2. All slides are

taken from this

book which

includes

detailed

explanations of

all concepts.

Available from

Amazon.com

Full color version available at

www.createspace.com/4707238

17. I would like to

use $50,000

per year from

my assets.

The rest, I

want to go to

my favorite

charity.

18. I want to

control my

own

investments

and spend

about 5% of

my assets

each year.

After death I

want it all to

go to charity.

19. I want to retire today,

but my pension

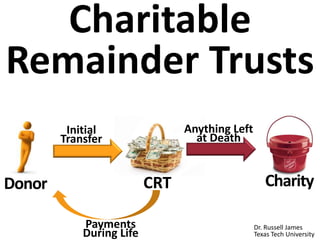

doesn’t start paying

for 9 more years. I

want to give assets

to charity, but I still

need $65,000 per

year for 9 years.

27. A client holds low-basis

appreciated assets that

generate little income (e.g.,

developable land or small

business growth stock).

How can she convert to

diversified income-

generating investments?

28. Option 1: Sell it. Pay the capital gains

tax. Invest the remaining amount.

$1,000,000 zero basis asset

$238,000 tax (23.8% federal)

$762,000 left to invest

29. Option 1: Even worse in many states

$1,000,000 zero basis asset

$339,350 tax (33.935% Calif. + Fed.)

$660,650 left to invest

30. Option 1: Or with certain assets

$1,000,000 zero-basis art

$408,706 tax (40.87% Calif. + Fed.)

$591,294 left to invest

31. Option 1: Or certain holding periods

$1,000,000 zero-basis short-

term capital gain

$509,280 tax (50.928% Cal. + Fed.)

$490,720 left to invest

Note that gifts of

short-term capital

gain are deductible

only at basis

32. Option 2: Transfer to a CRT

$1,000,000 zero-basis asset

_____$0 tax (CRT pays no tax)

$1,000,000 left to invest

33. You can produce

more income

with $1,000,000

Than with

$762,000 or

$660,650 or

$591,294 or

$490,720

34. CRT Advantages

• Immediate income tax

deduction

• No capital gains tax on

transfer to CRT

• No capital gains tax

when CRT sells

• Lifetime income

CRT Concern?

• Remainder goes to

charity not to family

How can we address

this limitation?

40. Find the §7520 rate

http://www.irs.gov/Businesses/Small-Businesses-&-Self-

Employed/Section-7520-Interest-Rates

Multiply payment by annuity

factor in IRS Pub. 1457http://www.irs.gov/Retirement-Plans/Actuarial-Tables

Value of CRAT

payments

41. Find the §7520 rate

http://www.irs.gov/Businesses/Small-Businesses-&-Self-

Employed/Section-7520-Interest-Rates

I can choose

current or

one of last

two month’s

rate

$4,000/year

CRATage55

donoron

10/31/13

Aug 2.0%

Sept 2.0%

Oct 2.4%

43. Find the §7520 rate

2.4%http://www.irs.gov/Businesses/Small-Businesses-&-Self-

Employed/Section-7520-Interest-Rates

$4,000/year

CRATage55

donoron

10/31/13

I want the

lowest

annuity

valuation

[highest

charitable

deduction]

so I select

Oct. 2.4%

44. Section 1 Table S - Based on Life Table 2000CM

Interest at 2.4 Percent

Life Life

Age Annuity Estate Remainder Age Annuity Estate Remainder

0 34.2376 0.82170 0.17830 55 18.1993 0.43678 0.56322

1 34.3011 0.82323 0.17677 56 17.7570 0.42617 0.57383

2 34.1418 0.81940 0.18060 57 17.3129 0.41551 0.58449

3 33.9727 0.81534 0.18466 58 16.8678 0.40483 0.59517

4 33.7967 0.81112 0.18888 59 16.4213 0.39411 0.60589

Find the §7520 rate

2.4%www.irs.gov/Businesses/Small-Businesses-&-Self-Employed/Section-

7520-Interest-Rates

Multiply annual payment by

annuity factor in IRS Pub. 1457

$4,000 X 18.1993www.irs.gov/Retirement-Plans/Actuarial-Tables

$4,000/yearCRAT

age55donoron

10/31/13

45. Find the §7520 rate

2.4%www.irs.gov/Businesses/Small-Businesses-&-Self-Employed/Section-

7520-Interest-Rates

Multiply annual payment by

annuity factor in IRS Pub. 1457

$4,000 X 18.1993www.irs.gov/Retirement-Plans/Actuarial-Tables

Value of annuity

$72,797

If annuity

pays more

than

annually, add

adjustment

factor from

Table K

$4,000/yearCRAT

age55donoron

10/31/13

51. Rule: 10% of

present value

minimum to

charity

Reality: Share

of CRT assets

to charity,

1.59%

Split interests trusts, filing year 2007,

Lisa Schreiber, IRS Statistics of Income

The IRS tax deduction is actuarially too

large because CRT donors live longer

Annuity purchasers

live longer (i.e., sick

people don’t buy

lifetime annuities)

Wealthy people live

longer (CRT donors

are very wealthy)

Charitable bequest

donors live longerSee: James, R.N., (2013) American Charitable

bequest demographics.

52. STEP 1: Using §7520 rate, at what

age will the CRAT exhaust?

Using a financial calculator solve for n (number of time periods) after entering present value

(initial CRAT assets), rate (§7520 rate), payments, and setting future value to 0. The

underlying formula is

STEP 2. Is there >5% chance the

donor will live that long?

(lx@age-of-exhaustion / lx@current-age, using Table 2000CM at

www.irs.gov/Retirement-Plans/Actuarial-Tables )

CRAT disqualified if >5% chance of

exhaustion due to annuitant longevity

56. When the trust makes a

payment, it opens the

spigot.

Ordinary income is paid

first, then capital gain and

so forth.

Return of

Principal

Exempt

Income

Capital

Gain

Ordinary

Income

57. Donor gives $100,000 of stock

($10,000 basis) to CRT. The CRT

sells the stock, buys corporate

bonds generating $3,000 of

income and municipal bonds

generating $2,000 of tax

exempt income.

Return of

Principal

Exempt

Income

Capital

Gain

Ordinary

Income

58. Donor gives $100,000 of stock

($10,000 basis) to CRT. The CRT

sells the stock, buys corporate

bonds generating $3,000 of

income and municipal bonds

generating $2,000 of tax

exempt income.

$10,000

$2,000

$90,000

$3,000

Return of

Principal

Exempt

Income

Capital

Gain

Ordinary

Income

59. What is the tax treatment of a

$2,000 distribution?

$10,000

$2,000

$90,000

$3,000

Return of

Principal

Exempt

Income

Capital

Gain

Ordinary

Income

60. What is the tax treatment of a

$2,000 distribution?

Recipient pays taxes on:

$2,000 of ordinary income

$10,000

$2,000

$90,000

$3,000

Return of

Principal

Exempt

Income

Capital

Gain

Ordinary

Income

61. What is the tax treatment of a

$5,000 distribution?

$10,000

$2,000

$90,000

$3,000

Return of

Principal

Exempt

Income

Capital

Gain

Ordinary

Income

62. What is the tax treatment of a

$5,000 distribution?

Recipient pays taxes on:

$3,000 of ordinary income

$2,000 of capital gain

$10,000

$2,000

$90,000

$3,000

Return of

Principal

Exempt

Income

Capital

Gain

Ordinary

Income

63. What is the tax treatment of a

$10,000 distribution?

$10,000

$2,000

$90,000

$3,000

Return of

Principal

Exempt

Income

Capital

Gain

Ordinary

Income

64. What is the tax treatment of a

$10,000 distribution?

Recipient pays taxes on:

$3,000 of ordinary income

$7,000 of capital gain

$10,000

$2,000

$90,000

$3,000

Return of

Principal

Exempt

Income

Capital

Gain

Ordinary

Income

65. If CRT ordinary income

earnings are always higher

than distributions, no capital

gain tax will ever be paid.

Return of

Principal

Exempt

Income

Capital

Gain

Ordinary

Income

69. Suppose you want

the trust to hold a

non-income

producing asset

A normal payout

requirement could

force a sale

land, art, non-dividend or closely-held stock

72. NIMCRUTs may be

problematic when

later returns are

consistently less than

payout rates.

There isn’t enough

income to make

normal payouts or

make-up past

deficiencies.

73. “Flip CRUT”: A NICRUT/NIMCRUT that

converts to a CRUT at a trigger event

NICRUT/

NIMCRUT

Standard

CRUT

Trigger

Event

75. 2015 2016 2017 2018 2019 … Death

Initial

Transfer

Anything

Remaining

at Death

2014

TriggerEvent

Incomeupto

5%

Incomeupto

5%

Incomeupto

5%

5%

5%

76. 2015 2016 2017 2018 2019 … Death

Initial

Transfer

Anything

Remaining

at Death

2014

TriggerEvent

$0.00

Ex: Trigger is sale

of $1,000,000 of

non-income

producing land

funding CRT

$0.00

$0.00

$50,000

$51,000

77. CRT “spigot” trusts

Trustees flip income off

and on at will by

investment choice

• Commercial deferred annuities*

• Limited partnership interests

• Non-dividend paying growth

stocks

• Delay realizing gains (post-

transfer capital gain can count

as income)

*Limits on this activity currently “under review” by IRS

78. Conrad Teitell suggests

triggering a FLIP-CRUT using

a small, but hard-to-market,

asset such as one share of

closely-held stock

Then trustee sells

whenever the flip is desired

Flip

when

sold

79. A donor can give part of an

undivided interest (e.g., 75%

as tenants in common) to a

CRT.

Subsequent sale generates

capital gain for the retained

share, but the contribution

generates a tax deduction.

80. Charitable

Remainder Trust

Flexible & Expensive

• CRTs are individually

created according to the

specific desires of each

client

Charitable

Gift Annuity

Simple & Cheap

• CGAs from a charity are

usually identical except for

the dollar amount

81. The flexibility of

CRTs

• Unlimited number of

public charity or private

foundation beneficiaries

(income limitations pass

through)

• Open choice on payout

years and amounts

• Unlimited number of

income beneficiaries

• Special restrictions on

income beneficiaries

allowed (where

violation gives income

to alternate beneficiary)

– Spendthrift trusts

– Match earned income to

prevent “trust fund” kids

– Require random drug

tests

82. “Notwithstanding any provision of this Will to the

contrary, my grandchildren DAVID PANZIRER and WALTER

PANZIRER shall not be entitled to any distributions from

any trust established for such beneficiary's benefit under

this Will unless such beneficiary visits the grave of my late

son JAY PANZIRER, at least once each calendar year,

preferably on the anniversary of my said son's death

(March 31, 1982) (except that this provision shall not

apply during any period that the beneficiary is unable to

comply therewith by reason of physical or mental

disability as determined by my Trustees in their sole and

absolute discretion).”

Leona Helmsley’s Charitable

Remainder Unitrust created

in her will includes

85. 100% excise tax on Unrelated Business

Taxable Income (UBTI), where CRT is

running a business (e.g., owning as a sole

proprietor or partner) instead of being a

passive investor

86. Not UBTI

Dividends, interest,

annuities, royalties, rents

from real estate, and

capital gains, so long as

none of them involve

debt-financing

UBTI

Net income from running

a hotel, parking lot,

convenience store, coin

operated laundry

or

Debt financed net income

87. Ex: CRT receives a

$1,000,000 home

($100,000 basis).

Trustee makes

improvements

using a $100,000

mortgage

(acquisition

indebtedness) and

sells for $1,200,000.

Result?

88. Ex: CRT receives a

$1,000,000 home

($100,000 basis).

Trustee makes

improvements

using a $100,000

mortgage

(acquisition

indebtedness) and

sells for $1,200,000.

Due to debt

financing

$1,000,000 capital

gain is UBTI, taxed

at 100%, and lost.

89. Self-Dealing

CRT can’t sell,

lease, loan, or

allow use of assets

by CRT creator,

contributor,

trustee, or their

ancestors,

descendents, or

spouses

91. If all parties

agree can a

CRT be broken

and

distributed?

IRS has

allowed

termination &

distribution of

present value

of all interests

PLR 200208039

92. Donor plans to create

CRT with remainder

value sufficient to

build a building, but

charity needs building

now. Solutions?

93. Donor plans to create

CRT with remainder

value sufficient to

build a building, but

charity needs building

now. Solutions?

CRT may segregate

and pledge funds as

collateral for a loan

taken out by the

charity. (Charity can

pay off loan with

remainder at death.)

PLR 8807082

95. Help me

HERE

convince my bosses that continuing to build and

post these slide sets is not a waste of time. If

you work for a nonprofit or advise donors and

you reviewed these slides, please let me know

by clicking

96. If you clicked on

the link to let

me know you

reviewed these

slides…

Thank

You!

97. This slide set is from the curriculum for

the Graduate Certificate in Charitable

Financial Planning at Texas Tech

University, home to the nation’s largest

graduate program in personal financial

planning.

To find out more about the online

Graduate Certificate in Charitable

Financial Planning go to

www.EncourageGenerosity.com

To find out more about the M.S. or

Ph.D. in personal financial planning at

Texas Tech University, go to

www.depts.ttu.edu/pfp/

Graduate Studies in

Charitable Financial Planning

at Texas Tech University

Editor's Notes

Creative commons picture from http://commons.wikimedia.org/wiki/File:Leona_Helmsley.jpg