Recommended

More Related Content

What's hot

Viewers also liked

Viewers also liked (15)

Similar to Effective ifrs 2012

Similar to Effective ifrs 2012 (20)

Recently uploaded

Recently uploaded (20)

Effective ifrs 2012

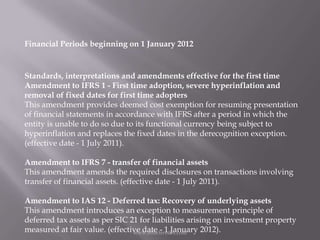

- 1. Financial Periods beginning on 1 January 2012 Standards, interpretations and amendments effective for the first time Amendment to IFRS 1 - First time adoption, severe hyperinflation and removal of fixed dates for first time adopters This amendment provides deemed cost exemption for resuming presentation of financial statements in accordance with IFRS after a period in which the entity is unable to do so due to its functional currency being subject to hyperinflation and replaces the fixed dates in the derecognition exception. (effective date - 1 July 2011). Amendment to IFRS 7 - transfer of financial assets This amendment amends the required disclosures on transactions involving transfer of financial assets. (effective date - 1 July 2011). Amendment to IAS 12 - Deferred tax: Recovery of underlying assets This amendment introduces an exception to measurement principle of deferred tax assets as per SIC 21 for liabilities arising on investment property measured at fair value. (effective date - 1 January 2012).www.effectiveifrs.com

- 2. Amendment to IAS 1 - Financial statement presentation of other comprehensive income This amendment requires entities to group other comprehensive income items into two groupings based on whether they might be reclassified to profit or loss subsequently or not. (effective date - 1 July 2012). Amendment to IAS 19 - Employee benefits This amendment eliminates the corridor approach and calculates finance costs on a net funding basis (effective date - 1 January 2013). Amendment to IAS 27 - Separate financial statements This amendment excludes the requirements relating to consolidated financial statements, which are now included in IFRS 10 while retaining the requirements relating to separate financial statements (effective date - 1 January 2013). Amendment to IAS 28 - Associates and joint ventures This amendment includes the requirements for associates and joint ventures that have to be equity accounted following the issue of IFRS 11 (effective date - 1 January 2013). www.effectiveifrs.com

- 3. IFRIC 20 - Stripping costs in the production phase of a surface mine This interpretation sets out the accounting for stripping costs in the production phase of a surface mine. The interpretation may require mining entities to write off existing stripping assets to opening retained earnings if the assets cannot be attributed to an identifiable component of an ore body (effective date - 1 January 2013). Amendment to IFRS 1 - First time adoption, Government loans This amendment allows the prospective application of the measurement requirements of government loans with a below market rate of interest, while retaining the election to apply retrospectively (effective date - 1 January 2013). IFRS 10 - Consolidated financial statements This standard addresses consolidated financial statements, previously under IAS 27, the requirements for special purpose entities previously under SIC 12 and sets out Control as the basis for consolidation revises its definition and provides application guidance for its application. (effective date - 1 January 2013). Amendments to IFRS 10, IFRS 11 and IFRS 12 - Transition guidance These amendments provide additional transition relief to IFRSs 10, 11 and 12, limiting the requirement to provide adjusted comparative information to only the preceding comparative period. For disclosures related to unconsolidated structured entities, the amendments will remove the requirement to present comparative information for periods before IFRS 12 is first applied. (effective date - 1 January 2013). www.effectiveifrs.com

- 4. IFRS 11 - Joint arrangements IFRS 11 supersedes IAS 31, it introduces a specific set of test for the classification of joint arrangements as either joint operation or joint venture. Joint ventures are to be accounted for using the equity method and joint operations by the share of assets, liabilities, revenue and expenses. (effective date - 1 January 2013). IFRS 12 - Disclosures of interests in other entities IFRS 12 sets out the disclosure requirements for subsidiaries, associates, joint arrangements and uncontrolled structured entities. (effective date - 1 January 2013). IFRS 13 - Fair value measurement IFRS 13 provides a precise definition of fair value and a sets out the measurement framework and disclosure requirements to be used across IFRS. (effective date - 1 January 2013). Amendment to IFRS 7 - asset and liability offsetting This amendment includes new disclosures requirements for financial assets and liabilities that are offset or subject to master netting arrangements or similar arrangement (effective date - 1 January 2013). www.effectiveifrs.com

- 5. Annual improvements to IFRS - 2009-2011 cycle Annual improvements to IFRS 2009-2011 reporting cycle, includes changes to the following: IFRS 1, First time adoption IAS 1, Financial statement presentation IAS 16, Property plant and equipment IAS 32, Financial instruments; Presentation IAS 34, Interim financial reporting (effective date - 1 January 2013). Amendment to IAS 32 - Asset and liability offsetting This amendment clarifies the offsetting criteria of IAS 32 and the meaning of currently has a legally enforceable right to set-off (effective date - 1 January 2014). Amendments to IFRS 10, IFRS 12 and IAS 27 - Investment Entities These amendments provide a consolidation of subsidiaries exemption to entities which meet the definition of an Investment Entity, allowing these entities to measure their investment in subsidiaries at fair value through profit or loss (effective date - 1 January 2014). IFRIC 21 - Levies This interpretation clarifies the IAS 37 criteria for the recognition of a liability in relation to government imposed levies. (effective date - 1 January 2014). www.effectiveifrs.com

- 6. Amendment to IAS 36 - Recoverable Amount Disclosures for Non-Financial Assets This amendment clarifies that the disclosures in relation to the recoverable amount of impaired assets is limited to the recoverable amount of impaired assets that is based on fair value less costs of disposal. (effective date - 1 January 2014). IFRS 9 - Financial instruments IFRS 9 replaces the classification and measurement framework in IAS 39 with a two classification model based on the entitys business model and the contractual cash flow characteristics of the financial asset, financial assets measured at amortized cost and financial assets measured at fair value (effective date - 1 January 2015). www.effectiveifrs.com