Recommended

More Related Content

Similar to Debit note & credit note.pptx

Similar to Debit note & credit note.pptx (20)

Recently uploaded

Recently uploaded (20)

Debit note & credit note.pptx

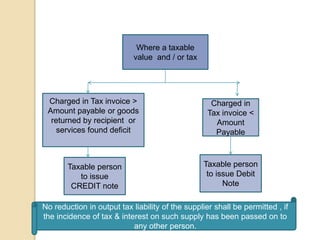

- 1. Where a taxable value and / or tax Charged in Tax invoice > Amount payable or goods returned by recipient or services found deficit Taxable person to issue CREDIT note Charged in Tax invoice < Amount Payable Taxable person to issue Debit Note No reduction in output tax liability of the supplier shall be permitted , if the incidence of tax & interest on such supply has been passed on to any other person.

- 2. Debit note – As per Section – 34 of CGST Act When a tax invoice has been issued for supply of any goods or services or both and the taxable value or tax charged in that tax invoice is found to be less than the taxable value or tax payable in respect of such supply, the registered person, who has supplied such goods or services or both, shall issue to the recipient a debit note containing the prescribed particulars.

- 3. Credit note – As per Section 34 (3)of CGST Act , 2017 Where a tax invoice has been issued for supply of any goods or services or both and the taxable value or tax charged in that tax invoice is found to exceed the taxable value or tax payable in respect of such supply, or where the goods supplied are returned by the recipient, or where goods or services or both supplied are found to be deficient, the registered person, who has supplied such goods or services or both, may issue to the recipient what is called as a credit note containing the prescribed particulars.

- 4. Declaration in return details of credit Note & Debit Note Credit Note - Any registered person who issues a credit note in relation to a supply of goods or services or both shall declare the details of such credit note in the return for the month during which such credit note has been issued but not later than September following the end of the financial year in which such supply was made , or the date of funishing of the relevant annual return , whichever is earlier . It may be noted that annual return is required to be filed under section 30(2) on or before 31st December of the financial year following the relevant financial year. In cases where such annual return is filed after 30th September, the time limit for issuing credit/debit note will be 30thSeptember only. Debit Note - Any registered person who issues a debit note in relation to a supply of goods or services or both shall declare the details of such debit note in the return for the month during which such debit note has been issued .

- 5. Important points The supplier shall mention the details of debit or credit note in from GSTR-1.On filing the details it will get auto-populated in form GSTR-2A for the recipient. The recipient can either modify or accept or reject these details and file form GSTR-2. Debit Note/Credit Note Must Contain Invoice Number 1. The debit note/credit note must contain the invoice number of the original supplies made. 2. The details of the debit note/credit to be declared in form GSTR-1 shall be given along with details of original invoice number, date and GSTIN. The time limit is only for issuing credit note and not debit note. The records of the debit note or credit note have to be retained until the expiry of seventy two months from the due date of furnishing of annual return for the year pertaining to such accounts and records.