VAT Court Diary: For the period Monday 31 March 2014 to Friday 11 April 2014

•

0 likes•512 views

High level summary from Grant Thornton of upcoming VAT cases in the UK and European courts.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (15)

Similar to VAT Court Diary: For the period Monday 31 March 2014 to Friday 11 April 2014

Similar to VAT Court Diary: For the period Monday 31 March 2014 to Friday 11 April 2014 (20)

More from Alex Baulf

More from Alex Baulf (20)

Recently uploaded

Recently uploaded (20)

VAT Court Diary: For the period Monday 31 March 2014 to Friday 11 April 2014

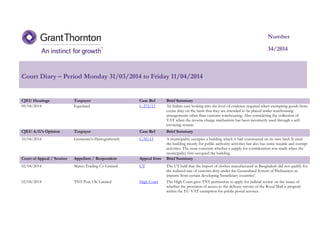

- 1. CJEU Hearings Taxpayer Case Ref Brief Summary 09/04/2014 Equoland C-272/13 An Italian case looking into the level of evidence required when exempting goods from excise duty on the basis that they are intended to be placed under warehousing arrangements other than customs warehousing. Also considering the collection of VAT when the reverse charge mechanism has been incorrectly used through a self- invoicing system. CJEU A/G’s Opinion Taxpayer Case Ref Brief Summary 10/04/2014 Gemeente's-Hertogenbosch C-92/13 A municipality occupies a building which it had constructed on its own land. It used the building mostly for public authority activities but also has some taxable and exempt activities. The issue concerns whether a supply for consideration was made when the municipality first occupied the building. Court of Appeal / Session Appellant / Respondent Appeal from Brief Summary 02/04/2014 Marco Trading Co Limited UT The UT held that the import of clothes manufactured in Bangladesh did not qualify for the reduced rate of customs duty under the Generalised System of Preferences as imports from certain developing 'beneficiary countries'. 02/04/2014 TNT Post UK Limited High Court The High Court gave TNT permission to apply for judicial review on the issues of whether the provision of access to the delivery service of the Royal Mail is properly within the EU VAT exemption for public postal services. Court Diary – Period Monday 31/03/2014 to Friday 11/04/2014 Number 34/2014

- 2. 2 Upper Tier Tribunal Appellant / Respondent Appeal from Brief Summary 01-03/04/2014 Taylor Clark Leisure Plc FTT The FTT held that the repayment claim submitted by Taylor Clark, the representative member of the VAT group, in respect of VAT on income from bingo and gaming machines of a trading subsidiary was out of time on the basis that the rights to a VAT refund were passed to a third party on the sale of the shares. Taylor Clark has appealed the decision. 10-11/04/2014 Isle of Wight Council (and others) FTT The issue at point in this case is whether the provision of off street car parking by a Local Authority should be subject to VAT or whether it should be treated as a 'non- business' activity given the Public Body status of the Local Authority. Following a judgement from the CJEU in respect of the interpretation of ‘significant distortion of competition’ this case was reheard by the FTT. The FTT dismissed the Council's appeal on the grounds that there was no doubt that Local Authorities are in competition with commercial providers of off street parking and the treatment of Local Authorities as non-taxable persons in relation to such provision would lead to significant distortion of competition. The Council has appealed. 11/03/2014 Roger Skinner Limited FTT The FTT held that supplies of certain dog foods fell within the zero-rating provisions as "biscuits and meal for cats and dogs". HMRC has appealed this decision.