How the 1-2-3 Account benefits Mortgage Holders but not Students

•

0 likes•862 views

The document discusses the 1-2-3 Account program, which provides cash back and is intended for mortgage holders and families with balances over $3,000. Younger people were dissatisfied because the program was not intended for them, while qualified mortgage holders expressed delight with the benefits. It recommends that consumers evaluate their personal finances to determine if the 1-2-3 Account is suitable for them and discusses marketing the program through various online and offline channels to those who would benefit most.

Recommended

Recommended

More Related Content

Similar to How the 1-2-3 Account benefits Mortgage Holders but not Students

Similar to How the 1-2-3 Account benefits Mortgage Holders but not Students (20)

More from Steven Bayley

More from Steven Bayley (13)

Recently uploaded

Recently uploaded (20)

How the 1-2-3 Account benefits Mortgage Holders but not Students

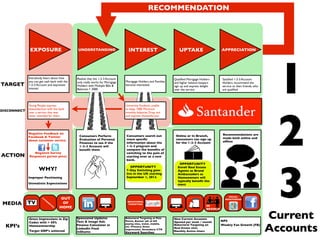

- 1. Realize that the 1-2-3 Account only really works for Mortgage Holders with Multiple Bills & Balances > 3000 Everybody hears about how you can get cash back with the 1-2-3 Account and expresses interest Mortgage Holders and Families become interested. Young People express dissatisfaction with the bank over a service that was never intended for them Negative Feedback on Facebook & Twitter about customer service Improper Positioning Unrealistic Expectations Negative Survey Responses garner press WHY? EXPOSURE UNDERSTANDING INTEREST UPTAKE APPRECIATION RECOMMENDATION Consumers Perform Evaluation of Personal Finances to see if the 1-2-3 Account will benefit them Qualified Mortgage Holders and higher balance keepers sign up and express delight over the service MEDIA KPI’s ACTION TARGET DISCONNECT T EX P ER IEN T IA L OUT OF HOME 8/12/13 9:21 PM BEHAVIORAL TARGETING Consumers search out more specific information about the 1-2-3 program and compare the benefits of switching to the pain of starting over at a new bank. OPPORTUNITY 7-Day Switching goes live in the UK starting September 1, 2013. Satisfied 1-2-3 Account Holders recommend the service to their friends, who are qualified Gross Impressions in Zip Codes with > 50% Homeownership Target GRP’s achieved New Current Accounts Opened per week / month NPS University Students unable to keep 1000 Minimum monthly balances Drop out and express dissatisfaction 1 2 3Current Accounts 8/12/13 11:39 PM 8/12/13 18/12/13 8:46 PM8/12/13 8:46 PM8/12/13 11:51 PM TV IN BRANCH Keyword Searches Behavioral Targeting at Pain Points, Banner ads at bill paying sites, water, mobile, etc. Primary: Gross Impressions, Secondary: CTR InShares Weekly Fan Growth (FB) Monthly Active Users Sponsored Updates Text & Image Ads Finance Calculator in LinkedIn Feed SOCIAL MONITORING Recommendations are made both online and offline Behavioral Targeting on Real Estate sites Online or In Branch, consumers can sign up for the 1-2-3 Account 8/13/13 10:52 AM OPPORTUNITY Enroll Real Estate Agents as Brand Ambassadors as Homeowners will typically benefit the most