QNBFS Daily Market Report May 01, 2016

•

0 likes•324 views

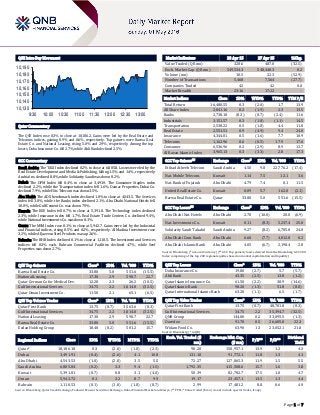

The QSE Index rose 0.3% to close at 10,186.2

Recommended

Recommended

More Related Content

Viewers also liked

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

QNBFS Daily Market Report May 01, 2016

- 1. Page 1 of 7 QSE Intra-Day Movement Qatar Commentary The QSE Index rose 0.3% to close at 10,186.2. Gains were led by the Real Estate and Telecoms indices, gaining 0.9% and 0.6%, respectively. Top gainers were Barwa Real Estate Co. and National Leasing, rising 5.0% and 2.9%, respectively. Among the top losers, Doha Insurance Co. fell 2.7%, while Ahli Bank declined 2.5%. GCC Commentary Saudi Arabia: The TASI Index declined 0.2% to close at 6,805.8. Losses were led by the Real Estate Development and Media & Publishing, falling 1.5% and 1.4%, respectively. Arabia Ins. declined 8.8%, while Solidarity Saudi was down 8.2%. Dubai: The DFM Index fell 0.4% to close at 3,491.9. The Consumer Staples index declined 2.2%, while the Transportation index fell 1.6%. Damac Properties Dubai Co. declined 7.9%, while Hits Telecom was down 3.5%. Abu Dhabi: The ADX benchmark index declined 1.0% to close at 4,543.5. The Services index fell 3.8%, while the Banks index declined 2.1%. Abu Dhabi National Hotels fell 10.0%, while Gulf Cement Co. was down 7.9%. Kuwait: The KSE Index fell 0.7% to close at 5,391.8. The Technology index declined 2.3%, while Insurance index fell 1.7%. Real Estate Trade Centers Co. declined 9.4%, while National Investments Co. was down 8.3%. Oman: The MSM Index rose 0.1% to close at 5,942.7. Gains were led by the Industrial and Financial indices, rising 0.5% and 0.2%, respectively. Al Madina Investment rose 3.2%, while Al Jazeera Steel Products was up 2.6%. Bahrain: The BHB Index declined 0.1% to close at 1,110.5. The Investment and Services indices fell 0.3% each. Bahrain Commercial Facilities declined 4.7%, while Seef Properties was down 2.7%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Barwa Real Estate Co. 33.80 5.0 551.6 (15.5) National Leasing 17.30 2.9 590.7 22.7 Qatar German Co for Medical Dev. 12.28 2.3 26.2 (10.5) Gulf International Services 34.75 2.2 1,014.0 (32.5) Qatar Oman Investment Co. 11.50 2.1 65.1 (6.5) QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Qatar First Bank 13.75 (0.7) 3,563.6 (8.3) Gulf International Services 34.75 2.2 1,014.0 (32.5) National Leasing 17.30 2.9 590.7 22.7 Barwa Real Estate Co. 33.80 5.0 551.6 (15.5) Ezdan Holding Group 18.40 (0.2) 501.2 15.7 Market Indicators 28 Apr 15 27 Apr 15 %Chg. Value Traded (QR mn) 328.6 487.0 (32.5) Exch. Market Cap. (QR mn) 549,534.3 548,440.3 0.2 Volume (mn) 10.5 22.3 (52.9) Number of Transactions 5,468 7,564 (27.7) Companies Traded 42 42 0.0 Market Breadth 23:16 17:22 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 16,480.55 0.3 (2.0) 1.7 13.9 All Share Index 2,841.16 0.2 (1.9) 2.3 13.5 Banks 2,738.18 (0.3) (0.7) (2.4) 11.6 Industrials 3,151.57 0.3 (1.8) (1.1) 14.5 Transportation 2,538.22 0.5 (1.8) 4.4 11.8 Real Estate 2,551.51 0.9 (4.9) 9.4 24.0 Insurance 4,344.01 0.5 (1.6) 7.7 10.9 Telecoms 1,162.96 0.6 (0.5) 17.9 17.6 Consumer 6,536.96 0.2 (2.9) 8.9 13.7 Al Rayan Islamic Index 3,965.13 0.3 (3.3) 2.8 17.3 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Etihad Atheeb Telecom Saudi Arabia 4.50 9.8 22,776.2 (17.4) Nat. Mobile Telecom. Kuwait 1.14 7.5 12.1 3.6 Nat. Bank of Fujairah Abu Dhabi 4.79 7.4 0.1 11.5 United Real Estate Co. Kuwait 0.09 5.7 162.0 (2.1) Barwa Real Estate Co. Qatar 33.80 5.0 551.6 (15.5) GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Abu Dhabi Nat. Hotels Abu Dhabi 2.70 (10.0) 20.0 (6.9) Nat. Investments Co. Kuwait 0.11 (8.3) 5,237.4 25.0 Solidarity Saudi Takaful Saudi Arabia 9.27 (8.2) 6,785.0 24.8 Abu Dhabi Com. Bank Abu Dhabi 6.60 (7.7) 4,812.8 0.2 Abu Dhabi Islamic Bank Abu Dhabi 4.05 (6.7) 2,198.4 2.8 Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Doha Insurance Co. 19.80 (2.7) 5.7 (5.7) Ahli Bank 43.35 (2.5) 13.8 (1.2) Qatar Islamic Insurance Co. 61.50 (2.2) 30.9 (14.6) Qatar Islamic Bank 98.20 (1.3) 51.8 (8.0) Qatar International Islamic Bank 63.20 (1.1) 6.5 (1.7) QSE Top Value Trades Close* 1D% Val. ‘000 YTD% Qatar First Bank 13.75 (0.7) 48,701.8 (8.3) Gulf International Services 34.75 2.2 35,394.7 (32.5) QNB Group 144.00 0.2 33,095.5 (1.3) Ooredoo 91.70 0.5 26,605.0 22.3 Widam Food Co. 63.90 1.3 23,052.1 21.0 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 10,186.18 0.3 (2.0) (1.8) (2.3) 90.28 150,957.1 13.9 1.2 4.3 Dubai 3,491.91 (0.4) (2.6) 4.1 10.8 131.18 91,772.1 11.8 1.3 4.1 Abu Dhabi 4,543.53 (1.0) (2.0) 3.5 5.5 72.27 127,865.3 11.9 1.5 5.5 Saudi Arabia 6,805.84 (0.2) 3.3 9.4 (1.5) 1,792.35 415,508.6 15.7 1.6 3.8 Kuwait 5,391.81 (0.7) 0.8 3.1 (4.0) 50.39 82,782.7 17.5 1.0 4.7 Oman 5,942.72 0.1 2.2 8.7 9.9 19.17 23,457.1 13.5 1.3 4.4 Bahrain 1,110.53 (0.1) (1.0) (1.8) (8.7) 2.99 17,481.2 8.8 0.6 4.9 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 10,130 10,140 10,150 10,160 10,170 10,180 10,190 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 7 Qatar Market Commentary The QSE Index rose 0.3% to close at 10,186.2. The Real Estate and Telecoms indices led the gains. The index rose on the back of buying support from non-Qatari shareholders despite selling pressure from Qatari and GCC shareholders. Barwa Real Estate Co. and National Leasing were the top gainers, rising 5.0% and 2.9%, respectively. Among the top losers, Doha Insurance Co. fell 2.7%, while Ahli Bank declined 2.5%. Volume of shares traded on Thursday fell by 52.9% to 10.5mn from 22.3mn on Wednesday. However, as compared to the 30-day moving average of 10.0mn, volume for the day was 5.3% higher. Qatar First Bank and Gulf International Services were the most active stocks, contributing 34.0% and 9.7% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Earnings Releases and Global Economic Data Earnings Releases Company Market Currency Revenue (mn) 1Q2016 % Change YoY Operating Profit (mn) 1Q2016 % Change YoY Net Profit (mn) 1Q2016 % Change YoY Jabal Omar Development Co. Saudi Arabia SR – – 17.4 -87.7% -44.0 NA Dubai Investments Dubai AED 714.7 31.6% – – 297.5 5.4% Deyaar Development Dubai AED 60.2 66.4% – – 51.0 -12.5% United Foods Co. Dubai AED 99.9 0.6% – – 6.6 2.7% National Central Cooling Co. Dubai AED 255.5 6.7% – – 63.4 3.6% Ras Al Khaimah Poultry & Feeding Co. Abu Dhabi AED 10.0 -38.7% – – 3.8 -15.3% Source: Company data, DFM, ADX, MSM Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 04/29 US Bureau of Economic Analysis Personal Income March 0.40% 0.30% 0.10% 04/29 US Bureau of Economic Analysis Personal Spending March 0.10% 0.20% 0.20% 04/29 US Bureau of Economic Analysis Real Personal Spending March 0.00% 0.10% 0.30% 04/29 US Bureau of Economic Analysis PCE Deflator MoM March 0.10% 0.10% -0.10% 04/29 US Bureau of Economic Analysis PCE Deflator YoY March 0.80% 0.80% 1.00% 04/29 US Bureau of Economic Analysis PCE Core MoM March 0.10% 0.10% 0.20% 04/29 US Bureau of Economic Analysis PCE Core YoY March 1.60% 1.60% 1.70% 04/29 US Bureau of Labor Statistics Employment Cost Index 1Q2015 0.60% 0.60% 0.50% 04/28 US Bloomberg Bloomberg Consumer Comfort 24-April 43.4 – 42.9 04/28 US Department of Labor Initial Jobless Claims 23-April 257k 259k 248k 04/28 US Department of Labor Continuing Claims 16-April 2,130k 2,136k 2,135k 04/28 US Bureau of Economic Analysis GDP Annualized QoQ 1Q2015 0.50% 0.70% 1.40% 04/28 US Bureau of Economic Analysis Personal Consumption 1Q2015 1.90% 1.70% 2.40% 04/28 US Bureau of Economic Analysis GDP Price Index 1Q2015 0.70% 0.50% 0.90% 04/28 US Bureau of Economic Analysis Core PCE QoQ 1Q2015 2.10% 1.90% 1.30% 04/28 EU European Commission Economic Confidence April 103.9 103.4 103.0 04/28 EU European Commission Business Climate Indicator April 0.1 0.1 0.1 04/28 EU European Commission Industrial Confidence April -3.7 -4.0 -4.2 04/28 EU European Commission Services Confidence April 11.5 10.0 9.6 04/29 EU Eurostat Unemployment Rate March 10.20% 10.30% 10.40% 04/29 EU Eurostat CPI Estimate YoY April -0.20% -0.10% 0.00% 04/29 EU Eurostat CPI Core YoY April 0.70% 0.90% 1.00% 04/29 EU Eurostat GDP SA QoQ 1Q2015 0.60% 0.40% 0.30% 04/29 EU Eurostat GDP SA YoY 1Q2015 1.60% 1.40% 1.60% 04/29 France INSEE GDP QoQ 1Q2015 0.50% 0.40% 0.30% 04/29 France INSEE GDP YoY 1Q2015 1.30% 1.00% 1.40% 04/29 France INSEE PPI MoM March 0.30% – -0.50% 04/29 France INSEE PPI YoY March -4.00% – -4.20% Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 32.60% 38.24% (18,520,102.12) Qatari Institutions 19.29% 18.29% 3,294,059.32 Qatari 51.89% 56.53% (15,226,042.80) GCC Individuals 0.82% 4.25% (11,266,915.18) GCC Institutions 5.79% 7.14% (4,444,667.60) GCC 6.61% 11.39% (15,711,582.78) Non-Qatari Individuals 12.57% 12.40% 557,083.53 Non-Qatari Institutions 28.92% 19.68% 30,380,542.05 Non-Qatari 41.49% 32.08% 30,937,625.58

- 3. Page 3 of 7 04/29 France INSEE CPI EU Harmonized MoM April 0.10% 0.10% 0.80% 04/29 France INSEE CPI EU Harmonized YoY April -0.10% -0.10% -0.10% 04/29 France INSEE CPI MoM April 0.10% 0.10% 0.70% 04/29 France INSEE CPI YoY April -0.20% -0.10% -0.10% 04/29 France INSEE Consumer Spending MoM March 0.20% -0.40% 0.50% 04/29 France INSEE Consumer Spending YoY March 2.70% 2.10% 1.60% 04/29 Germany Destatis Retail Sales MoM March -1.10% 0.40% 0.00% 04/29 Germany Destatis Retail Sales YoY March 0.70% 2.70% 5.50% 04/28 Germany Destatis CPI MoM April -0.40% -0.20% 0.80% 04/28 Germany Destatis CPI YoY April -0.10% 0.10% 0.30% 04/28 Germany Destatis CPI EU Harmonized MoM April -0.50% -0.20% 0.80% 04/28 Germany Destatis CPI EU Harmonized YoY April -0.30% 0.00% 0.10% 04/28 Germany Deutsche Bundesbank Unemployment Change (000's) April -16k 0k -2k 04/28 Germany Deutsche Bundesbank Unemployment Claims Rate SA April 6.20% 6.20% 6.20% 04/29 UK Bank of England Mortgage Approvals March 71.4k 74.2k 73.2k 04/29 UK Bank of England Money Supply M4 MoM March -0.40% – 0.90% 04/29 UK Bank of England M4 Money Supply YoY March 1.60% – 2.20% 04/29 UK Bank of England M4 Ex IOFCs 3M Annualised March 6.50% 6.00% 5.60% 04/29 UK Bank of England Net Consumer Credit March 1.9bn 1.3bn 1.4bn 04/29 UK GfK NOP (UK) GfK Consumer Confidence April -3.0 -1.0 0.0 04/28 UK Nationwide Building Society Nationwide House PX MoM April 0.20% 0.40% 0.70% 04/28 UK Nationwide Building Society Nationwide House Px NSA YoY April 4.90% 5.00% 5.70% 04/28 Spain INE Unemployment Rate 1Q2015 21.00% 20.90% 20.90% 04/28 Spain INE CPI EU Harmonised MoM April 0.40% 0.80% 2.00% 04/28 Spain INE CPI EU Harmonised YoY April -1.20% -0.90% -1.00% 04/28 Spain INE CPI MoM April 0.70% 1.10% 0.60% 04/28 Spain INE CPI YoY April -1.10% -0.70% -0.80% 04/29 Spain INE GDP QoQ 1Q2015 0.80% 0.70% 0.80% 04/29 Spain INE GDP YoY 1Q2015 3.40% 3.30% 3.50% 04/29 Spain Bank of Spain Current Account Balance February -1.5bn – -0.7bn 04/29 Italy ISTAT PPI MoM March 0.20% – -0.50% 04/29 Italy ISTAT PPI YoY March -3.90% – -4.10% 04/29 Italy ISTAT Unemployment Rate March 11.40% 11.60% 11.60% Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) News Qatar ERES net profit surges 33.2% QoQ in 1Q2016 – Ezdan Holding Group’s (ERES) net profit jumped 33.2% QoQ and 12.1% YoY to QR585.7mn in 1Q2016, on the back of ongoing expansion of projects and comprehensive development plans on facilities and assets. It should be noted that the primary QOQ jump in the bottom-line was led by dividend income (which is generally absent in the fourth quarter). Earnings per share (EPS) increased to QR0.22 in the 1Q2016 compared to QR0.20 in 1Q2015. The company’s rental income slipped 5.3% QoQ (+8.7% YoY) to QR394.4mn in 1Q2016. To expand the funding sources for its plans to enter the international markets, the group has started proceedings to issue $2bn Sukuk, in addition to “ambitious plans” to launch real estate, hospitality, and shopping malls projects in 2016. ERES CEO Ali Mohamed al-Obaidli said the company is studying opportunities for its overseas expansion after acquiring leading position locally and regionally, in addition to several awards it received for investment excellence. (QSE, QNBFS Research, Gulf-Times.com) MPHC bottom-line declines 29% QoQ in 1Q2016 – Qatar Petroleum’s subsidiary, Mesaieed Petrochemical Holding Company’s (MPHC) net profit plummeted 29% QoQ to QR212.4mn in 1Q2016. However, on a YoY basis net profit surged 83%, on the back of increased sales volumes and other income. The company’s profit growth was also aided by recognition of higher tax refund in 1Q2016. The company continued to benefit from the supply of competitively priced ethane feedstock and fuel gas under long- term supply agreements. This contracting arrangement is an important value driver for the group’s profitability in a challenging market condition. Earnings per share (EPS) came in at QR0.17 in 1Q2016 as compared to QR0.09 in 1Q2015. The company’s Share of profit from Joint Ventures declined 29% QoQ (up 86% YoY) to QR193.5mn in 1Q2016. (QSE, Zawya, QNBFS Research) QGMD posts QR2.1mn net loss in 1Q2016 – Qatari German Company for Medical Devices (QGMD) reported a net loss of QR2.1mn in 1Q2016 compared to a loss of QR2.0mn in 4Q2015. Revenue declined 70.1% QoQ and 34.5%YoY to reach 2.0mn in 1Q2016. The loss per share amounted to QR 0.18 in 1Q2016 compared to loss per share QR0.33 in 4Q2015. (QSE, QNBFS Research) AHCS net income down QoQ in 1Q2016 to QR129.2mn – Aamal Company (AHCS) recorded a decline of 53.0% QoQ in 1Q2016 net profit to QR129.2mn. However, on a YoY basis net profit surged 25.4%. Revenue fell 15.9% QoQ (up 6.9% YoY) to QR679.6mn in 1Q2016. AHCS Chairman Sheikh Faisal bin Qassim al-Thani said that its financial gearing (net debt to net debt plus equity) reduced further to 2.5% (against 3.8% as of December 31, 2015), which reflects the strong free cash flow generation, which is a testimony to the focus it has put on generating positive returns on the capital deployed, thereby helping to sustain its profitable growth and create shareholder value. He said “This low gearing also means that we can move swiftly should we identify suitable commercial

- 4. Page 4 of 7 opportunities that we would like to exploit”. In 1Q2016, AHCS continued to grow its operations through organic means, including investing to expand the bulk carrying capacity at Aamal Maritime Transportation Services through the acquisition of a second vessel. Earnings per share (EPS) amounted to QR0.21 in 1Q2016 vs. QR0.16 in 1Q2015. (QSE, Gulf-Times.com, QNBFS Research) NLCS comes out of the red in 1Q2016 – Alijarah Holding (NLCS) reported a net profit of QR2.1mn in 1Q2016 vs. a net loss of QR45.7mn in 4Q2015. The total income declined 5.1% QoQ to QR55.6mn. On a YoY basis, although net profit declined 63.0%, total income grew 4.0%. Earnings per share amounted to QR0.04 in 1Q2016 vs. QR0.12 in 1Q2015. (QSE, QNBFS Research) QGRI raises stake in Qatari Unified Bureau Insurance – Qatar General Insurance and Reinsurance Company (QGRI) announced its approval to increase its share in the Qatari Unified Bureau Insurance WLL from 20% to 25%, for an amount of QR6.8mn. Qatari Unified Bureau Insurance is a limited liability company established in 1999 and its activity is to provide insurance cover for vehicles entering the country and to sell insurance cards for vehicles traveling outside the country (QSE). Kahramaa bans import of incandescent light bulbs; launches major programs to maintain water security – Qatar General Electricity and Water Corporation (KAHRAMAA), in cooperation with the Ministry of Municipality and Environment and a number of agencies concerned in the state, announced a ban on import and circulation of incandescent light bulbs (Tungsten 75 and 100 watts), with effect from May 1, 2016, as part of a plan aiming to cut electricity and water consumption and harmful carbon emissions rates through the National Program for Conservation and Energy Efficiency (Tarsheed). Meanwhile, Kahramaa has launched major initiatives to achieve water security in the country. Water consumption in Qatar rose to 535mn cubic meters in 2015 from 195 million cubic meters in 2005, and its demand in Qatar has been growing by an annual average of 10.6% over the past 11 years and expected to reach about 902mn cubic meters in 2025. Kahramaa President, Eng Essa bin Hilal Al Kuwari said, “Qatar is known for its scarcity of renewable water resources and during the last decade pressure on water resources has increased significantly, due to natural climatic conditions, population increase, and intended level of agricultural and industrial development.”(Peninsula Qatar) UDCD unveils iconic Al Mutahidah Towers project – United Development Company (UDCD), the master developer of The Pear Qatar (TPQ), has unveiled a new project named “Al Mutahidah Towers” at the ongoing “Cityscape Qatar 2016” exhibition. Al Mutahidah Towers, consisting of around 450 high-end apartments and retail space, will be located at Viva Bahriya in TPQ, an urban mixed-use township close to West Bay. Ibrahim Jassim Al Othman, President & CEO, UDCD said, “We are planning to begin the construction works on the project by early fourth quarter of this year, which is expected to be completed within three years.” (Peninsula Qatar) Aspetar opens first sports surgery training center in region – Aspetar, the Doha-based orthopaedic and sports medicine hospital, opened the region’s first Sports Surgery Training Center for training surgeons in sports related injuries. Aspetar has targeted some countries in the region for the training, which include countries from the Middle East, North Africa (MENA) region and a few European and Asian countries. (Gulf-Times.com) Ezdan Mall to open in Wakrah by 2016-end – Residents of Wakrah are expected to see the first mall in the area opening its gates for customers in 2016. Ezdan Holding Group (ERES) announced it is planning to open the swanky Ezdan Mall in Wakrah by 2016-end. Spread over an area of 64,785 square meters, the mall will host several reputed global brands. (Peninsula Qatar) International US labor costs rise modestly in 1Q2016 – The Labor Department said US labor costs rose steadily in the 1Q2016 as the firming jobs market struggled to generate strong wage growth, which could give the Federal Reserve more latitude to hold off on an interest rate hike until later in 2016. The Employment Cost Index, the broadest measure of labor costs, increased 0.6% after an unrevised 0.5% gain in the 4Q2015. The 1Q2016 increase in the ECI was in line with economists' expectations. In the 12 months through March, labor costs rose 1.9%, well below the 3% threshold that economists say is needed to bring inflation closer to the Fed's 2% inflation target. Labor costs increased 2.0% in the year to December. (Reuters) UK mortgage approvals fall ahead of new tax, but lending surges – Bank of England (BoE) data showed British mortgage approvals fell for the first time in six months in March shortly before a new tax took effect, but consumers borrowed at the fastest rate in over a decade. Mortgage approvals for house purchases numbered 71,357 in March, down from 73,195 in February. Analysts had forecast 74,500 mortgage approvals were made in March. British finance minister George Osborne announced in November that he would add a surcharge on the purchase of buy-to-let properties and second homes from April 1, in a move aimed to boost home ownership by first-time buyers. The news spurred an increase in buying of such properties in recent months before March's slowdown as the deadline approached. Net mortgage lending, which lags approvals, rose by 7.435bn pounds last month, the biggest increase since October 2007, before the global financial crisis hit and above all forecasts. The BoE said consumer credit grew by 1.883bn pounds last month, the strongest increase since March 2005 and a long way above the median forecast for an increase of 1.3bn pounds in the Reuters poll of economists. The rise was not a one-off: in the 1Q2016 as a whole, consumer credit rose by an annualized 11.6%, the strongest increase since the first three months of 2015. The BoE has said it is not worried about the rise of borrowing in the economy as a whole although it has highlighted some areas of consumer lending, such as car loans, for closer monitoring. The BoE also said purchases of British government bonds by foreign investors touched their highest level in four months at 7.811bn pounds in March, more than reversing net sales of 3.029bn pounds in February. (Reuters) German industrial workers down tools in dispute over wages – More than 100,000 workers in the German metals and electrical industries staged walkouts across the country after labor union IG Metall rejected a wage offer for the 3.8mn employees it represents. IG Metall union turned down an offer from employers for a wage rise of 2.1%, saying it fell too far short of its demand for a 5% increase. The 2.1% over 24 months still keep workers on a restricted diet in favor of profits. IG Metall union said that warning strikes would continue into the coming week, adding that it would start 24-hour strikes if no agreement was reached by the Pentecost holiday in mid-May. The union said in the southwestern state of Baden-Wuerttemberg, the home of car brands Porsche and Mercedes, more than 37,000 workers from over 150 companies joined walkouts. Around 17,000 workers at companies including industrial group Thyssenkrupp and carmaker Daimler took part in industrial action in North Rhine-Westphalia. Overall, nearly 110,000 workers joined the walkouts and participated in industrial action. (Reuters) France sees economic growth spurt from consumers and business – The INSEE national statistics agency said in a preliminary estimate of gross domestic product (GDP) that the French growth

- 5. Page 5 of 7 accelerated more than expected at the start of 2016 with the strongest increase in consumer spending since 2004 and a pick-up in business investment. The economy grew 0.5% in the 1Q2016, beating even the most optimistic forecast in a Reuter’s poll, as consumers splurged on clothes, cars and housing equipment. Consumer spending was up 1.2% over the three months, with higher spending on heating after a mild end to 2015, also offering a boost and offsetting the impact of a global slowdown that hurt exports. If consumers led the way in the quarter, however, economists particularly took heart in a 1.6% rise in business investment, the strongest increase in five years. Investment by companies in the manufacturing sector surged by 3.3%, the highest since the spring of 2006. (Reuters) Russian central bank holds rates but says it may cut soon – Russia's central bank left its main policy rate on hold as expected, citing inflation concerns, but hinted it may cut it in the months ahead as inflation falls. The bank has now left the rate on hold at 11% since July, signaling its determination to bear down on inflation to meet its target of 4% by the end of 2017. It has made clear it regards this as a bigger worry than stimulating the economy, which is expected to contract for a second consecutive year in 2016 under the impact of low oil prices and Western financial sanctions linked to the Ukraine conflict. But in an accompanying statement, the bank also said a rate cut could take place at a "forthcoming" meeting should inflation risks abate. It has previously said this expression means at one of the next three central bank meetings. Although most analysts had expected rates to stay on hold, many had also foreseen a softening of rhetoric this month as a strong rally in oil prices has lifted the rouble. Inflation has also dropped sharply, falling to 7.3% in March from 16.9% in 2015. (Reuters) Regional Sipchem announces periodic maintenance turnaround for production units – Saudi International Petrochemical Company (Sipchem) is planning to carry out scheduled turnaround maintenance at the following production units: Carbon Monoxide of International Gases Company (IGC), Acetic Acid of International Acetate Company (IAC), and Ethyl Acetate of Sipchem Chemicals Company (SCC). This scheduled turnaround maintenance is in accordance with each of the above company 2016 business plans and is expected to increase both efficiency and reliability of each of the production units. The scheduled turnaround maintenance will commence on May 1, 2016 and is planned to be completed in 15 days. The financial impact of this activity will be announced once it is completed and will also be reflected in 2Q2016 financial results. (Tadawul) GGCI not to renew medical insurance policy with Al-Juffali Companies – Gulf General Cooperative Insurance Company (GGCI) will not renew the medical insurance policy with Al-Juffali Companies Group, which will expire on April 30, 2016. The gross written premium of this policy is estimated at SR0.41, which represents 11% of the company overall gross written premium of year 2015, and it is expected to have a negative impact on the company financials for year 2016. (Tadawul) Metlife-AIG-ANB announces renewal of insurance policies – Metlife- AIG-ANB Cooperative Insurance Company has announced the renewal of Property All Risk policy with face amount of SR2.61bn and Comprehensive General Liability Policy with a face amount of SR50mn and Property Terrorism Policy with face amount of SR75mn and Group Life and Disability insurance Policy for ANB employees with face amount of SR824.8mn with a total premium of SR2.59mn in favor of Arab National Bank. The proposals have been accepted on April 28, 2016. The duration of the policies is one year with effect from May 01, 2016 and renewable based on mutual agreement thereafter. (Tadawul) SAMA net foreign assets fall $6bn in March 2016 – The Saudi Arabian Monetary Agency (SAMA) reported a fall of $6bn in net foreign assets in March 2016 as low oil prices took their toll. Net foreign assets held by the central bank dropped by 1% from the previous month to SR2.17tn in March 2016. Assets fell 16.2%YoY to their lowest level since April 2012. They reached a record high of $737bn in August 2014 before starting to shrink. The central bank has been drawing down its assets to cover a huge state budget deficit caused by low oil prices. Deposits with banks abroad edged down 0.4% from the previous month to $132bn in February 2016, while investment in foreign securities fell 1.4% to $389bn. (Bloomberg) IPIC pays interest on bonds after 1MDB default – International Petroleum Investment Company (IPIC) has said that it had paid interest due on bonds issued by 1MDB Energy (Langat) to fulfill its obligation as a guarantor under the bonds’ terms. IPIC said the payment was made after Malaysian state fund 1Malaysia Development Bhd (1MDB) defaulted on the payments and that it would now demand indemnity for repayment of the $50.3mn interest. The coupon on the $1.75bn bond was due on April 18, 2016. (Reuters) DIB plans AED3.6bn share issue – Dubai Islamic Bank (DIB) is planning to raise AED3.6bn from a share issue, as 1Q2016 profit increased. The lender will sell 988.4mn shares at AED3.20 a piece. DIB’s board approved the start of the share sale process that will almost double share capital and support growth. (Bloomberg) UNB reports AED450mn net profit in 1Q2016 – Union National Bank (UNB) reported a net profit of AED450mn in 1Q2016, up by 131% over the preceding quarter and down by 27% YoY. The operating profit for 1Q2016 was AED551mn, a decrease of 19% YoY. The operating income for three month period ended March 31, 2016 was down by 13% to AED813mn as compared to the corresponding period of previous year. Loan & advances were up by 2% YoY to AED68.3bn as at March 31, 2016. The investment portfolio increased by 6% YoY to AED15.3bn as at March 31, 2016 partly to comply with the liquidity norms. The total assets of UNB registered a growth of 2% to AED99.8bn as at March 31, 2016 as compared to last year. Customer deposits stood at AED72.1bn by 1Q2016-end, registering an increase of 3% as compared to the corresponding period in the previous year. (ADX) KNPC signs KD1.2bn loan for fuels project – Kuwait National Petroleum Company (KNPC) has signed the first tranche of financing for its multi-billion-dollar Clean Fuels Project, a major plank of the country’s economic development plan. The tranche, provided by local banks and lasting for 10 years, is worth KD1.2bn and led by National Bank of Kuwait (NBK) and Kuwait Finance House (KFH). The second tranche of the loan, which will be arranged by international lenders, is expected to be $6bn and close by 2016-end. The two tranches comprise around 70% of the total financing required for the project, while the remaining 30% will be financed from KNPC's own funds. NBK’s share of the first tranche was worth KD400mn, and KFH’s portion was KD275mn. Eleven banks, including five Islamic lenders, took part in the first tranche. (Reuter) Boubyan Bank gets nod to issue Tier 1 Sukuk – Boubyan Bank has received regulatory approval to market and issue Sukuk, expected to be $250mn in size, to boost its Tier 1 or core capital. Reuters reported that the lender had picked banks to arrange a series of fixed income meetings starting on May 1, 2016, ahead of a potential US dollar-denominated Sukuk issue. (Reuters) OPWP floats tender for raising water capacity – Oman Power and Water Procurement Company (OPWP) has floated a tender seeking an international consultant to provide advisory services for enhancing water production capacity from 2022. The tender

- 6. Page 6 of 7 documents are available between April 25 and May 8, while the last date of bid submission is June 5. (GulfBase.com) IMF: Bahrain’s economy to slow further in 2016-17 – According to the International Monetary Fund (IMF), Bahrain’s economy is expected to slow further in 2016 and 2017, weighed down by weak investor sentiment and fiscal adjustments, with financial outflows expected to continue. The fund expects Bahrain’s fiscal deficit to touch 19.5% of gross domestic product (GDP) in 2016 and sees it remaining high over the medium term, despite measures to ensure fiscal sustainability. The Gulf country has seen revenues take a hit from falling oil prices, with its GDP slowing to an estimated 3.2% in 2015 from 4.5% in 2014. The IMF urged Bahrain to address impediments to private investment if the Gulf nation is to achieve diversified and sustainable growth, and stressed the importance of a fiscal contingency plan and a strong debt management strategy. (GulfBase.com)

- 7. Contacts Saugata Sarkar Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa ` QNB Financial Services Co. WLL One Person Company Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. WLL One Person Company (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg (#Market closed on April 29, 2016) Source: Bloomberg (*$ adjusted returns; #Market closed on April 29, 2016) 80.0 100.0 120.0 140.0 160.0 180.0 Apr-12 Apr-13 Apr-14 Apr-15 Apr-16 QSE Inde x S&P Pa n Ara b S&P GCC (0.2%) 0.3% (0.7%) (0.1%) 0.1% (1.0%) (0.4%) (1.6%) (0.8%) 0.0% 0.8% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,292.99 2.1 4.9 21.8 MSCI World Index 1,670.80 (0.4) (0.9) 0.5 Silver/Ounce 17.84 1.6 5.1 28.7 DJ Industrial 17,773.64 (0.3) (1.3) 2.0 Crude Oil (Brent)/Barrel (FM Future) 48.13 (0.0) 6.7 29.1 S&P 500 2,065.30 (0.5) (1.3) 1.0 Crude Oil (WTI)/Barrel (FM Future) 45.92 (0.2) 5.0 24.0 NASDAQ 100 4,775.36 (0.6) (2.7) (4.6) Natural Gas (Henry Hub)/MMBtu 1.91 0.8 0.5 (17.5) STOXX 600 341.48 (1.2) (0.1) (1.7) LPG Propane (Arab Gulf)/Ton# 49.63 0.0 5.0 26.8 DAX 10,038.97 (1.9) (1.4) (2.0) LPG Butane (Arab Gulf)/Ton 58.63 0.6 8.1 2.0 FTSE 100 6,241.89 (1.1) 0.6 (0.7) Euro 1.15 0.9 2.0 5.4 CAC 40 4,428.96 (1.9) (1.2) 0.6 Yen 106.50 (1.5) (4.7) (11.4) Nikkei# 16,666.05 0.0 (2.3) (2.5) GBP 1.46 0.0 1.5 (0.8) MSCI EM 840.19 (0.5) (0.6) 5.8 CHF 1.04 0.8 2.0 4.5 SHANGHAI SE Composite 2,938.32 (0.2) (0.2) (16.8) AUD 0.76 (0.3) (1.4) 4.4 HANG SENG 21,067.05 (1.5) (1.9) (4.0) USD Index 93.08 (0.7) (2.1) (5.6) BSE SENSEX 25,606.62 (0.1) (0.5) (2.2) RUB 64.77 0.0 (2.7) (10.7) Bovespa 53,910.51 0.1 5.7 42.5 BRL 0.29 1.6 3.8 15.3 RTS 951.11 (1.4) 2.1 25.6 115.2 90.6 90.0