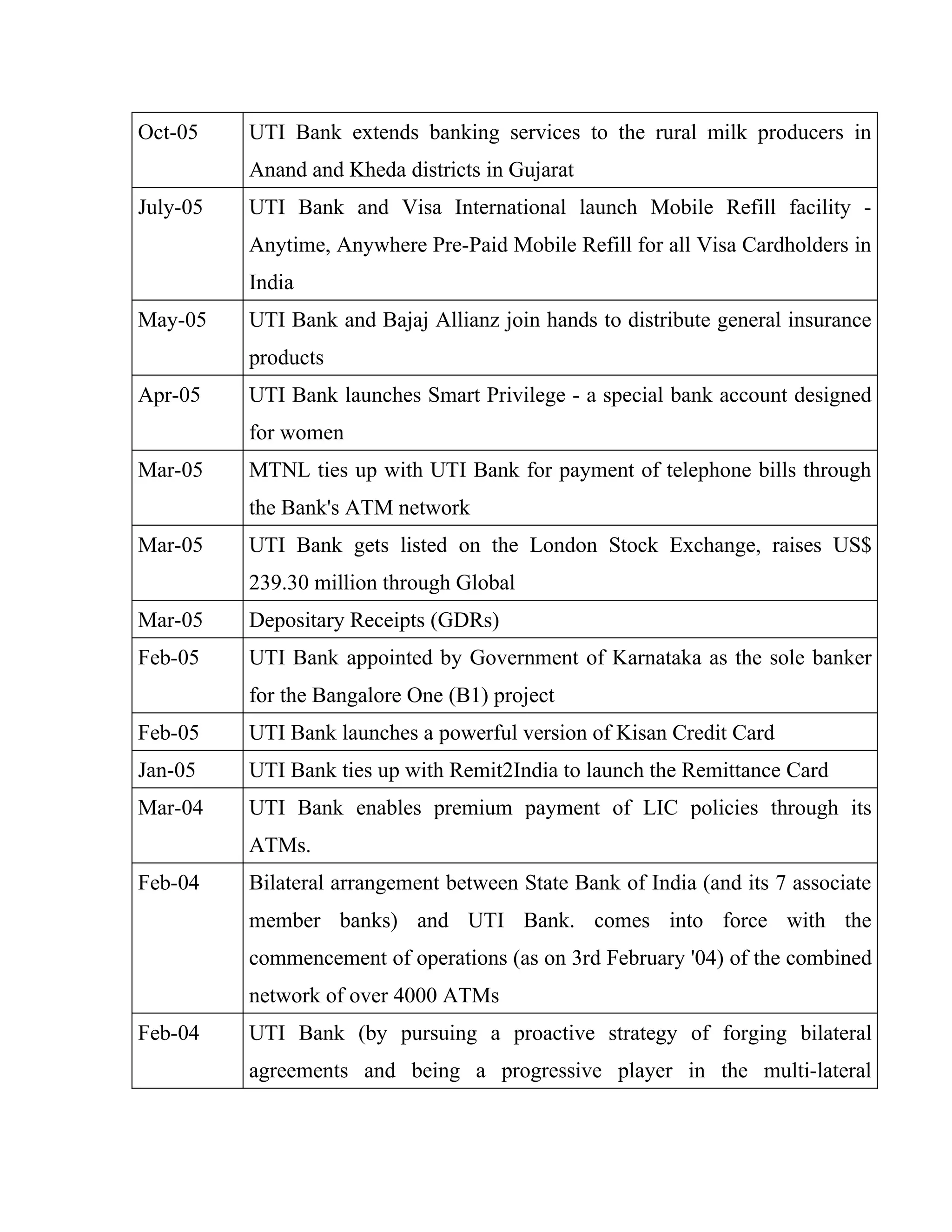

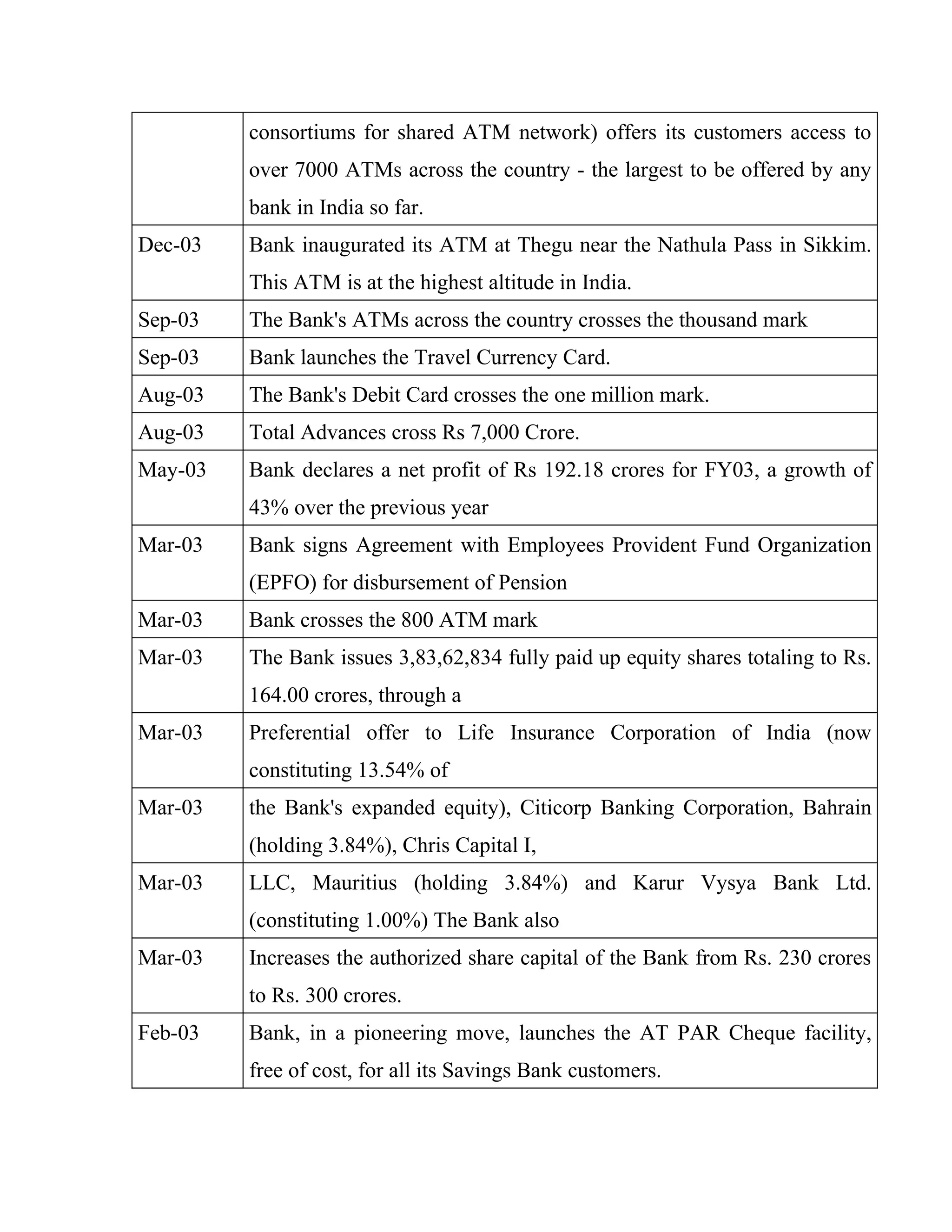

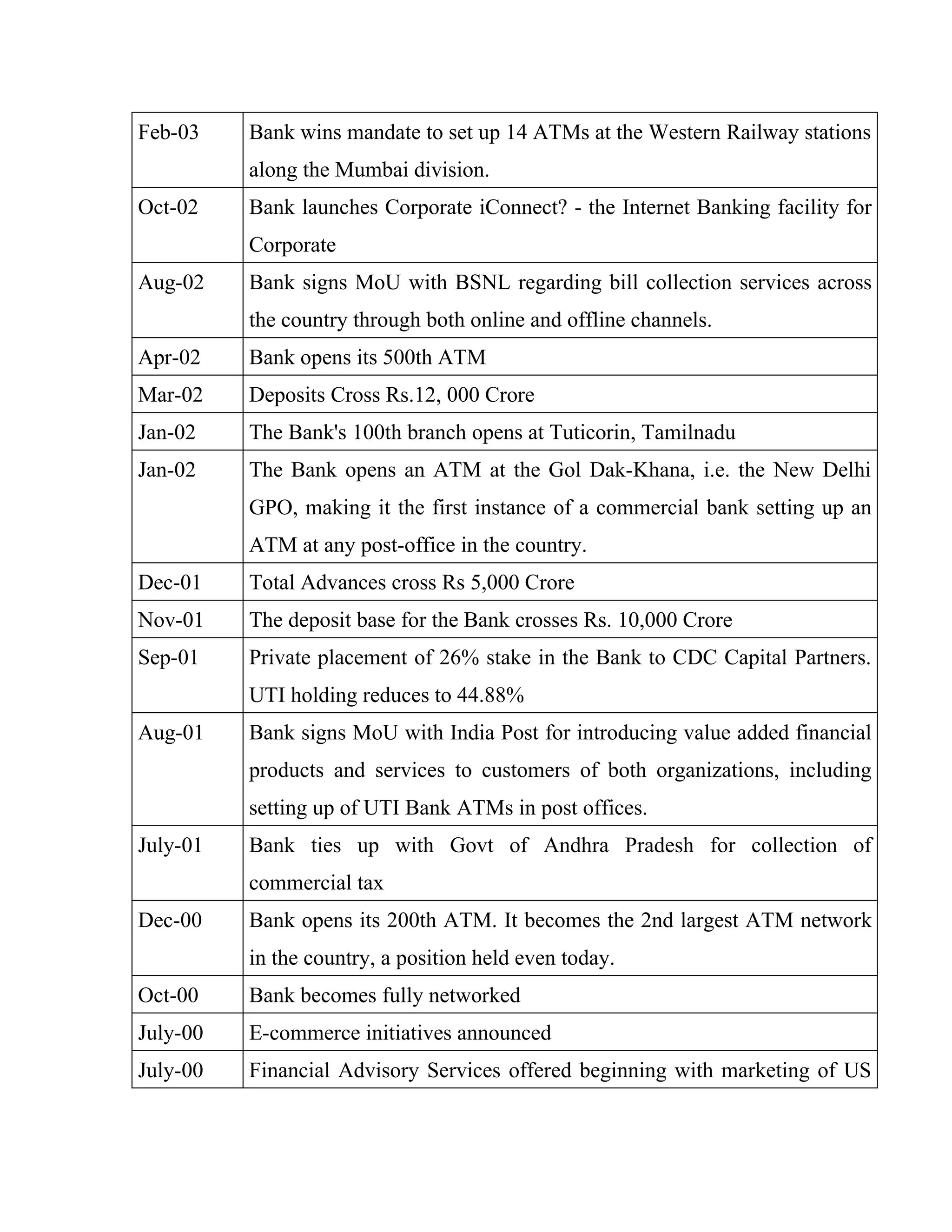

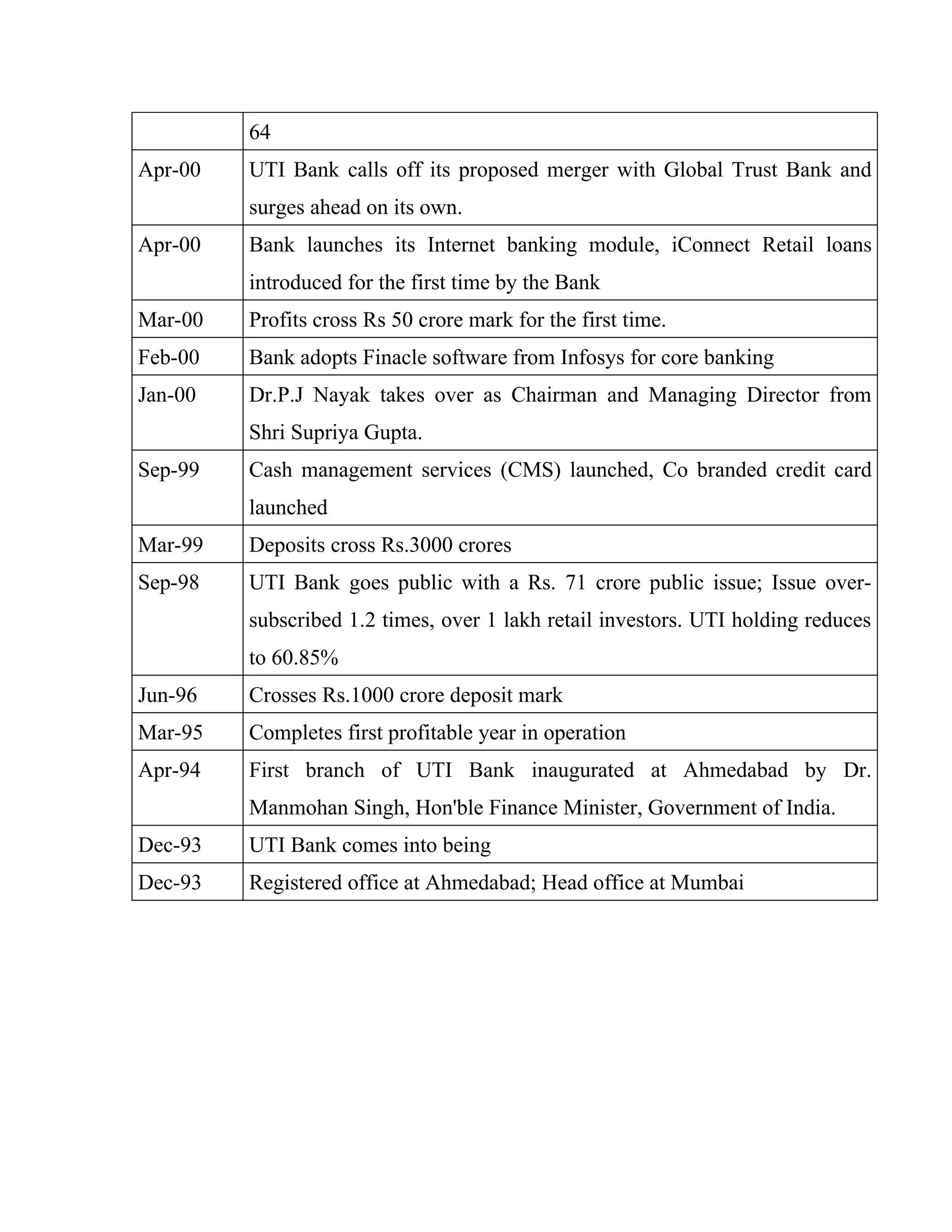

The document provides an overview of Axis Bank, formerly known as UTI Bank. It discusses the bank's history, starting operations in 1994 as a joint venture between Unit Trust of India, Life Insurance Corporation of India, and General Insurance Corporation of India. It outlines key milestones such as expanding its branch network, launching new products like credit cards and ATMs, and renaming to Axis Bank in 2007. The document also describes the bank's management and provides a high-level company profile.

![and bonds. Banks lend money by making advances to customers on current

accounts, by making installment loans, and by investing in marketable debt

securities and other forms of money lending. Banks provide almost all

payment services, and a bank account is considered indispensable by most

businesses, individuals and governments. Non-banks that provide payment

services such as remittance companies are not normally considered an

adequate substitute for having a bank account. Banks borrow most funds

from households and non-financial businesses, and lend most funds to

households and non-financial businesses, but non-bank lenders provide a

significant and in many cases adequate substitute for bank loans, and money

market funds, cash management trusts and other non-bank financial

institutions in many cases provide an adequate substitute to banks for

lending savings to

3.4 Accounting for bank accounts

Bank statements are accounting records produced by banks under the

various accounting standards of the world. Under GAAP and IFRS there are

two kinds of accounts: debit and credit. Credit accounts are Revenue, Equity

and Liabilities. Debit Accounts are Assets and Expenses. This means you

credit a credit account to increase its balance, and you debit a debit account

to increase its balance.[7]This also means you debit your savings account

every time you deposit money into it (and the account is normally in deficit),

while you credit your credit card account every time you spend money from

it (and the account is normally in credit).However, if you read your bank

statement, it will say the opposite—that you credit your account when you

deposit money, and you debit it when you withdraw funds. If you have cash

in your account, you have a positive (or credit) balance; if you are](https://image.slidesharecdn.com/naresh-axis-bank-project-100121021440-phpapp01/75/Naresh-Axis-Bank-Project-27-2048.jpg)

![Free monthly e-statement

Monthly Statement of Account delivered at your doorstep. Facility for

collecting donations in your account through our network of

Branches and extension counters across the country, as well as through

iConnect - our Internet Banking facility. Also, Axis Bank can offer the

facility to donate funds to your Trust through our Internet Banking facility

iConnect to its customers. An Axis Bank customer can donate any amount to

your Trust through the Internet. In such cases, the savings account of the

customer gets debited and the savings account of your Trust gets credited

with the amount of donation at the same time. At the end of every month,

the Bank will provide an MIS giving details of the amount of donations and

the name of donor. This will enable the Trust to issue receipts to the donors.

Free Internet Banking facility that enables you to view the status of your

account, transfer funds and carry out a number of banking activities from the

comfort of your home or office.

Investment Advice: Our Financial Advisory Desk will provide portfolio

management advice as well as help you undertake investments.

Free Demat:

To facilitate your investments, we offer a free Demat Account (charges due

to NSDL must still be levied) to our esteemed account holders in the Trust

or Society segment.

Foreign Contribution (Regulation) Act [FCRA] accounts:

The FCRA account enables approved organizations to receive foreign

contributions for utilization in their activities in India. The Bank will

provide assistance in the process of documentation and obtaining

necessary approvals from Ministry of Home Affairs at New Delhi.](https://image.slidesharecdn.com/naresh-axis-bank-project-100121021440-phpapp01/75/Naresh-Axis-Bank-Project-45-2048.jpg)