rental rate has grown at 1.5% between 2012

and 2013, and 7.4% between 2011 and 2012. This is

largely because Tanger does not adjust rents yearly,

but rather provides long-term fixed leases, which are

attractive to established tenants looking to manage

costs. The growth in base rent is reflective of lease

renewals and re-tenanting (footnote for definition): In

2012, 2.1 M sq ft of space was renewed or re-

tenanted, and in 2011, 2.0 M sq ft was renewed or

re-tenanted. The rates Tanger charges on renewed

or re-tenanted leases reflect wider demand for

Outlet mall space and various economic factors. In

2013, average new rent for re-tenanted space was

$30.57, less than the $31.72 new rent in 2012. This

drop is reflective of additional supply in the market

from expansions by Tanger and its competitors.

Tanger also collects percentage rent: a percentage

of tenants’ sales volume above predetermined

levels. As base rents are fixed higher, the

predetermined levels are set higher as well –

reflecting Tanger’s commitment to keeping tenant

costs low. Tanger’s second largest revenue segment

is Expense Reimbursements. Contractually, tenants

are responsible for certain common expenses such

as common area maintenance, insurance, tax,

advertising, and other property management

4

expenses. These expenses are offset by equivalent

property maintenance and some SG&A expenses –

and have no effect on Net Income; if expense

reimbursements increased or decreased, certain

maintenance and SG&A expenses would increase or

decrease equivalently. Nonetheless, the expense

reimbursement strategy helps widen Tanger’s

margins and keep base rents – the most observed

metric – low.

Strategy

Tanger’s strategy is centered on capturing strong

macro fundamentals (see page 4), conservative

business practices and capital stewardship, and

strong property development.

One of Tanger’s strengths as a business is the

constant demand for Outlet stores across economic

cycles and fashion preferences. Despite the sharp

downturn in 2007 – 2009, Tanger continued to grow

its dividend because consumers switched to

shopping at Outlets for discounted brands instead of

department stores. Tanger’s tenants’ ability to deliver

savings for customers drives additional business

during economic turmoil, and provides counter-

cyclical drivers for growth. Additionally, Tanger’s

portfolio is immune to changes in fashion: its largest

tenants are retailers with experience in fashion and

span the fashion spectrum: Gap, Banana Republic,

Old Navy, Tommy Hilfiger, Nike, Nautica, and Polo

Ralph Lauren. Additionally, it has been refreshing its

portfolio with new brands such as H&M, Forever 21,

$0

$5

$10

$15

$20

$25

$30

$35

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

TTM

$/Sq.Ft.

$MM

SKT Historicals

Total Revenues

FFO

Dividends

Rev per Square Foot

FFO per Square Foot

3.

Tanger Factory Outlets (NYSE: SKT) Mohit Hajarnis & Carter Chen

5

and Under Armour (3Q 2014 Earnings Call).

According to management, as business in a brand

dies down, business in another brand picks up;

according to CEO Steven Tanger, “For every Coach

there is a Michael Kors.”

Tanger is unique amongst competitors Simon and

GGP, which operate malls and outlets under

individual names, because it operates all of its

outlets under the Tanger brand. The brand has

generated value with retailers and consumers, as

demonstrated by its industry leading occupancy

rates and traffic growth. Tanger has maintained

occupancy greater than 98% for the past three

years, because Tanger maintains a strong brand.

Additionally, Tanger has built strong retailer

relationships over its 30+ year history; the typical

Tanger tenant is a large national chain, and stable

over the long term. This insulates Tanger from

bankruptcies and fluctuations in consumer

preferences. Additionally, it eliminates the need for a

provision for doubtful accounts, which competitors

Simon and GGP have needed to account for loses

from tenants going out of business. Tanger’s long-

term leases provide value to tenants through locked-

in rates and managed costs, making them an

attractive partner to retailers. Tanger’s percentage

rentals have also increased over the last three years

– reflective of “higher tenant sales,” and Tanger

brand value with shoppers.

REITs can be a risky investment because capital

mismanagement can wipe out common equity and

suffocate strong revenues with high interest

payments. However, Tanger’s management is

notably conservative, and a strong asset for

shareholders. Tanger focuses on growth solely in the

United States and Canada, seeking “under-served

markets” as sources of future growth, while

competitor Simon has undertaken a joint venture in

China to expand its footprint. While the risk/reward

may be higher for Simon, Tanger’s management has

been dependable in delivering consistent returns to

shareholders. Since its IPO, Tanger has increased its

dividend every single year – even through the

financial crisis. According to Morningstar, Tanger

has developed roughly 10% ROREA for the past 15

years, moving between 7.8% in 2003 to 12.3% in

2002. The highly dependable nature of Tanger’s

management is reflective of its roots: current CEO

Stephen Tanger founded the business alongside his

6

father, Stanley Tanger in 1981, and the company has

the longest history in the outlet business: 33 years.

Stephen Tanger has been in senior management

positions at Tanger since 1986, and was paid 61%,

79%, and 67% of total compensation in restricted

stock units in 2011, 2012, and 2013, respectively –

reflecting a “skin-in-the-game” mentality.

Tanger has consistently grown its property portfolio

by targeting specific markets that would be best

served by an outlet mall. Management considers a

variety of factors in building or acquiring new

properties. The typical market has an average

household income of $65,000, access to major

highways, excellent visibility, or sees at least 5

million visitors a year. The company typically adds

between 600K and 700K square feet every year, and

has expanded consistently over the past five years.

Simultaneously, the company has maintained strong

financial health by reducing Debt/Equity from 5.20X

in 2008 to 1.95X in 2010, and then slowly increasing

it to 2.54X in 2013. The slow, yet consistent,

expansion of Tanger’s portfolio reflects its

commitment to manageable growth without

overextending the balance sheet. The company is

committed to long-term growth: while interest rates

are low and the company can refinance or borrow, it

is investing in new properties and a strong “shadow

pipeline” of properties – promising greater revenues

in the future.

This commitment to strong capital stewardship is

one of Tanger’s defining traits. Tanger owns 44

(including joint ventures) outlet properties, while

Simon owns 66, but Tanger has a superior DSCR

(2.46X vs. 2.12X), and Debt/Equity ratio (2.54X vs.

4.03X). Additionally, ~ 80% of Tanger’s debt is fixed.

Tanger has stewarded capital much better than its

competitors; REITs are troublesome for some

investors because they often issue new shares to

fund projects because they have very little retained

earnings. Tanger has diluted common equity twice in

the past 10 years: July 2011 and August 2009 for a

total of $244.1 M. However, Tanger’s competitors,

Simon and General Growth Properties, have issued

over $350 M in preferred shares to special investors

over the past 10 years, and declared bankruptcy –

wiping out common equity, respectively.

However, this conservative leadership has sacrificed

opportunities for additional return in return for

4.

Tanger Factory Outlets (NYSE: SKT) Mohit Hajarnis & Carter Chen

7

additional risk. Tanger’s focus on North American

expansion has caused it to ignore foreign expansion

into markets like China and the Middle East, where

competitors, like Simon, have opened new outlets.

Tanger has sufficient room in its balance sheet to

raise debt and take on riskier, high-yield projects.

Additionally, by focusing on the business and long-

term growth (a positive, no doubt), the company is

ignoring medium term investors by front-loading

Capital Expenditures and diluting Free Cash Flow.

Although this strategy guarantees bigger dividends

for long-term shareholders, it colors the market’s

perception of the company’s long-term profitability,

leading the market to price the company at a

discount to its peers.

Industry Overview

The modern outlet center first appeared in the early

1970s and outlet stores have been an effective and

unique distribution channel for retailers ever since.

Today, the US is home to 368 outlet centers, housing

~13,000 stores for a total of 78 million square feet of

retail space. The first factory stores—built in the

1930s—were established to unload excess inventory

and damaged goods. The value proposition was

simple: provide a channel to dispose of problem

merchandise that is remote enough from flagship

stores so it does not dilute brand value. That value

proposition still exists today: brands like Nike use

outlets to sell hard-to-move merchandise, i.e. shoes

with flashy colors or abnormal sizes. But the value of

outlet malls has vastly expanded since then. The

central value proposition of the modern outlet center

comes from effective price discrimination. Outlet

centers are simply made and remote enough to

8

avoid patronage from affluent costumers. However,

bargain hunters will make the hike for the discounted

merchandise (the average discount at an outlet store

was 38% in 2012).

Merchandise varies, but effective costumer

segmentation remains the driving force behind

retailers’ selections of offerings. To this effect,

retailers offer a variety of goods in their outlet stores.

These range from items identical to those in their full

price channels, to items specifically made for outlet

stores—Brooks Brothers 346 line is a good example

of this.

The outlet industry continues to grow at a healthy

pace. US outlet center gross leasable area (GLA) has

grown at a 5.3% CAGR over the past 6 years, and

now stands at 86 million square feet. During the

same period, sales per square foot have notched a

4.8% CAGR, growing from $301/sq. ft. in 2008 to

$398/sq. ft. in March of this year. Average rents have

kept pace, growing from $28/sq. ft to $34/sq. ft., a

CAGR of 3.1%.

The unique outlet model makes it somewhat a-

cyclical. When full-price retailers are doing well, they

do not feel the need to cut prices, and hence outlets’

deep discounts are all the more attractive. From the

2Q14 conference call with PVH Corp. CEO Manny

Chirico: “[T]he healthiest environment for the outlet

channel is when regular retail is doing well, because

there’s not a compelling message going on at regular

retail from a promotional point of view.” Outlets’

value proposition for both the consumer and retailer

is at its most robust in good times. However even in

$301

$331

$357

$398

$28

$25

$30

$34

-

10

20

30

40

50

60

70

80

90

$0

$100

$200

$300

$400

$500

2008

2010

2012

2014

SquareFeet(MM)

$/SquareFoot

Growth of the US Outlet Industry

Total US Outlet Center GLA

Sales per Square Foot

Average Rent per Square Foot

5.

Tanger Factory Outlets (NYSE: SKT) Mohit Hajarnis & Carter Chen

9

mean times, outlet centers’ value proposition is still

intact. There is only so much full-price stores are

willing to discount, and hence outlet traffic is steadier

in bad economic times than traffic at full-price

stores.

Industry Risks

Despite robust growth, the outlet industry has its

share of naysayers. Bears’ wariness can be boiled

down to two concerns. 1) Effective price

discrimination is unachievable, and outlet stores

cannibalize sales from full price channels. 2) Outlets

0

dilute brand value. These concerns give rise to

questions about whether outlet malls are a truly

effective and sustainable retail channel, or whether

they inflate sales at the expense of margins and

brand identity.

To address these concerns, We think it is important

to draw a distinction between brands that are

considered luxury (or “accessible luxury”) and brands

that are not. Part of the appeal of a luxury brand, like

Coach, Michael Kors, or Burberry, is its exclusivity.

For the consumers of these brands, there is an

appeal from the sense of luxury that comes from a

high price tag. So discounts on these luxury brands

have the potential to dilute brand value, as they make

these items less exclusive. We believe that this

phenomenon exists. The decline of the Coach brand

over the past few years is evidence of this trend.

However, we believe that brands that are not

traditionally considered luxury—Gap, Banana

Republic, Van Heusen, and other core constituents

of outlet malls—are not subject to this brand dilution.

For the consumer of these items, exclusivity is not a

concern—and so dilution should not be feared for

these brands. And in fact, these luxury brands make

up only a small portion of outlet storefronts—14% by

our calculations.

We also see no evidence of ineffective price

discrimination. Like we mentioned above, outlets are

a complement to full-price retailers, especially when

full price retailers are doing well. Glenn Murphy, CEO

of Gap, Inc. notes during their 2Q14 conference call

“this incredible relationship between the specialty

business and our outlet business.” He goes on to

comment that “The only place that we’re seeing real

estate growing and square footage increasing as in

lifestyle centers after being converted to the power

centers, or being converted to outlet centers.”

Largest Outlet Chains by Store Count in 2014

Dressbarn/Dressbarn Woman 205

Carter’s Outlets 160

Gymboree 156

Tommy Hilfiger 155

Van Heusen 154

Gap Outlet 152

Wilsons Leather Outlet 150

OshKosh B’Gosh Outlet 142

Polo Ralph Lauren Factory Stores 139

Banana Republic Factory Stores 128

Levi’s Outlet 128

Aeropostale Outlet 126

Brooks Brothers Factory Store 125

Children’s Place Outlet 124

Lane Bryant Outlet 118

Izod 117

PacSun 112

Guess? Factory Store 110

Jockey Outlet 110

Calvin Klein 107

Names in Red represent Luxury Brands

% of Total Stores that are Luxury: 14%

Source: Value Retail News

Outlet Stores from a Retailer’s Perspective

Luxury Everyday Upscale Everyday

Regular Consumers Cannibalize Sales Cannibalize Sales Grow Sales

Discount Consumers Grow # of Customers Grow # Customers Grow Sales

6.

Tanger Factory Outlets (NYSE: SKT) Mohit Hajarnis & Carter Chen

1

Key Value Generators

Market Rent and a Growing Portfolio

Tanger’s profitability in the next five years, and

beyond, will be primarily driven by the renewal of

long-lived leases in its portfolio and strong pipeline

of new properties and expansions. The industry

average for outlet center base rent is $33.72 psf

(Value Retail News), but Tanger charges $20.40 psf.

We assert that there are no material differences

between Tanger’s properties and competitors’

properties, but in fact Tanger properties may be

more valuable because the Tanger brand name

drives customer traffic. In Y/E 2013, Tanger received

a 19.3% premium on its renewed leases and a

37.8% premium on re-leased properties. The

discrepancy between Tanger’s base rent and the

market rent suggests that Tanger can capture a

significant premium on renewals – and an even

higher premium on properties that are re-leased

(current tenant leaves and a new tenant leases the

property).

A forward prediction of the revenue increases from

renewed and re-leased properties in Y/E

demonstrates 11.9% projected revenue growth. We

divided total properties up for renewal/re-tenanting

into 25% re-tenanted and 75% renewed, reflective of

the traditional mix. We anticipate that this ratio may

lean more towards re-tenanted properties this year

because of the Coldwater Creek bankruptcy, which

should open additional space. We estimated that all

renewed leases would be charged a 20% premium,

and all re-tenanted / new properties would earn the

market rate for base rent - $33.72. All other revenues

were estimated using Revene/psf ratios and keeping

them fixed over the long term (Additional information

on valuation is available on page 8).

Most beneficial to Tanger’s long-term revenue

growth is its robust pipeline of new and renovated

outlet properties. Over the next three year, Tanger

plans to open 2.5 million square feet (weighted for

ownership). Assuming Tanger receives the market

rent for these properties, average rents for Tanger’s

portfolio should increase, and given the 8-year

average term of its expiring leases this year, these

rates should remain lock in for a considerable period

of time – protecting the company from

macroeconomic retail trends. We used the

company’s estimates for renewals, the historical ratio

of renewal / re-tenanting, and company’s stated

2

portfolio expansions from press releases and

earnings calls. Tanger is growing their portfolio faster

than their historical pace because they were able to

raise debt at low rates between 2010 and 2014, and

spend it on capital expenditures over the next five

years.

Balance Sheet Health

Tanger’s portfolio growth is especially remarkable

because the company has not overextended its

balance sheet to fund growth. Tanger’s DSCR is

2.46X, compared to Simon’s 2.12X and GGP’s 1.13X

DSCRs. The DSCR ratio reflects the company’s

ability to take on additional debt; Tanger can take on

a maximum of $1.9B of new debt, doubling total

debt and (assuming new debt is spent on new

properties at $292 psf), growing the total portfolio by

6.3 million square feet – growing its portfolio by

50%. The same is not true for Tanger’s competitors

because their DSCRs are pushing the limits set in

their debt covenants. Tanger’s ability to take on

Renewal 2014 (E)

Square Feet 838,181

Average Expiring

Rent

$19.38

Average New Rent $23

Premium 20%

Release 2014 (E)

Square Feet 902,819

Average Expiring

Rent

-

Average New Rent $34

Premium -

Total Square Feet* 13,010,000

*Including new properties

Revenue Breakdown

($KK)

2014 (E)

Base Rentals $280,290.12

Percentage Rentals $11,804.31

Expense

reimbursement

$115,046.67

Other Income $11,228.31

Total Income $418,369.43

Base Rentals / Sq Ft $21.50

Percentage Rentals /

Sq Ft

$0.91

Expense

reimbursement / Sq

Ft

$8.83

Other Income / Sq Ft $0.86

7.

Tanger Factory Outlets (NYSE: SKT) Mohit Hajarnis & Carter Chen

3

additional debt and grow the portfolio is an important

component of its value generating process. We can

objectively see the health of Tanger’s balance sheet

from its recent balance sheet activity. Tanger

refinanced its $250M Sr. Loan (I) down from 6.15%

to 3.75% due 2024. These 10-year loans incur a ~

150 bps premium to 10-year US treasuries,

suggesting a low estimated probability of default. A

similar Sr. Loan issued by CBL & Associates for

$300MM in October 2014 was priced at 4.60% - 85

bps above Tanger’s debt.

Risks & Other Considerations

Tanger’s biggest concerns are competition with

malls, other REITs, and online shopping.

At a fundamental level, malls and outlet centers

rarely compete for customers because consumers

go to Outlet malls seeking the deep discounts that

retailers do not provide at malls. However, Tanger

strategically builds properties far from urban centers,

so most customers make a day-trip out to outlet

centers, instead of competing for business with local

malls, and spending more than they do at traditional

malls.

Tanger (SKT) Simon (SPG) GGP

Macerich

(MAC)

CBL Average

$ Rent / Sq Ft $20.40 $42.34 $71.29 $44.51 $42.48 $44.20

Tenant $ Sales / Sq

Ft

$387.00 $582.00 $564.00 $527.25 $356 $483.25

Occupancy Cost % 5.27% 7.27% 12.64% 8.44% 11.93% 9.11%

4

The demand for outlet malls has increased amongst

other investors. However, Tanger believes that it

maintains an economic moat because of its long-

standing partner relationships, which are necessary

for high occupancy properties. However, outlet

developers like Simon and General Growth

Properties, compete with Tanger for prime properties

to build outlet malls, which Tanger cannot protect

against. Moreover, with Simon and GGP’s larger,

albeit less healthy, balance sheets, they can acquire

properties or out-bid Tanger on key properties.

Moreover, the rapid growth of outlet malls in the US

may reduce profitability per property and decrease

the company’s ROREA.

Tanger has faced constant competition from online

shopping, but historical financial results have proven

the company’s resilience to new entrants. However,

the advent of new discount luxury online retailers like

Gilt.com proves problematic for Tanger’s business

model of offering luxury goods at discount prices.

Gilt.com generated $550 M in sales in 2012,

compared to $450 M in 2011

(http://www.bloomberg.com/news/2013-07-31/gilt-

groupe-ceo-seeks-to-prove-flash-sales-are-no-

fad.html), demonstrating a clear demand for the

$5.36

$2.51

$2.85

$4.20

$4.88

$5.03

$8.51

$8.92

$8.43

$9.09

$8.06

$0

$5

$10

$15

$20

$25

$30

$35

$40

Y/E 2008

Y/E 2009

Y/E 2010

Y/E 2011

Y/E 2012

Y/E 2013

2014 (E)

2015 (E)

2016 ( E)

2017 (E)

2018 (E)

Lease Expirations and Projected Premiums

Avg. Premium on New Rents

Industry Average Rent

8.

Tanger Factory Outlets (NYSE: SKT) Mohit Hajarnis & Carter Chen

5

product. However, Gilt.com services a different need

than Tanger outlets. Foremost, Gilt.com is geared

toward younger consumers with high incomes, while

Tanger Outlets are marketed to older, middle-

income Americans. Additionally, Gilt.com seeks to

off-load retailers excess inventory, not provide the

same exposure to new consumers or grow existing

consumers. Finally, retailers view Gilt.com as a

means of reducing inventory risk; by selling the

discounted inventory at, or below, cost, it reduces

the risk that it will be unable to sell the merchandise

eventually. Outlet malls serve an entirely different

need than Gilt.com.

Valuation

To understand the value in Tanger, we modeled

Tanger in two ways: a DCF valuation and a

Discounted Dividend Model. We chose to expand

our valuation by including a DDM because the

tangible cash flows that Tanger’s investors receive

are dividends, while free cash flows are the

hypothetical funds available to investors each year.

Today’s low interest rate environment is providing

opportunities for Tanger to expand its portfolio,

which requires high capital expenditures today.

Those capital expenditures, a cash expense, are

diluting Free Cash Flow, but are not affecting

Adjusted Funds from Operations, the metric which

the company uses to decide dividend payouts.

Historically, the company has paid out roughly 50%

6

to 60% of AFFO, and our model assumed a fixed

payout over the long-term.

Our valuation depended on our projecting the

average rent a new tenant would be charged, as well

as the total square footage in Tanger’s portfolio. We

estimated that the average new rent for 2014 would

be the market rate of $33.72 (via research report)

and would grow at 3% a year. Total square footage

for Tanger’s portfolio was estimated in future years

by taking into account all developing projects Tanger

disclosed, and then adding 700,000 square feet in

2017 and 2018 – in line with historical portfolio

growth. We also took into account the total square

footage renewed each year based on company

estimates in the 10-K. The total square footage was

divided into renewals – which garnered a 20%

premium on expiring rent, and re-tenanting, which

were charged the market rent. All new properties

were charged the average market rent as well. Other

line items were estimated in the following manners:

Percentage rentals: percentage rentals per square

foot (2013) multiplied by square feet for each year.

Expense reimbursements: expense

reimbursements per square foot (2013) multiplied by

square feet for each year.

Other Income: other income per square foot (2013)

multiplied by square feet for each year.

SG&A: SG&A margin was kept constant.

Projections

$KK 2014 (E) 2015 (E) 2016 ( E) 2017 (E) 2018 (E)

Total Revenues $418,369 $475,145 $514,206 $553,698 $598,343

Operating Expenses $137,563 $156,231 $169,074 $182,059 $196,739

D&A $100,455 $108,716 $113,918 $119,313 $124,707

SG&A $44,019 $49,993 $54,102 $58,258 $62,955

Operating Income $136,333 $160,206 $177,112 $194,069 $213,942

Interest Expense $59,373 $59,373 $64,921 $70,675 $70,675

Other Income / GoS $0 $52,004 $0 $0 $52,004

Income before taxes $76,960 $152,837 $112,190 $123,394 $195,271

Equity in earnings of

unconsolidated ventures*

$0 $0 $0 $0 $0

Noncontrolling Income from

Operating Partnership

$0 $0 $0 $0 $0

Net Income $76,960 $152,837 $112,190 $123,394 $195,271

Capital Expenditures $108,133 $116,800 $167,900 $153,300 $153,300

AFFO (Calculated) $18,010.94 $10,001.00 $123,129.59 $160,081.19 $110,592.72

FCF (Calculated) 2014 (E) 2015 (E) 2016 ( E) 2017 (E) 2018 (E)

*Represents earnings in joint ventures - accounted in Total Revenues in this model

9.

Tanger Factory Outlets (NYSE: SKT) Mohit Hajarnis & Carter Chen

7

D&A: D&A per square foot (2013) multiplied by total

square footage for the year.

Interest Expense: Interest expense divided by total

debt (2013), 4.54%, multiplied by total debt for each

year.

Total Debt: Stated asset value dividend by square

feet (2013) multiplied by new square feet not already

financed (2017 – 2018). Debt is raised in the same

year capital expenditures are incurred. Although

CapEx is $292 per square foot, New Debt is roughly

$1,000 per square foot given the cost of land and

carrying value of the finished asset.

Capital Expenditures: Building expenses per square

foot (2013), $292, multiplied by half of total square

footage added in the given year, and in the following

8

year.

Cost of Debt: dividing interest expense by total debt

for the year, 4.54% - kept constant given high

percentage of fixed debt.

Cost of Equity: CAPM. See model for breakdown.

The terminal value is estimated in two ways: using a

terminal growth rate, of 2%, and a growth multiple,

which is the current P/E of 31.57X.

Our DCF output was $21.73 (terminal growth rate)

and $39.28 (terminal multiple). The $39.28 value is

close to the current market price, lending credence

to our assertion that the market believes Tanger is

fairly valued because its DCF models indicate a fair

value near $35 - $37. However, our DDM output was

$50.31 (terminal growth rate) and $52.60 (terminal

Growth Rate Method

Enterprise Value $4,801,340

Debt -

Market Value $4,801,340

Implied Price $50.31

Upside 40.8%

Terminal Dividend Yield Method

Enterprise Value $4,985,953

Debt -

Market Value $4,985,953

Implied Price $52.24

Upside 46.3%

Sensitivity Analysis

Market Return

$50.31 6.0% 6.5% 7.0% 7.5% 8.0%

TerminalGrowth

Rate

1.0% $43.32 $40.59 $38.18 $36.03 $34.11

1.5% $50.15 $46.49 $43.32 $40.55 $38.11

2.0% $59.89 $54.69 $50.31 $46.57 $43.34

2.5% $74.90 $66.85 $60.35 $54.99 $50.49

3.0% $101.04 $86.76 $76.00 $67.60 $60.85

9

dividend yield), which we think is an accurate

representation of Tanger’s intrinsic value. While front-

loading cash expenses when it is easy and cheap to

raise debt is a strong strategy for long-term

investors, it depresses calculated Free Cash Flow,

and thereby underprices the intrinsic value of the

business. The tangible cash flows investors receive

are dividends, and we estimate a 40% - 45% upside.

This valuation is attractive to the 3 – 5 year investor

because it provides the market with sufficient time to

0

move the price closer to intrinsic value, but

nonetheless provide a healthy 2.7% dividend yield

over the next 3 – 5 years, guaranteeing 8.1% to

13.5% return in realized dividends, plus reinvestment

gains. The margin of safety generated by the

dividends is attractive to the conservative investor.

Market Return

$52.24 6.0% 6.5% 7.0% 7.5% 8.0%

SKTYield

2.1% $65.68 $65.01 $64.35 $63.70 $63.06

2.3% $59.01 $58.41 $57.82 $57.24 $56.67

2.6% $53.67 $53.13 $52.60 $52.07 $51.55

2.9% $49.31 $48.82 $48.33 $47.85 $47.37

3.1% $45.67 $45.22 $44.77 $44.32 $43.88

10.

Tanger Factory Outlets (NYSE: SKT) Mohit Hajarnis & Carter Chen

Revenue Breakdown ($KK) Y/E 2011 Y/E 2012 Y/E 2013 1Q 2013 2Q 2013

Base Rentals $207,637 $235,233 $253,402 $66,976 $68,160

Percentage Rentals $9,084 $11,172 $11,251 $2,083 $1,915

Expense reimbursement $89,620 $101,110 $109,654 $31,542 $29,452

Other Income $8,882 $9,482 $10,702 $2,241 $2,749

Total Income $315,223 $356,997 $385,009 $102,842 $102,276

Base Rentals / Sq Ft $18.72 $20.10 $20.40 $5.39 $5.49

Percentage Rentals / Sq Ft $0.82 $0.95 $0.91 $0.17 $0.15

Expense reimbursement / Sq Ft $8.08 $8.64 $8.83 $2.54 $2.37

Other Income / Sq Ft $0.80 $0.81 $0.86 $0.18 $0.22

Real Estate Assets / Debt Y/E 2011 Y/E 2012 Y/E 2013 Maturity Rate

Assets

Land $141,577 $148,002 $230,415

Buildings, Improvements &

Fixtures

$1,434,637 $1,799,350 $2,019,404

Total $1,576,214 $1,947,352 $2,249,819

Accumulated Depreciation $453,145 $582,859 $654,631

Liabilities

Senior notes

Senior notes (1)* $249,490 $249,683 $249,789 Nov '15 6.15%

Senior notes (2) $298,019 $298,350 $298,531 Jun '20 6.13%

Senior notes (3) $245,928 Dec '23 3.88%

Senior exchangeable notes $7,107 Aug '11 3.75%

Mortgages

Atlantic City $56,707 $32,626

November '21

- December

'26

5.14% - 7.65%

Deer Park $148,522 Aug '18 2.80%

Hershey $32,213 $30,963 Aug '15 5.17% - 8.00%

Ocean City $18,825 $18,386 Jan '16 5.24%

Note Payable $9,453 $9,604 Jun '16 1.50%

Unsecured term loan

$250,000 $250,000 Feb '19

LIBOR +

1.60%

Unsecured term note

$7,500 Aug '17

LIBOR +

1.30%

Unsecured lines of credit

$160,000 $178,306 $16,200 Oct '17

LIBOR +

1.00%

Total Debt $714,616 $1,093,537 $1,308,049

Debt Due

Average Cost of Debt 3.95%

Net Working Capital $861,598 $853,815 $941,770

Disclosure: We certify that all work presented is our own, and any external sources are properly

cited. We have disclosed all pertinent information discovered while researching this pitch and also

declare that we find this stock to be an ethical purchase.