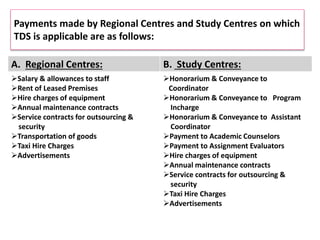

1. Payments made by Regional Centres and Study Centres on which

TDS is applicable are as follows:

A. Regional Centres: B. Study Centres:

Salary & allowances to staff

Rent of Leased Premises

Hire charges of equipment

Annual maintenance contracts

Service contracts for outsourcing &

security

Transportation of goods

Taxi Hire Charges

Advertisements

Honorarium & Conveyance to

Coordinator

Honorarium & Conveyance to Program

Incharge

Honorarium & Conveyance to Assistant

Coordinator

Payment to Academic Counselors

Payment to Assignment Evaluators

Hire charges of equipment

Annual maintenance contracts

Service contracts for outsourcing &

security

Taxi Hire Charges

Advertisements

2. Statutory responsibility for TDS has been placed on any

‘person’ responsible for paying income chargeable under the

head ‘Salaries’.

In the case of employees of IGNOU appropriate disbursing

officer is person responsible for paying salary. Hence

responsibility of TDS lies on the DDO.

PAYERS, WHO ARE COVERED U/s 192

3. Do’s & Don’ts for Deposit of Tax

Sl. Do’s Dont’s

(a) Use Challan Type - ITNS 281 (a) Don’t use single challan to deposit

tax under various sections.

(b) Quote correct TAN of the deductor (b) Don’t use single challan to deposit

tax deducted for Corporate and Non-

corporate deductees.

(c) Use separate challan to deposit TDS under

each section & indicate the correct nature of

Code.

(c) Don’t make any mistake in the

Assessment Year to be indicated in

the challan.

U/s Nature of Payment Code (d) If you have multiple TANs for the

same division filing TDS returns,

don’t use different TANs in different

challan. Use one consistently &

surrender the others.

192 Salary 92B

194A Interest other than Interest on securities 94A

194C Payment of contractor or sub-contractor 94C

194H Commission or Brokerage 94H

194I a) Rent on equipment 4 IA

194I b) Rent on building or furniture & fixture 4 IB

194J Fees for professional or Technical Services 94J

4. Effect of mistake done by the Deductor or

the Outsourced Professional

If error is made by Deductor or Outsourced

Professional w.r.t.

If wrong PAN is entered, no credit will be

available to the deductee due to non-reflection in 26AS

If name is wrongly entered, credit of TDS will

still be available, because it is PAN based

If address is wrongly entered, credit of TDS will

still be available, because it is PAN based

Although credit of TDS will be available, but his Income will

be wrongly reflected in his TDS certificate.

Although credit of TDS will be available,

but it can result in application of interest .

Deductee will not get benefit of tax credit

because 26AS shows status ‘U’

means Unmatched.

Deductee will not get benefit of tax credit

because 26AS shows status ‘U’

means Unmatched.

Deductee will not get benefit of tax credit

because 26AS shows status ‘U’

means Unmatched.

Deductee will not get benefit of tax credit

because 26AS shows status ‘U’

means Unmatched.

Demand will be raised by TDS Department on the Deductor, along with Interest @ 1% P.M.

PAN

NAME

ADDRESS

CREDIT AMOUNT

CREDIT DATE

WRONG SECTION

OF TDS

CHALLAN BSR CODE

CHALLAN DATE

BANK NAME

TDS RATE

OUTSOURCED

PROFESSIONAL

Generates

FVU* File

& uploads

through e-

filing on

NSDL Site

5. Rates for Tax Deduction at Sources on Various Payments

Nature of

Payment

Threshold Limit TDS (Surcharge : NIL,

CESS :NIL on Payments

Other than Salary)

Payment of salary –

U/s 192

Age :

- below 60 years RRs.2,00,000

Note: 1 U/s 80EE : Deduction U/s 80EE upto Rs. 1Lac being

interest on loan for acquisition of residential house shall be

admissible w.e.f. 1st April 2014.

Note:2 W.e.f. 1st April 2014, Rebate U/s 87A: Resident

Individual whose Total Income does not exceed Rs.5 Lacs

shall get a rebate of Rs. 2,000 or 100% of Tax Payable

whichever is lower.

Average of Income-tax

computed on basis of

the rate in-force for the

Financial Year as

follows:

0- Rs.2 Lacs - NIL

Rs.2 Lacs-Rs.5 Lacs – 10%

Rs.5 Lacs- Rs.10 Lacs – 20%

Above Rs.10 Lacs – 30%

(Plus Education Cess

& SHEC : - 3%)

6. Nature of Payment Threshold

Limit

TDS (Surcharge : NIL,

CESS : NIL)

Interest other than interest on

securities – U/s 194 A

Rs. 5,000 per

annum

10 %

Payment / credit to a

contractor/sub-contractor

U/s 194 C

Rs. 30,000 per

contract or

Rs. 75,000 per

annum in

aggregate

a. Individual / HUF 1%

b. Other than an 2%

individual /HUF

(e.g.: Company/Firm)

Commission or Brokerage -U/s 194 H Rs. 5,000 per

annum

10%

Rent U/s 194 I

a. On Equipment

b. On Building or Furniture

Rs. 1,80,000 P.A.

Rs. 1,80,000 P.A

2%

10%

Fees for Professional or technical

services – U/s 194 J

Rs. 30,000 per

annum

10%

7. Appointment Letters of Coordinators

The Coordinator is responsible :

1. for all the activities of the Study Centre. He shall coordinate

the work of all the individual counselors and act as a liaison

between the University Regional Centre and the Study Centre.

2. for maintenance of all records and registers in respect of all

activities of the Study Centre either academic or

administrative.

3. to ensure discipline in the Study Centre consistent with the

aims and objects of the University.

4. to perform such other duties, as are assigned by University

from time to time for the effective functioning of Study Centre.

8. Payment to Consultant

Where IGNOU engages an employee as a Consultant on part-time basis on

contract, remuneration paid to such Consultant is liable for TDS

i) U/s 194J

(Professional

Services)

Where Contract is FOR SERVICE:

Where the employer such as IGNOU engages

services of Professional on basis of Agreement

which gave them choice of time to come to IGNOU

for providing their professional services and they

were not on roll of IGNOU as its employees, there

was no Employer-Employee relationship and

payments to them is covered U/s 194J.

ii) U/s 192 (Salary) Where Contract is OF SERVICE:

Where the employer can demand services from

employee as part of employment service.

9. Features of Contract FOR SERVICE

• (Commissioner of Income Tax V. Coastal Power Co. [2007]

162 Taxman 120 )

1. A.K. Bhatnagar was an employee of Coastal Power Co.

2. He was drawing salary from Coastal Power Co.

3. in addition to that under a separate Agreement, he was given a Consultancy

Assignment which had the following covenants :

i) Consultancy was on temporary basis;

ii) Consultant was not entitled to participate in welfare plans – such as

Medical plans, Travel Accident Plan etc.

iii) Consultant would indemnify the employer against all liabilities

Delhi High Court held that in view of the above covenants, there is no Employer-

Employee relationship and payments are not covered U/s 192 as Salary but covered

U/s 194J as Professional Fees.

10. Features of Contract OF SERVICE

1. Where the employer can demand services from employee as part of

employment service.

2. To treat an amount as salary – Payment must not have been received by the

service provider in course of carrying on profession, because fees for technical

services includes any consideration received from rendering managerial,

technical or consultancy services but excludes any consideration which would

be income of the recipient chargeable under the head ‘SALARIES’.

(United Hotels Ltd. V. ITO [2005] 2 SOT 264) (Delhi-Trib.)

3. In one case, a hospital had, apart from regular employees, engaged consultant

doctors on contract basis, and paid them remuneration in the form of share in

the fees charged by it from the patients, subject to a specified minimum agreed

amount. They were treated as employees falling under the category of fixed

period/contract employees and / or part-time employees, thereby resulting in

the existence of employer-employee relationship.

11. Conclusion:

• Remuneration paid to part time teachers for assignments are covered as

salary U/s 192, and not as fee for Professional Services U/s 194J or

Contract U/s 194C.

This has been held by the Authority of Advance Ruling in Max Muller

Bhawan Case (2004) 268 ITR 31 (AAR).

12. Judicial decisions on TDS on Salary U/s 192

a) Section 192 requires that deduction from salary is to be made at the

time of payment and not at the time when salary become due.

[Citigroup Global Markets India (P) Ltd. V. DCIT (2009) 29 SOT 326 (Mum.) ].

b) If any tax has been deducted in excess in the earlier months, the

employer is authorized to adjust such excess in the subsequent

months. Visa-versa, if the employer has deducted less tax in the

earlier months, he will have to make higher deduction in the

subsequent months.

[Hero Honda Motors Ltd. V. ITO [2004] 112 Taxman 154 (Delhi) (Mag.)]

The above adjustment is permissible only in respect of same employee

and not for all employees.

Interest u/s 201(1A) is not leviable if the exact amount of TDS is not

deducted each month. [ITO V. Asia Hotels Ltd. (1991) 41 TTJ (Del) 28].

13. Judicial decisions on TDS on Salary

c) If after the year is over, there is a short deduction of tax due to honest

and bonafide belief by the employer and employee make good this

short fall in his Return of Income the employer is not to recover such

short fall and he cannot be penalized.

[Gwalior Rayon Silk Ltd. V. CIT (1983) 140 Income Tax Return 832

(MP)].

But at the same time employer cannot take TDS on salary casually and

resort to a lump-sum deduction at the end of Financial Year for making

good the deficiency. [Madhya Gujrat Vij Co. Ltd. V. ITO [2011] 14

taxmann.com 156 (Ahb.-Trib.)].

Controversy with the Department normally arises when such variation

is adjusted in last quarter or last month.

d) If employee incurring loss from house property furnishes verified

statement as per Rule 26B, benefit of the same can be given in TDS.

14. Judicial decisions on TDS on Salary

e) Deduction U/s 80G will generally not be allowed for purpose of TDS.

However, contribution made by employee through employer to Prime

Minister National Relief Fund, CM Relief Fund, LG Relief Fund will be

admissible on basis of certificate issued by DDO. [Circular No. 2/2005

dated 12.01.2005]

f) Salaried employees drawing house rent allowance upto Rs. 3,000 per

month will be exempted from production of rent receipt to the

employer.

g) Where the Head Office or the Branch Office is already filing the return

under Section 206, no other Assessing Officer shall require the

assessee to file such a return with him.

[Circular No. 719 dated 22.08.1995]

15. Judicial decisions on TDS on Salary

h) Although earlier the Supreme Court had held in . [CIT V. ITI Ltd. (2009)

183 Taxman 219 (Supreme Court) ] that there is No statutory

obligation of the employer to collect supporting evidence to the

declaration given to show that the employee has actually utilized

amount paid towards leave travel concession or conveyance

allowance for purpose of TDS U/s 192, but subsequently the CBDT has

issued Circular No. 8/2012 [F.No- 275/192/2012-IT(B)] dated

05.10.2012 as per which :

“the employer has to satisfy the obligation that leave travel (fare)

concession is not taxable in view of Section 10(5), the employer is not

only required to be satisfied about the ingredients of the said clause

but also to keep and preserve evidence in support thereof”.

16. Some More Points on TDS on Salary

1. Special Allowance exempt under Section 10(14):

Allowance, not in the nature of perquisite, granted to meet expenses

wholly, necessarily & exclusively incurred in the performance of duties to

the extent to which actually incurred & proof of expenditure furnished to

the employer.

2. Where IGNOU pays amount to another partner institute towards

reimbursement of salaries of certain personnel of that institute who are

deputed for rendering services to IGNOU, the amounts so reimbursed to

that institute will not be subject to TDS because there was no contract

between IGNOU & the deputed personnel by virtue of which IGNOU could

demand services from the deputed personnel and that personnel could

not claim fees directly from IGNOU since there was no specific contract

between IGNOU & the deputed personnel.

3. If those deputed personnel are not carrying on the specified profession,

they will not be covered for TDS U/s 194J.

17. Claim for credit of TDS in the year in which relative

income is offered for tax:

• Section 198 provides that TDS deducted is

deemed to be income received. Hence, even

when the relative income is received later, to

the extent of TDS, income is deemed to be

received in the year of deduction of TDS.

18. TDS on Contract Payment U/s 194C

a) In absence of a contract section 194C does not come into play.

b) TDS will be deducted on invoice value excluding the value of material purchased

from such customer if such value is mentioned separately in the invoice.

c) Where the contract of work is given on piece rate basis and the total payment

was not expected to exceed RRs. 75,000 but later on it is found that the payment

exceeds that amount, deduction should be made in respect of earlier payments

as well. [Circular No. 93, dated 26.09.1972]

d) There will be no requirement to deduct TDS of those authorities or bodies whose

income is unconditionally exempt U/s 10 of Income Tax Act, 1961 and who are

statutorily not required to file Return of Income U/s 139. [Circular No. 4/2002,

dated 10.07.2002]

e) In composite contracts if Invoice is raised, separately mentioning the value of

material supplied, no deduction is required to be made U/s 194C for the value of

material supplied, even if the said agreement is part of a composite transaction.

[CIT v. Karnataka Power Transmission Corporation Ltd. 49 ITCL 167].

19. TDS on Contract Payment U/s 194C

f) Where different contracts entered with sister concern are found to be in nature

of a single integrated agreement termed as “Works Contract”, deduction of TDS

U/s 194C is applicable for the entire payment.

[Essar Oil Ltd. v. ITO 30 Taxmann.com 39]

g) In respect of outsourcing services received from placement agencies, even if

separate bills are raised, one for salaries of outsourced persons and second for

service charges of the placement agencies, TDS @ 2% U/s 194C will be applicable

on the entire payment made to the placement agency.

h) Similar treatment will be done for payments made to Security Agencies.

20. Payment for Hiring Goods Carriage

1. Provisions of Section 194C will be applicable. Threshold limit will

be Rs. 30,000 for each GR and Rs. 75,000 in aggregate for the

whole year.

2. TDS is not to be deducted if transporter furnishes PAN to the

deductor. Its details have to be furnished in E-TDS Return.

3. If transporter does not furnish PAN to the deductor, TDS will be

deducted @20% of the value, which will also be reported in the E-

TDS Return but the deductee will not be entitled to claim credit of

the TDS.

4. TDS U/s 194C is applicable on Hire Charges of taxi in excess of Rs.

30,000 for each duty and Rs. 75,000 in aggregate for the whole

year.

21. Professions covered for fees U/s 194J are:

Sl. No. Professions covered for fees U/s 194J

1 Legal Profession

2 Medical Profession

3 Engineering

4 Architecture

5 Accountancy

6 Technical Consultancy

7 Interior Decoration

8 Advertising

9 Any other profession notified by CBDT for purpose of maintaining

Books of Accounts U/s 44A. They are:

a) Authorized Representative before legal authority

b) Film Artist

22. Sl. No. Professions covered for fees U/s 194J

9 c) Information Technology Professional : Notified Technology enabled

products or services are:

Back-office Operations

Call Centres

Content Development or

Animation

Data Processing

Engineering and Design

Geographic Information System

Service

Human Resources Services

Insurance Claim Processing

Payroll

Remote Maintenance

Revenue Accounting

Support Centres, and

Web-Site Services

It does not mean that any Managerial or Agency Services can be covered as

Professional or Technical Services U/s 194J.

[GlaxoSmithkline Consumer Healthcare Ltd. V. ITO [2007] 12 SOT 221 (Del.)]

Where professional raises a separate bill for reimbursement of Out of Pocket

Expenses such as conveyance, boarding/lodging etc., on which there is no element of

profit, TDS is to be made only on fees component & not on the reimbursement

component. [ITO v. Dr. Willmar Schwabe India(P) Ltd. [2005] 3 SOT 71 (Delhi-Trib.)

23. Application of Section 194J on Fees for Technical Services

Only when technology or technical knowledge of a person is made

available to others and not where by using technical system,

services are rendered to others.

e.g.: If charges are paid to Electricity Transmission Company for

operation and maintenance of transmission lines for use of the

transmission lines, there is no technical service rendered by the

transmission company.

Therefore deduction of TDS is Not Applicable for rendering

Transmission Service.

(Jaipur Vidyut Vitran Nigam Ltd. V. Dy CIT [2009] 123 TTJ (JP-Trib.)

888)

24. Brokerage & Commission U/s 194H

Where a franchisee operates education centre jointly and

shares revenue on account of composite services provided by

them, on amount shared and remitted to Franchisee for

infrastructural claims, TDS is not deductable as rent U/s 194I.

[ACIT Vs. Nib Ltd. (2008) SOT 44 (Del) (URO)]

Further section 194C can be attracted only when one person

provides service to another, and not when there is payment for

use of one person’s trade Name or Goodwill by the other

person.

[Career Launchers (India) Ltd. v. ACIT 250 CTR 240 (Delhi)].

25. TDS on Rent U/s 194I

1. On aggregate amount exceeding Rs. 1,80,000 paid to each

landlord individually during Financial Year.

2. Rent on :

- Land, Building, Furniture & Fixture : TDS @ 10%

- Equipment Hire : TDS @ 2%

3. TDS is to be made on Advance Rent at the time of paying the

Advance. The deductee can claim credit as and when the

rental income is offered for taxation by him.

Language of Rent Agreement is important to determine how

& when the Advance Rent is adjustable in order to trigger the

liability of TDS on Advance Rent.

26. TDS on Rent U/s 194I

4. Payment to Hotels:

Earlier, payments to hotels was notified by Circular No. 681,

dated 08.03.1994 as a contract covered U/s 194C.

However, following a writ in the case of East India Hotels Ltd.

v. CBDT [2009] 320 Income Tax Return 526 (Bom.), the

Circular was held to be bad in law. As a result payment to

hotels is now not covered U/s 194C.

Further, as per Circular No. 715, dated 08/Aug/1995,

payments made to hotels for rooms hired on “Regular Basis”

would be in the nature of rent subject to TDS U/s 194I.

27. TDS on Rent U/s 194I

• “Regular Basis” has been defined where

rooms are earmarked at specified rate. But

where it merely a rate contract and there is no

obligation on part of the hotel to provide a

room or specified set of rooms, the occupancy

will be considered as concessional or casual,

as a result provisions of Section 194I will Not

Apply.

28. Purchase of Land – TDS involvement U/s 194 IA

In this case “Immovable Property” means Land (Other

than Agricultural Land) or any building or part of a

building. Tax shall be deducted @ 1% of such sum, if

the consideration paid or payable for the transfer of

such property is Rs. 50 lacs or more.

29. Clarification by CBDT on the correct scope of TDS on

specific services:

Sl.

No

Payment to Covered

U/S

Reasons

1 Recruitment Agency 194J It is not for carrying out any

work for supply of labour but

is payment for services

rendered.

2 Sponsorship of debates/seminar &

other functions held in university

with a view to earn publicity

through display of banners

194C The essence is for carrying out

work of advertisement.

3 Cost of advertisement issued to

souvenirs

194C The essence is for carrying out

work of advertisement

4 Advertisement Contract for release

covers the gross amount including

bills of Media

194C @1% of Gross Amount of the

bill.

30. Sl.

No

Payment to Covered

U/S

Reasons

5 Advertisement payment made

directly to Government agency

like Doordarshan

No TDS Government agencies are

exempted.

6 Contract for supply of printed

material as per prescribed

specification

194C It is a contract for carrying out

work under contract.

7 Software acquired in

subsequent transfer without any

modification

No TDS The receiver obtain a Declaration

from the Transferor of the

software that TDS U/s 194J has

been deducted for any previous

transfer of such software.

[Notification No.-21/2012 dated

30.06.2012]

8 Composite Agreement for use of

premises & provision of man-

power

194I Where essence is taking

premises on rent.

31. Sl. No Payment to Covered

U/S

Reasons

9 Deposit given to landlord against

rent

194I Only if deposit is adjustable

against future rent.

10 Payment to regular electrician on

contract basis

194C It is a contract for carrying out

the work.

11 Maintenance contract including

supplies spares:

Routine Maintenance

Technical Services

194C

194J

It is a contract for carrying out

the work.

It is a technical consultancy.

32.

33. Exemption of Allowances

• Leave Travel Allowance

• Leave Encashment

• Medical Benefits

• House Rent Allowance

• Children Education Allowance

• Hostel Expenditure Allowance

• Academic Allowance

• Uniform Allowance

• Transport Allowance

• Hill Area Allowance

34. Leave Travel Allowance

i) Leave Travel Allowance (LTC) : is limited to amount of travelling of an

employee and his family members (upto 2 surviving children born after 1st

October 1998)

ii) Allowed twice in the Block of 4 Calendar year :

(Current Block is 2010-13)

(Next Block is 2014 – 17)

Where no LTC is availed in the Block of 4 years, the amount can be availed

during the first calendar year of the immediately succeeding Block.

iii) Allowance is restricted to economy class of Air fare of National Carrier or A.C.

First Class for travelling to any place in India.

iv) If places are not connected by Air or Rail, the amount eligible will be the

amount of First Class or Deluxe Class fare of Recognized Public Transport

System.

(Where no Recognized Public Transport System exists, amount equivalent to

A.C. First Class Rail fare for equivalent distance of journey).

35. Leave Encashment

Leave Encashment on retirement will be exempt upto least of

the following:

• 10 months salary on basis of last 10 months average salary.

• Rs. 3 Lacs

• Amount equivalent to earned leave;

• Actual amount paid by the employer

• Entitlement to earned leave not to exceed 30 days for every

year of actual service.

36. Medical Benefits

In addition to reimbursement of amount spent for medical

treatment upto Rs. 15,000 in a Financial Year, the following are

also exempt for Medical Treatment of an employee or any other

family member (spouse/children/parents/dependant brothers &

sisters):

i) Treatment in hospitals maintained by

employer/Government/Local Authority;

ii) Treatment of prescribed disease in hospital approved by

Commissioner of Income Tax.

(DDO must obtain certificate of the hospital w.r.t. disease

and amount spent on treatment)

37. House Rent Allowance

Least of the following exempt:

• - 50% of salary

(if residential house is located in Delhi / Mumbai / Kolkata /

Chennai)

- 40% of salary if residential house is located in any other city.

• Actual House Rent Allowance received.

• Excess of rent paid over 10% of salary.

38. Children Education Allowance

• Rs. 100 per month per child upto maximum of 2

children.

• Employee can claim tax free education allowance U/s

10(14), and at the same time avail the rebate

U/s 80C in respect of tuition fee of 2 children.

Hostel Allowance

• Rs. 300 per month per child upto maximum of 2

children.

39. Academic Allowance

• Allowance upto any limit granted by employer for

encouraging academics, research & training in

educational and Research Institutions.

41. Transport Allowance

For conveyance to & fro place of duty:

• Upto Rs. 800 per month

• For Blind person the exemption is Rs. 1600 per

month.

42. Hill Area Allowance

• Exemption varies from Rs. 300 to Rs. 7000 per

month depending upon the specified place.

43. Allowances which are fully taxable

• Dearness Allowance

• City compensatory Allowance

• Lunch/Tiffin Allowance

• Overtime Allowance

• Non - Practising Allowance

• Family Allowance

• Servant Allowance

44. Valuation of perquisites

1 Interest free / Concessional Loan

2 Use of Moveable Assets

3 Rent free unfurnished accommodation taken on

lease / owned by employer

4 Valuation of perquisites on Motor Cars

45. Interest free / Concessional Loan

1. The difference between SBI Prime lending rate for similar type of loan as on

1st day of the year compared with the rate charged by the employer.

Type of Loan SBI Lending Rates

Housing Loan Varies from 9.95% - 10.10% p.a.,

depending upon loan amount

-Upto Rs. 30 Lacs : 9.95% p.a.

-Above Rs. 30 Lacs : 10.10% p.a.

Car Loan For term loan : 10.45% p.a.

For Overdraft : 10.15% p.a.

Two Wheeler Loan Upto 3 years : 17.95% p.a

Education Loan Upto Rs. 4 Lacs : 13.20% p.a.

Above Rs. 7.5 Lacs : 11.45% p.a.

(for girl students 0.50% concession in

interest rates)

46. Use of Moveable Assets

• Moveable assets like furniture is included in income @ 10% of original cost upto

10 years of the life of the asset

or

• Actual Hire Charges as reduced by amount recovered from the employer.

(Laptop/Computer are not treated as perquisite).

• On transfer of moveable assets, difference between WDV & the price at which

the asset is sold to employee.

• Depreciation rates to be considered on:

- Electronic Items Rates

- Computer 50%

- Motor Car 20%

- Other Assets 10%

47. Rent free unfurnished accommodation taken on Lease

1. Actual rent or 15% of salary, whichever is lower reduced by rent paid by the

employee.

2. Rent free unfurnished accommodation owned by employer :

Size of City in terms of Population Percentage (%) of Salary

Below 10 Lacs 7.5%

10 Lacs – 25 Lacs 10%

Above 25 Lacs 15%

48. Valuation of Perquisites on Motor Cars

Motor car owned

or taken on hire by

Expenses met by Value of Perquisites

Capacity up to

1.6 Ltrs.

Capacity above

1.6 Ltrs

Employer Employer Rs. 1,800 Rs. 2,400

Employer Employee Rs. 600 Rs. 900

Employer Employee Expenses –

Rs. 1,800 or actual

expenses for official

use (If proper

documents are

maintained)*

Expenses –

Rs. 2,400 or actual

expenses for official

use (if proper

documents are

maintained)*

In addition to above, the perquisite value shall be increased by Rs. 900 if driver is also

provided to run the motor car.

49. Eligible Deductions from Salary for Computing TDS

Sl. Section Particulars

1 80C • Life Insurance (Restricted to 10% of Capital Sum Assured)

•Contribution to PF/RPF/PPF

• Housing Loan Repayments

• Notified Mutual Fund/ UTI

• Tuition fees of any 2 children paid to University/College/

schools in India. (Full time education includes Play-school

activities, Pre-Nursery & Nursery classes

(Circular No. 5/2011, dated 16/August/2011]

•Term Deposit with Scheduled Bank for 5 years & above.

• 5 years Term Deposit with Post Office

Gross qualifying amount or Rs. 1 Lac, whichever is lower

Note: DDO can call for documents of investment made by

the employee, and cannot merely rely on declaration of

investment made by the employees (Circular No. 9/2005]

50. Sl. Section Particulars

2 80CCC • Contribution of Pension Fund: Amount eligible: Rs. 1 Lac

• Contribution for Annuity Plan of LIC or any other Insurer for

receiving Pension from the fund

3 80CCD • Contribution to Central Government Pension Scheme

• Amount eligible : 10% of Salary of the previous year.

NOTE: Aggregate deduction U/s 80C/80CCC/80CCD shall not exceed Rs. 1 Lac.

4 80CCG Investment in Rajiv Gandhi Equity Saving Scheme (RGESS):

• Gross total income of the employee should not exceed Rs. 12 Lacs

• The employee should be first time investor in Equity / Mutual Fund .

• Amount of deduction will be 50% of Investment subject to ceiling of

Rs. 25,000.

• The deduction can be spread over a period of 3 years commencing

from Assessment Year 2013-14.

5 80D • Premium for Health Insurance Policy

• Policy should be of an approved Insurer or approved scheme of GIC

• Employee can availed deduction for premium paid by parents

(including Rs. 5000/- for preventer Health Check-up and not

Diagnostic Check-up)

51. Sl. Section Particulars

6 80DD • Medical treatment of Handicap Dependant(s)

• Fixed deduction of : Rs. 50,000

• For severe disability : Rs. 1 Lac

(Obtain Certificate issued by Medical Authority)

7 80DDB • Medical treatment of specified disease : Rs. 40,000

• Where expenditure relates to Sr. Citizen : Rs. 60,000

(Age 60 Years )

8 80E • Interest on loan for Higher Education of the employee or any

relative (Spouse & children) of the employee

• No ceiling limit for the deduction

9 80EE • Interest upto Rs. 1 Lac on loan for Residential House Property for

A/Y 2014-15.

Condition : - Loan is sanctioned between 01 April 2013 to

31st March 2014.

• Value of the Residential House not to exceeds Rs. 40 Lacs

• Purchaser does not own any other residential house property on

the date of sanction of Housing Loan

• Amount of loan sanctioned does not exceeds Rs. 25 Lacs

• Where Interest is more than Rs. 1 Lac, balance amount will be

allowed as deduction in A/Y 2015-16

52. Sl. Section Particulars

10 80G For purpose of TDS the following will be eligible:

i) Donation to :

PM Relief Fund

CM Relief Fund

LG Relief Fund

National Defence Fund

Army Central Welfare Fund

Air Force Central Welfare Fund

Indian Naval Benevolent Fund

• Amount of deduction is whole of the amount subject to ceiling of

10% of Salary

11 80GG • Deduction in respect to House Rent paid for Residence subject to

not receiving HRA from employer

• Employee or is spouse or minor children does not own residential

house in the place where he is employed. Employee should file

declaration in Form-10.

•Amount eligible for deduction will be least of the following:

House rent paid in excess of 10% of his total income;

25% of total income

Rs. 2000 per month

53. Sl. Section Particulars

12 80U Deduction for Disability Allowance:

• Certified by Medical Authority

• Notified for purpose of the persons with Disabilities (Equal

Opportunities, Protections of Rights and Full Participation) Act, 1995.

• Deduction is not related to expenditure incurred by the employee

• a) amount of deduction : Rs. 5,000

• b) For Severe Disability : Rs. 75,000

54. Whether TDS is applicable on amount of Service Tax

i. No TDS on amount of Service Tax on Rent U/s 194I

A. Payment on rent may be liable to Service Tax but the payer does not have to deduct TDS on the

amount of Service Tax. For Example:

+ =

In this case payer has to deduct tax on Rs. 1,00,000 only and

not on Rs. 1,12,360.

B. TDS is applicable on amount of Service Tax on Professional & Technical U/s 194J. For Example:

+ =

If liable to Service Tax then the payer has to deduct TDS on Service Tax amount also.

In this case payer has to deduct tax on Rs. 1,12,360 & not on Rs. 1,00,000.

C. TDS is applicable on amount of Service Tax on Contract or Sub-Contract U/s 194C.

Payment on contract may be liable to Service Tax. The payer has to deduct the TDS on the Service

Tax amount also (As example B).

Rent

Rs. 1,00,000

Service Tax

Rs. 12,360

Total Value

Rs. 1,12,360

TDS on

Rs. 1,00,000

Rent

Rs. 1,00,000

Service Tax

Rs. 12,360

Total Value

Rs. 1,12,360

TDS on

Rs. 1,12,360

55. Preparation of TDS Returns

1. While preparing TDS return , please check all aspects such as:

A. Details of Deductor TAN of deductor

Name & Address of deductor

B. Challan details such as: • Challan Date

• Bank name in which TDS deposited

• BSR Code (7 digits)

• Challan No. (upto 5 digits)

• Against each Challan, indicate the details of deductee

on whose account the tax has been deducted

• Do not mention Challan No. as ITNS 281 .

Challan Serial No. generated by bank is to be entered.

C. Deductee Details PAN (10 digits) (alpha-numeric)

Name of Payee

TDS Amount paid

2. While depositing TDS

Challan

Use Challan No. 281 (ITNS)

Proper Head in which TDS to be deposited

Section Code such as 92B, 94C, 94J, 94I

Whether deductee is a Company or Non-Company

TAN & Name of Payee

56. 3. After deposit the TDS Challan: Check details regarding deposit of TDS made

by Deductor is Tallied with the data given by

banks

• Proper Stamp of Bank

• Clear Serial No. (Upto 5 digit)

• Clear Date

• Clear BSR Code (7 Digits)

• We can check the details provided by the

bank by using the Challan Status Enquiry on

TIN Website: www.tin-nsdl.com

• If bank has not uploaded your challan, you

may request the bank to upload the same.

If PAN not provided by deductee then TDS

will be @ 20% & deductee will not get credit

of TDS.

Preparation of TDS Returns

57. Prescribed Time Limit for Depositing TDS

NOTE:

If TDS is not deducted, then Interest will be charged @ 1% per month or part of a

month, but if TDS is deducted and not deposited, then interest will be charged 1.5%

per month or part of a month.

For Example:

TDS Amount - Rs. 40,000

Deducted on - April 20, 2013

Due Date - May 7, 2013

Paid On - May 22, 2013

Interest for - One month and 2 days – rounded off to 2 months

Interest Rate - 1%

Interest - 40000 X (1/100) X (2) = Rs. 800

APRIL TO FEBRUARY Within 7 Days of Next Month

MARCH 30TH APRIL

58. Prescribed manner of Payment for TDS

Deductor Relevant

Sections of

TDS

Bank where payment can

be made

Manner of

making

payment

Other than

Government –

such as

University

All Sections RBI or State Bank of India

or any authorised bank

Challan to

accompany

the payment

59. When payment made through challan at Bank, Challan Status Enquiry

www.tin-nsdl.com

Challan Status Enquiry

TAN Based View

Enter TAN & Period

Enter Amount

Confirm Amount

Check Challan Details

60. Prescribed Time Limit for Furnishing TDS Returns

NOTE:

(i) Late fee U/s 234E for late filing of TDS Return - Rs. 200 per day from the due

date. Fee shall not exceed total amount of Tax Deduction.

(ii) Section 271 H: It provides penalty ranging from Rs. 10,000 and Rs. 1,00,000 for

delay in furnishing TDS Return, but no penalty shall be levied if the TDS return is

furnished within 1 year of the due date after payment of the Tax Deducted

along with the interest and fees.

Ist Qtr Ended – 30th June 15TH July

IInd Qtr. Ended –

30th September

15TH October

IIIrd Qtr. Ended – 31st

December

15TH January

IVth Qtr. Ended – 31st

March 15TH May

61. Time Limit for Issue of TDS Certificates

Note: If the TDS Certificate is not issued within time limit prescribed, the payer will be liable for

penalty @ Rs. 100 for each day of default. Total penalty cannot exceed the TDS Amount.

FORM 16 for Salary Annually Due Date 31st May

FORM 16 –A for

Non- Salary Payments

Quarterly

Within 15 Days from the due date of

furnishing the TDS Return under Rule

31-A

Ist Qtr

30th June

IInd Qtr

30th September

IIIrd Qtr

31st December

IVth Qtr

31st March

TDS certificates to

be issued by

30th July

TDS certificates to be

issued by

30th October

TDS certificates to be

issued by

30th January

TDS certificates to

be issued by

30th May