Architecture- easements and valuations

•Download as PPTX, PDF•

2 likes•1,631 views

Easements are certain rights connected with enjoyment o immovable property. The easement rights and obligation arise as a result of local or general custom. It is the right which the owner or occupier of a land possesses for the beneficial enjoyment of that land. The Land on which the right of beneficial enjoyment has been created is called the dominant heritage (owner: Dominant owner) The land on which easement is created is called the Servient heritage ( owner: Servient owner)

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Architecture- easements and valuations

Similar to Architecture- easements and valuations (20)

More from Aditi Garg

More from Aditi Garg (15)

Recently uploaded

Recently uploaded (20)

Architecture- easements and valuations

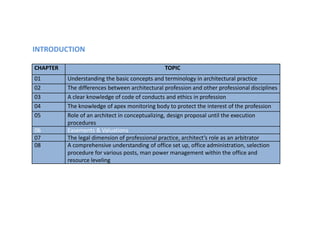

- 1. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 INTRODUCTION CHAPTER TOPIC 01 Understanding the basic concepts and terminology in architectural practice 02 The differences between architectural profession and other professional disciplines 03 A clear knowledge of code of conducts and ethics in profession 04 The knowledge of apex monitoring body to protect the interest of the profession 05 Role of an architect in conceptualizing, design proposal until the execution procedures 06 Easements & Valuations 07 The legal dimension of professional practice, architect’s role as an arbitrator 08 A comprehensive understanding of office set up, office administration, selection procedure for various posts, man power management within the office and resource leveling

- 2. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 MISCELLANEOUS TOPICS EASEMENTS Easements are certain rights connected with enjoyment o immovable property. The easement rights and obligation arise as a result of local or general custom. It is the right which the owner or occupier of a land possesses for the beneficial enjoyment of that land. The Land on which the right of beneficial enjoyment has been created is called the dominant heritage (owner: Dominant owner) The land on which easement is created is called the Servient heritage ( owner: Servient owner)

- 3. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 EASEMENTS Easements right are acquired by the following ways: 1. By prescription 2. By express grant 3. By implied grant 4. By custom When an owner allows people to pass through his land without any objection or obstruction for a continuous period of 20 years or allows the neighbor to enjoy light and air from his property, the easement created is called Easement by prescription

- 4. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 EASEMENTS Easements right are acquired by the following ways: 1. By prescription 2. By express grant 3. By implied grant 4. By custom When an owner permits people to pass through his land with the full knowledge and consent to create some kind of right through a written agreement, the easement created is called Easement by Express Grant

- 5. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 EASEMENTS Easements right are acquired by the following ways: 1. By prescription 2. By express grant 3. By implied grant 4. By custom When an owner sells a rear portion of his property which does not have an independent access, it is implied that he will permit the purchaser to pass through his land, the thus easement created is called Easement by Implied Grant

- 6. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 EASEMENTS Easements right are acquired by the following ways: 1. By prescription 2. By express grant 3. By implied grant 4. By custom When people enjoy certain rights to make use of a piece of land for a social activity year after year as a custom, it is said to be an Easement by Implied Grant

- 7. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 VALUATION Valuation is defined as the process of determining the fair value of a specific property for a specific purpose on a specified date. Valuation is done using an established and appropriate method of valuation. Valuation is done by a specially qualified valuer wo has acquired specialized training and experience.

- 8. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 VALUATION Valuation is done for a variety of reasons 1. Valuation for Sale or Purchase 2. Valuation for Legal purpose 3. Valuation for Taxation purpose 4. Valuation for Compulsory Acquisition 5. Valuation for Accounting purposes 6. Valuation for Insurance purposes

- 9. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 VALUATION Valuation is done for a variety of reasons 1. Valuation for Sale or Purchase One of the most common purposes- prospective seller quote the maximum, the purchaser offers the lowest sum. An expert valuer determines the value on the basis of a number of transaction that have taken place in a particular are which is comparable in size, location, condition and usage. 2. Valuation for Legal purpose Required for legal purposes like obtaining a probate of a will, division of assets among it owns or business partners, determining the value for stamp duty or court fee or

- 10. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 VALUATION Valuation is done for a variety of reasons 3. Valuation for Taxation purposes Properties are valued for the purposed of deciding the tax liability in the event of gifting or sale of property to determine the tax required to be paid. This may in turn decide the wealth tax that the seller may be required to pay. 4. Valuation for Compulsory Acquisition Whenever a public body needs a piece of privately owned property, it is notified for acquisition. A valuer prepares claim of compensation in which he values the land under acquisition as per established norms.

- 11. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 VALUATION Valuation is done for a variety of reasons 5. Valuation Accounting purposes Properties are periodically valued to determine the value of assets of companies for accounting purposes ( to be included in annual reports to shareholder, partners) 6. Valuation for Insurance Acquisition Properties are valued for determining the “Insured value” for the purpose of working out the amount of premium the owner must pay to the insurance company. (and for the compensation to be paid in the event of loss due to any reason)

- 12. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 APPRECIATION AND DEPRECIATION Appreciation and depreciation are issues that come up frequently on the Real Estate License Exam. APPRECIATION is an increase in a property’s value caused by factors like inflation, increasing demand, and improvements to the property. DEPRECIATION is a decrease in the value of a property caused by lower demand, deflation in the economy, deterioration, or the influences of other undesirable factors.

- 13. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 APPRECIATION AND DEPRECIATION Deprecation is calculated mathematically but the basis of calculation depends on the expert’s judgement based on his experience. Different method for calculating the depreciation of a property 1. Accelerated Depreciation method 2. Straight-line Depreciation method 3. Sinking fund depreciation method

- 14. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 APPRECIATION AND DEPRECIATION 1. Accelerated Depreciation method: Accelerated depreciation is the depreciation of fixed assets at a fast rate early in their useful lives. This type of depreciation reduces the amount of taxable income early in the life of an asset, so that tax liabilities are deferred. 2. Straight-line Depreciation method: Straight line depreciation is the default method used to gradually reduce the carrying amount of a fixed asset over its useful life. The method is designed to reflect the consumption pattern of the underlying asset, and is used when there is no particular pattern to the manner in which the asset is to be used over time. Use of the straight-line method is highly recommended, since it is the easiest depreciation method to calculate, and so results in few calculation errors. 3. Sinking fund depreciation method: Under this method, a fixed amount is debited every year to depreciation amount and credited to depreciation fund account instead of asset account. The asset is shown at its original cost, in the books, in every year. The amount which is credited in the sinking fund, is invested in gilt-edged securities. Sinking fund method makes available a sum of money for the replacement of asset by maintaining separate provision

- 15. ARC 404 : PROFESSIONAL PRACTICE B.ARCH VI SEMESTER : FEBRUARY 2015 References 1. http://www.coa.gov.in/home/home.htm 2. http://www.robertcoolidge.com/process-1.html 3. http://www.dummies.com/how-to/content/how-to-calculate- appreciation-and-depreciation-for.html 4. http://www.accountingtools.com/straight-line-depreciation 5. Architectural Practice in India: Prof. Madhav Deobhakta & Ar. Meera Deobhakta