Profile of the 2011 Irish Fair of Minnesota

•

1 like•286 views

This visitor profile of the 2011 Irish Fair of Minnesota includes items such as visitor demographics, willingness to pay admission, information sources, as well as a comparison of 2007 and 2011 visitors.

Recommended

More Related Content

More from University of Minnesota Tourism Center

More from University of Minnesota Tourism Center (20)

Profile of the 2011 Irish Fair of Minnesota

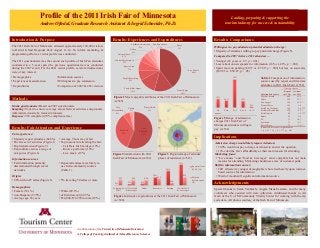

- 1. Leading, preparing & supporting the tourism industry for success & sustainability The 2011 Irish Fair of Minnesota attracted approximately 100,000 visitors to Harriet Island Regional Park August 11-14. To inform marketing & programming efforts, a visitor profile was conducted. The 2011 questionnaire was the second such profile of Irish Fair attendees conducted in a 5-year span (the previous questionnaire was conducted during the 2007 event). For the 2011 visitor profile, several attendee items were of key interest: Fair experience: • Majority repeat attendees (62.6%) • Diverse set of activities (Figure 1) • High satisfaction (Figure 2) • Expenditures across a range of categories (Figure 4) • Average 5 hour stay at fair • Top reasons for attending the fair: o Celebrate Irish heritage (19%) o Know a performer (14%) o Live music (13%) Information sources: • Fair information primarily disseminated through social networks. • Repeat attendees more likely to use Irish-community sources (Table 1). Origin: • 80% within 25 miles (Figure 3) • 5% traveling 50 miles or more Demographics: • Female (53.1%) • non-Hispanic (97.5%) • Average age 43 years • White (89.1%) • of Irish descent (69.3%) • $50,000-$74,999 income (19%) Table 1 Comparison of information sources used by repeat and first-time attendees to 2011 Irish Fair (n=532) % using source Information source Repeat (n=326) 1st-time (n=195) Word of mouth 48.5 43.6 Other 24.2 27.7 Newspaper 19.0 10.8 * Pioneer Press 10.1 5.6 Irish Fair Webpage 15.0 5.6 *** Irish Bar/Restaurant 12.0 6.2 * Irish Gazette 8.9 1.0 *** Radio 8.3 4.6 TV 7.1 10.3 Facebook 7.1 6.2 Poster/Flyer 7.1 2.6 * Indicates difference is significant at * p .05. ** p .01. *** p .001 Willingness to pay admission potential admission charge: • Majority of attendees willing to pay potential charge (Figure 5). Compared to 2007 visitors, 2011 attendees… • Younger (43 years vs. 47; p = .001) • Less reliant on newspapers for information (16% vs. 41%; p < .001). • Spent more on parking ($9.71 vs. $7.29; p < .000) but less on souvenirs ($39.91 vs. $50.87; p < .05) Results: Fair Attendees and Experience A collaboration of the University of Minnesota Extension & College of Food, Agricultural & Natural Resource Sciences Profile of the 2011 Irish Fair of Minnesota Andrew Oftedal, Graduate Research Assistant & Ingrid Schneider, Ph.D. Methods Onsite questionnaire: Based on 2007 questionnaire Sampling: Varied to ensure coverage across festival activities and grounds. Administered onsite by trained volunteers Response: 550 completed (70% compliance rate) Introduction & Purpose Live Music 40% Dance Stage 14% Food & Beverages 13% People Watching 8% Sports Area 7% Vendor Marketplace 4% Cultural Area 4% Other 4% Children's Activities 2% Pub Experience 3% Mass 1% Figure 1 Most enjoyable attributes of the 2011 Irish Fair of Minnesota (n=528) 17% 14% 55% 13% 2% No answer Zero $1-5 $6-10 >$11 2% 5% 6% 30% 54% 77% $21 $20 $20 $25 $10 $30 Lodging (in $10s) Off-site food & beverages Other Souvenirs Parking On-site food & beverages Spent at least $1.00 (%) Median dollars spent ($) Figure 4 Attendee expenditures at the 2011 Irish Fair of Minnesota (n=528) Figure 5 Range of admission charges 2011 Irish Fair of Minnesota attendees willing to pay (n=532) Special thanks to Sarah VanSickle, Angela Mens-Eastman, and the many volunteers who assisted with data collection. Additional thanks to Art Nash of the U of M Community Vitality Center for working with the zip code data. All photos courtesy of the Irish Fair of Minnesota. Results: Comparisons Very Satisfied 56% Satisfied 34% Very Dissatisfied 6% Unsure 3% Dissatisfied 1% Figure 2 Satisfaction with 2011 Irish Fair of Minnesota (n=522) Implications Admission charge would likely impact visitation: • 30.8% would not pay a charge or refused to answer the question. • 13% cited the fair’s affordability as their main reason for attending. Marketing focus: • “Live music” and “food & beverages” most enjoyable but not main reasons for attending. Marketing should use a mix of customer pulls. Shift in information sources: • 2011 attracted a younger demographic who relied heavily upon internet- based sources for information • Word of mouth still significant information source Acknowledgements Figure 3 Regional map of attendee places of residence (n=513) Results: Experiences and Expenditures • Demographics • Experiences & satisfaction • Expenditures • Information sources • Willingness to pay admission • Comparison of 2007 & 2011 visitors Leading, preparing & supporting the tourism industry for success & sustainability