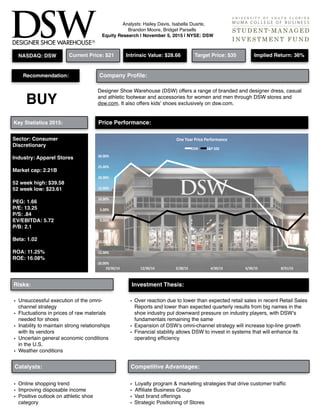

1. Key Statistics 2015:

BUY

Recommendation: Company Profile:

Designer Shoe Warehouse (DSW) offers a range of branded and designer dress, casual

and athletic footwear and accessories for women and men through DSW stores and

dsw.com. It also offers kids' shoes exclusively on dsw.com.

Sector: Consumer

Discretionary

Industry: Apparel Stores

Market cap: 2.21B

52 week high: $39.58

52 week low: $23.61

PEG: 1.66

P/E: 13.25

P/S: .84

EV/EBITDA: 5.72

P/B: 2.1

Beta: 1.02

ROA: 11.25%

ROE: 16.08%

Price Performance:

!20.00%&

!15.00%&

!10.00%&

!5.00%&

0.00%&

5.00%&

10.00%&

15.00%&

20.00%&

25.00%&

30.00%&

10/30/14& 12/30/14& 2/28/15& 4/30/15& 6/30/15& 8/31/15&

One&Year&Price&Performance&

DSW& S&P&500&

Investment Thesis:Risks:

• Unsuccessful execution of the omni-

channel strategy

• Fluctuations in prices of raw materials

needed for shoes

• Inability to maintain strong relationships

with its vendors

• Uncertain general economic conditions

in the U.S.

• Weather conditions

• Over reaction due to lower than expected retail sales in recent Retail Sales

Reports and lower than expected quarterly results from big names in the

shoe industry put downward pressure on industry players, with DSW’s

fundamentals remaining the same

• Expansion of DSW’s omni-channel strategy will increase top-line growth

• Financial stability allows DSW to invest in systems that will enhance its

operating efficiency

Analysts: Hailey Davis, Isabella Duarte,

Brandon Moore, Bridget Parsells

Equity Research | November 5, 2015 | NYSE: DSW

Current Price: $21 Intrinsic Value: $28.66 Target Price: $35 Implied Return: 36%NASDAQ: DSW

• Loyalty program & marketing strategies that drive customer traffic

• Affiliate Business Group

• Vast brand offerings

• Strategic Positioning of Stores

Catalysts: Competitive Advantages:

• Online shopping trend

• Improving disposable income

• Positive outlook on athletic shoe

category

2. Investment Thesis Breakdown

Shoe Industry: Omni-channel Expansion:

Financial Stability:

Disappointing retail sales in June and September that

was due to slowing job growth and overseas

turbulence that curbed discretionary spending created

downward pressure on the overall retail industry.

DSW's stock dropped among its peers because of the

conditions.

Weather conditions also adversely affected sales of

DSW and some of its industry peers in the third

quarter of 2015. Within its industry, its fundamentals

remain attractive, as the stock dropped further than its

competitors even though the revenues were missed on

for similar reasons.

DSW is expanding its omni-channel strategy, which will result

in previously store-only products to be also available online

and in the recently launched DSW mobile app. This will

respond to the trending customer preference of shopping

online by expanding the channels from which customers can

purchase from DSW. The options to Buy Online, Pick-up In-

Store and Buy Online, Ship To Store will be implemented in the

fourth quarter of 2015, which will expedite in-store pickup for

online sales. Furthermore, DSW's has turned all of its 449

stores into mini-distribution centers capable of fulfilling demand

that is originated elsewhere, which allows customers to

purchase shoes from a shop other than from where the

customer originally demanded the item.

DSW's omni-

channel has

been proven

successful

with it

trending to

well over

$100 million in

sales this year. Its omni-channel customers spend two to three

times more than its single channel customers, with its mobile

app playing an important role in converting single channel

customers. Mobile traffic has grown rapidly over the last two

years and now accounts for over 40% of online traffic.

With healthy cash flows, DSW has had and will continue to have the capability of investing in systems that will enhance its

operating efficiency in areas such as its supply chain, merchandise planning and allocation, inventory management,

distribution and labor management.

DSW has implemented an order routing fulfillment optimization for all its product categories. This proprietary technology is

designed to reduce markdowns by fulfilling orders from the slowest turning locations. It has also completed investments in its

supply chain to support size replenishment and size optimization. Size replenishment focuses on replenishing core styles at a

size level; size optimization allows it to effectively allocate sizes by store. All categories will be planned using an enterprise-

wide assortment planning system that will allow it to build assortments based on local customer profiles rather than just based

on store volume.

During fiscal 2014, DSW had invested in the installation of a new shipping sorter in its distribution center. This new shipping

sorter improved productivity and increased shipping capacity within its fulfillment center. Its fulfillment center processes

orders, which are shipped directly to customers using a logistics provider. Its ship from store program enables it to fulfill unmet

demand originating from either dsw.com or DSW stores from inventory that is located in other stores rather than only from its

inventory in the fulfillment center or the customer’s home store.

Equity Research | November 5, 2015 | NYSE: DSW Analysts: Hailey Davis, Isabella Duarte, Brandon Moore, Bridget Parsells 2

Recommendation: BUY

$0.00$

$5.00$

$10.00$

$15.00$

$20.00$

$25.00$

$30.00$

$35.00$

$40.00$

$45.00$

$50.00$

$250,000$

$270,000$

$290,000$

$310,000$

$330,000$

$350,000$

$370,000$

$390,000$

$410,000$

Jul02005$

Jan02006$

Jul02006$

Jan02007$

Jul02007$

Jan02008$

Jul02008$

Jan02009$

Jul02009$

Jan02010$

Jul02010$

Jan02011$

Jul02011$

Jan02012$

Jul02012$

Jan02013$

Jul02013$

Jan02014$

Jul02014$

Jan02015$

Jul02015$

Total$Monthly$Retail$Sales$vs.$DSW$Stock$Price$$

Total&Monthly&Retail&Sales& DSW&Stock&Price&

3. `

DSW Rewards is a customer loyalty program that the company relies on to drive customer traffic, sales and loyalty. DSW

Rewards members earn reward certificates that offer discounts on future purchases. In both fiscal 2014 and 2013, shoppers in

the loyalty program generated approximately 90% of DSW sales. As of January 31, 2015, approximately 23 million members

were enrolled in DSW Rewards and have made at least one purchase over the course of the last two fiscal years, compared

to approximately 22 million members as of

February 1, 2014.The loyalty program gives

consumers an incentive to come back to DSW

rather than competitors due to the fact they will be

earning loyalty points and receiving discounts.

DSW is able to use data from the loyalty program to

inform shopping behaviors and trends, and that

allows the company to tailor its experience to how

customers are already behaving.

DSW’s new digital marketing strategies drove sales

for the second quarter of 2015. It uses advanced

analytics to deliver targeted messages throughout

the customer journey. It does so through on-site

search technology, email strategy, and digital media

targeting which results in increased customer

engagement and incremental sales.

Loyalty Program & Marketing Strategies:

13#

15#

17#

19#

21#

23#

25#

2010# 2011# 2012# 2013# 2014# 2015#

Loyalty#program#customers#

Loyalty#program#

customers#

Unsuccessful execution of the omni-channel strategy:

Changes in weather patterns affect consumer

preferences, therefore if the store orders seasonal

products in bulk that do not meet weather

conditions, it could face inventory write downs that

would adversely affect revenue and margins.

DSW relies on its strong relationships with vendors to purchase

brand name and designer merchandise at favorable prices. If these

relationships are damaged, DSW may not be able to obtain a

significant merchandise at attractive prices, which would adversely

affect the business and financial performance. However, since its

beginnings DSW has been able to successfully maintain and create

new strong relationships with its vendors, therefore we do not see

this risk materializing.

Decreases in disposable income and in the consumer

confidence index, weak demand for apparel in the retail

sales report and increasing unemployment rate can

adversely affect sales and the financial performance of the

Risks

Recommendation: BUY

Equity Research | November 5, 2015 | NYSE: DSW Analysts: Hailey Davis, Isabella Duarte, Brandon Moore, Bridget Parsells 3

Competitive Advantages

Uncertain general economic conditions in the U.S.:

Weather conditions affecting seasonal sales:

DSW’s management is positioning the company as an

omni-channel retailer and is expected to make significant

capital investments and have significant expenses related

to this strategy. The failure or inability to execute the omni-

channel strategy would materially adverse the business,

financial and operating results, and how customer

expectations are met.

Inability to maintain strong relationships with its vendors:

4. Competitive Advantages Continued

Vast Brand Offerings:

DSW stores and dsw.com sell a large assortment of better-

branded and private label merchandise. Its products at each

store are geared toward the particular demographics of the

location. A typical DSW store carries approximately 24,000

pairs of shoes in approximately 2,000 styles compared to a

significantly smaller product offering at typical department

stores. A wide product portfolio enables DSW to cater to

various customer needs and broaden its market coverage,

which, in turn, increases the company's top-line growth.

91%$

57%$

8%$

13%$

38%$

6.30%$

79%$

Shoe%sales%as%%%of%revenue%%

DSW$

TJX$$

JCP$

ROST$

M$

AMZN$

FL$

DSW opens stores in high traffic areas, such as strip

centers and malls that attract more consumers into

the stores. It also plans to reposition existing stores

as opportunities arise.

As shown on the graph to the right, DSW opens

stores in the six states with the most popular cities

such as New York, Houston, Austin, Tampa, Miami,

and San Francisco to name a few.

DSW has revenue sharing licensing agreements

through its Affiliate Business Group (ABG) with

Steinmart, Gordmans, Yellow Box and Frugal Fannie.

DSW is able to leverage the store space of 370

additional locations and E-commerce channels

through ABG contributing 5.8% of revenue over the

past three years while not having to add the fixed

costs associated with these locations.

Affiliate Business Group:

41#

37#

33#

27#

22# 21#

States&with&20+&Store&Count&

California#

Texas#

New#York#

Florida#

Illinois#

Pennsylvania#

Recommendation: BUY

Strategic Positioning of Stores:

Equity Research | November 5, 2015 | NYSE: DSW Analysts: Hailey Davis, Isabella Duarte, Brandon Moore, Bridget Parsells 4

5. Recommendation: BUY

Suppliers & Demographics

DSW purchases merchandise in bulk directly from approximately 430 domestic and foreign vendors that provide a

discount for DSW that are passed onto the customers. Its vendors include suppliers who either manufacture its own

merchandise, supply merchandise

manufactured by others, or both. Most of its

domestic vendors import a large portion of their

merchandise from abroad.

If prices of raw materials increase, specifically

leather and rubber, its suppliers will pass the

increase onto DSW, which will in turn pass it

onto its customers and could lose revenues due

to price increases. However, according to the

graph shown on the right rubber is increasing

and leather is decreasing, therefore keeping

cost constant. This is expected to remain

constant in the successive years.

DSW’s customers include middle class

consumers with 28% of customers having

income ranging from $30,000-$60,000 and 31%

having income above $60,000. With the

economy continuing to show improvement, its growth will increase with consumers willing to spend more money on shoes.

Because DSW targets customers are middle class consumers, it will perform better with an improving economy.

0"

50"

100"

150"

200"

250"

300"

Oct*10"

Jan*11"

Apr*11"

Jul*11"

Oct*11"

Jan*12"

Apr*12"

Jul*12"

Oct*12"

Jan*13"

Apr*13"

Jul*13"

Oct*13"

Jan*14"

Apr*14"

Jul*14"

Oct*14"

Jan*15"

Apr*15"

Jul*15"

Commodity"price"for"rubber"&"leather"

Rubber"

Leather"

Equity Research | November 5, 2015 | NYSE: DSW Analysts: Hailey Davis, Isabella Duarte, Brandon Moore, Bridget Parsells 5

Industry Drivers

Relying on consumer spending, the shoe industry will

benefit from increased consumer spending over the

next five years with consumers using multi-channel

avenues such as online retail and mobile

applications. A greater number of Americans

returning to work, combined with improved home

ownership conditions, will increase consumer

confidence leading to increased discretionary

spending. Shoe store sales are expected to grow by

approximately 2.7% CAGR in the next five years as

per capita disposable income growth is projected to

peak in 2015 and then slow at a modest pace in

successive years.

One of the fastest growing trends in the apparel

sector is athleisure, where additional growth in sales is

expected. There is a growing proportion of the population participating in sports, thus athletic shoe wear is likely to be

purchased for style and function to wear whether the consumer is exercising or relaxing.

This shoe store industry is in the mature stage of the business cycle described as having tight profit margins, growth in sales

slower than GDP growth, and high competition placing downward pressure on prices. Increases in revenue will come from

increasing store counts in underserved markets and opening up more shopping channels that are convenient for the customer,

such as online stores.

!3.00%&

!2.00%&

!1.00%&

0.00%&

1.00%&

2.00%&

3.00%&

2010& 2011& 2012& 2013& 2014& 2015& 2016& 2017& 2018& 2019& 2020&

Per&capita&disposable&income&

Per&capita&disposable&income&

6.

Recommendation: BUY

Equity Research | November 5, 2015 | NYSE: DSW Analysts: Hailey Davis, Isabella Duarte, Brandon Moore, Bridget Parsells 6

Competitors

Finish Line (FINL): Shoe Carnival (SCVL):

The Finish Line, Inc. is a mall-based specialty

retailer of branded athletic footwear, apparel and

accessories. Finish Line operates in the US and

the District of Columbia.

Demographics: Middle to high level income

athletic people who practice sports. High quality,

known brand items.

Shoe Carnival is a family footwear retailer. The company's stores

offer dress, casual shoes, sandals, boots and athletic footwear for

men, women and children with a selection of both name brand and

private label merchandise. Shoe Carnival primarily operates in the

US, where it is headquartered in Evansville, Indiana.

Demographics: Moderate income, value conscious families.

Genesco Partners (GCO):

Foot Locker Inc. (FL):

Based in Nashville, Tennessee, is a specialty

retailer of branded footwear, licensed and

branded headwear, as well as a wholesaler of

branded footwear. Genesco also designs,

sources, markets and distributes footwear.

Genesco is represented by more than 2,225 retail

stores in the United States, Canada, and Puerto

Rico and is composed of five main business

segments; Journeys Group, Hat World/Lids

Group, Underground Stations Group, Johnston &

Murphy, and the licensed brands, consisting

mainly of the Dockers Brand.

Demographics: Relatively young consumers

(20-35 years of age).

Foot Locker, Inc. is a retailer of athletic footwear and apparel.

The company operates 3,473 athletic stores under various brand

names, including Foot Locker, Lady Foot Locker, Kids Foot

Locker, Champs Sports, Footaction and SIX:02. Foot Locker has

presence in 23 countries. It is headquartered in New York City,

New York.

Demographics: FootAction stores target urban customers who are

more brand and trend-conscious while Champs Sports target

sports enthusiasts with a broad array of footwear and sporting

goods equipment.

J.C. Penney Inc. (JCP):

Ross Stores Inc. (ROST):

J.C. Penney Company, Inc. is one of the leading

retailers in the US. The company offers a range of

family apparel and footwear, accessories, jewelry,

beauty products, and home furnishings through a

chain of department stores and the e-commerce

website jcp.com. JC Penney is the holding

company whose principal operating subsidiary is

J. C. Penney Corporation. J.C. Penney primarily

operates in the US.

Ross Stores is an off-price retailer of apparel and home

accessories. It sells products from other seasons at a marked

down price. Ross Stores is an off-price retailer that purchases

unwanted inventory from name-brand manufacturers,

department stores, and other retailers at an opportunistically

low price. ROST then sells them at heavy discounts off the

regular retail price. Carries more popular brands.

Demographics: Price-conscious middle class consumers and

consumers from the lower-income brackets.

7.

Recommendation: BUY

Competitors Continued

Competitor Analysis:

Throughout 2015, DSW’s and its competitors,

such as Shoe Carnival, Finish Line, and

Genesco prices decline because of missed

expectations in revenue. For instance,

unfavorable weather was a common factor for

less-than-expected sales of winter shoes.

• Shoe Carnival missed on revenues in both

first and second quarters and had its

guidance revised downwards.

• Finish Line, on the other hand, beat

revenues and earnings in the first quarter

but missed on revenues in the second

quarter due to a deceleration in same-store sales.

• Genesco missed on its revenues and earnings in the first quarter of the year and revised its full-year guidance downwards

7.30%&

4.70%&

2.66%&

2.40%&

14.50%&

5.80%&

5.50%&

Market&Share&&

DSW&

Finish&Line&

Shoe&Carnival&

Genesco&

Foot&Locker&

Payless&&

Brown&Shoe&Company&

0"

5"

10"

15"

20"

25"

30"

2011" 2012" 2013" 2014" 2015" Forward""

Historical*P/E*Ra/os*0*Compe/tors*

DSW"

Finish"Line"

Shoe"Carnival"

Foot"Locker"

Genesco"

2"

2.5"

3"

3.5"

4"

4.5"

5"

2011" 2012" 2013" 2014" 2015"

Inventory)Turnover)

DSW)

Finish)Line)

Shoe)Carnival)

Foot)Locker)

Genesco)

Ratios Against Competitors

Equity Research | November 5, 2015 | NYSE: DSW Analysts: Hailey Davis, Isabella Duarte, Brandon Moore, Bridget Parsells 7

8.

Recommendation: BUY

Equity Research | November 5, 2015 | NYSE: DSW Analysts: Hailey Davis, Isabella Duarte, Brandon Moore, Bridget Parsells 8

Business Model

The DSW Business Model has recently switched to become customer-centric. All shoe inventory is strategically

placed on the sales floor to invite customers to try each shoe at his or her own pace. With all the inventory on

display, customers are welcomed to more tailored shopping experiences without sales pressure from employees

and without prolonged waiting times. The store continues to deliver everyday low prices instead of fluctuating

between regular and sales pricings.

Its stores are also mini-distribution centers capable of product deliveries. In cases where inventory is unavailable,

orders are directed for fulfillment from nearby locations. What differentiates DSW from other retailers is its ability to

understand meeting demand generated across the board, regardless of fulfilling orders from the same store.

Orders are taken from the mini-distribution channels and consolidated

between stores and from dot.com, making DSW more flexible to

gratify its customer needs.

Furthermore, DSW strives to place the correct shoes in their

correspondingly labeled boxes to avoid confusion and inventory

replenishment errors. DSW’s “size by store” model optimizes

inventory along with SAS data analytics. SAS automatically

recommends the most requested styles and sizes per individual

location to optimize inventory to meet demands. The result is a

reduction in obsolete inventory which would need to be sold at a

discount at season end, thus preventing loss of sales from stock-outs.

Revenue growth this quarter and general comparable store sales as

well as the omni-channel sales are benefitting from this switch in

processes. The store is highly benefitting from the implementation of its omni-channel where customers can

browse, compare, and order products from their smartphones in the DSW app, online from the website, and even

from sales personnel at in-store locations with timeliness, ease, and organization. Plus, the opening of multiple

small store concepts is improving from significantly smaller box sizes, thus presenting additional growth opportunity

for markets where only small stores can be placed.

9.

Recommendation: BUY

Equity Research | November 5, 2015 | NYSE: DSW Analysts: Hailey Davis, Isabella Duarte, Brandon Moore, Bridget Parsells 9

Valuation

EV/EBITDA Valuation:

Multiple valuation methods were used to arrive at a target price for 2020. The first model used is an EV/EBITDA multiple

model. DSW currently trades at an EV/EBITDA multiple below its five-year historical average. Its five-year historical average

EV/ EBITDA multiple is 7.81 times (see appendices page #19). We expanded the multiple over our investment horizon due to

its improved omni-strategy that will increase revenues. At 7.6 times EBITDA, DSW will have a market cap of over $2.9 billion

and an equity value per share of $35.83.

We conducted a

sensitivity

analysis on the

multiple to

account for the

improving efforts

of its marketing

strategy to help

drive customer

traffic.

EV/EBITDA Sensitivity Analysis:

10.

Recommendation: BUY

Price/Earnings Valuation:

Equity Research | November 5, 2015 | NYSE: DSW Analysts: Hailey Davis, Isabella Duarte, Brandon Moore, Bridget Parsells 10

A P/E model was also conducted to help obtain a price target for 2020. We modeled for P/E expansion. The historical P/E

multiple for the last five years is 17.51 (see appendices page #18). During our investment horizon, DSW’s P/E will expand to

a multiple of 17.42. DSW’s P/E multiple will continue to expand as as the economy continues to improve and consumers

spending more disposable income on shoes. DSW will take market share away from its competitors as it continues to improve

its omni-channel and marketing strategies to obtain customers.

Price/Earnings Sensitivity Analysis:

A sensitivity analysis was also conducted to reflect what the firm’s price target could be at different multiples during 2020. The

bear case assumes the P/E expands to only 16.42 and DSW’s 2020 EPS is $1.69. Yielding a 5.78% annualized return. The

bull case assumes the P/E expands to 18.42 and DSW’s 2020 EPS is $2.19. Yielding a 13.99% annualized return. According

to all of our multiples, there is still strong upside with very little downside risks at DSW’s current price. This supports our

recommendation of a strong buy on DSW.

11.

Recommendation: BUY

Equity Research | November 5, 2015 | NYSE: DSW Analysts: Hailey Davis, Isabella Duarte, Brandon Moore, Bridget Parsells 11

Free Cash Flow to Equity Valuation:

We used a free cash flow to equity model to value what DSW is worth today. Our model implies that the stock is 36.47%

undervalued on our base case scenario. The model has implied assumptions based on our expectations of the firm, its

competitors, and the industry landscape.

* Top line growth will increase with higher number of members joining the customer loyalty program and by improvements

in the omni-channel strategy

* Capital expenditures will increase at a moderate rate due to the firm’s plan on increasing its store count in future years to

come

* Using a 60-month regression, we arrived to a beta of 1.3 that was used in calculating the discount rate. Since shoes are

relativity inelastic, we believe this to be in line with our assumption.

Free Cash Flow to Equity Sensitivity Analysis:

We also conducted a scenario analysis by changing the discount rate and terminal price to account for the

possibility of unsuccessful election of the omni-channel strategy, fluctuations in prices of raw materials needed for

shoes, and uncertain general economic conditions.

The bear case implies that DSW is 27.97% undervalued, whereas our bull case implies that DSW is 45.26%

14.

Recommendation: BUY

Equity Research | November 5, 2015 | NYSE: DSW Analysts: Hailey Davis, Isabella Duarte, Brandon Moore, Bridget Parsells 14

Appendices Continued

15.

Equity Research | November 5, 2015 | NYSE: DSW Analysts: Hailey Davis, Isabella Duarte, Brandon Moore, Bridget Parsells 15

Recommendation: BUY

Appendices Continued

16. Equity Research | November 5, 2015 | NYSE: DSW Analysts: Hailey Davis, Isabella Duarte, Brandon Moore, Bridget Parsells 16

Recommendation: BUY

Appendices Continued

Chief Executive Officer- Michael R. MacDonald

Mike MacDonald’s annual compensation has been consistent with company performance

over the past year. He has been the CEO and President of DSW Inc. since April 27, 2009.

Mr. MacDonald has over 30 years of business experience in all phases of retail, including

managing merchandising, marketing, stores, operations and finance functions. He has

served as a CEO, CFO, President and COO, CAO, as well as a Senior VP and Chairman of

varying retail and department stores such as Sacks, Marshall Field & co, Northern

Department Stores Group and ShopKo Stores Operating Co in addition to Carson Pirie Scott

& Co, Dayton Hudson Department Stores, and Boston Store and Younkers. Additionally, he

has been an Independent Director of Ulta Salon, Cosmetics & Fragrance, Inc.

The average tenure of the DSW management team is approximately 4.6 years in length,

which is about average. The average tenure of the DSW board of directors is roughly 8.3

years long. The length of tenure is also average. In the past month, more shares have

been bought than sold by DSW management and board of directors with only one seller in the past three months

while 501,750 shares were bought. Currently the company Insiders own 18.8% of DSW Inc.

Executive Vice President and Chief Executive Officer Successor- Roger Rawlins

Mr. Rawlins has extensive retail leadership experience including nearly a decade of

experience with DSW. Prior to his current role, Mr. Rawlins served as Executive Vice

President, Omni Channel, Senior Vice President and General Manager of DSW.com and

Vice President, Finance and Controller. Prior to joining DSW in 2006, Mr. Rawlins served

in leadership positions at HER Real Living and L Brands Inc.

Management: