Solution Manual for Financial Accounting, 11th Edition by Robert Libby, Patri...

15 July Daily market report

1. Page 1 of 8

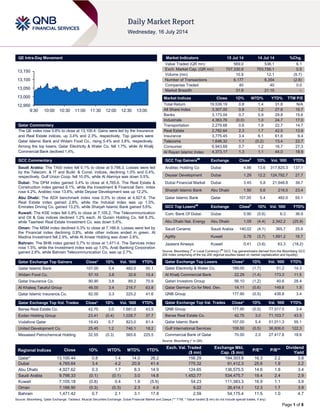

QE Intra-Day Movement

Qatar Commentary

The QE index rose 0.8% to close at 13,100.4. Gains were led by the Insurance

and Real Estate indices, up 3.4% and 2.3%, respectively. Top gainers were

Qatar Islamic Bank and Widam Food Co., rising 5.4% and 3.8%, respectively.

Among the top losers, Qatar Electricity & Water Co. fell 1.7%, while Al Khalij

Commercial Bank declined 1.4%.

GCC Commentary

Saudi Arabia: The TASI index fell 0.1% to close at 9,798.3. Losses were led

by the Telecom. & IT and Build. & Const. indices, declining 1.0% and 0.4%,

respectively. Gulf Union Coop. fell 10.0%, while Al Alamiya was down 5.5%.

Dubai: The DFM index gained 3.4% to close at 4,765.6. The Real Estate &

Construction index gained 6.1%, while the Investment & Financial Serv. index

rose 4.2%. Arabtec rose 13.6%, while Deyaar Development was up 12.2%.

Abu Dhabi: The ADX benchmark index rose 0.3% to close at 4,927.6. The

Real Estate index gained 2.8%, while the Indusial index was up 1.5%.

Emirates Driving Co. gained 13.2%, while Sharjah Islamic Bank gained 5.6%.

Kuwait: The KSE index fell 0.8% to close at 7,105.2. The Telecommunication

and Oil & Gas indices declined 1.2% each. Al Qurain Holding Co. fell 6.3%,

while Taameer Real Estate Investment Co. was down 5.6%.

Oman: The MSM index declined 0.3% to close at 7,166.9. Losses were led by

the Financial index declining 0.8%, while other indices ended in green. Al

Madina Investment fell 2.9%, while Al Anwar Holding was down 2.8%.

Bahrain: The BHB index gained 0.7% to close at 1,471.4. The Services index

rose 1.5%, while the Investment index was up 1.0%. Arab Banking Corporation

gained 2.8%, while Bahrain Telecommunication Co. was up 2.7%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar Islamic Bank 107.00 5.4 482.0 55.1

Widam Food Co. 57.10 3.8 32.6 10.4

Qatar Insurance Co. 90.90 3.8 89.2 70.9

Al Khaleej Takaful Group 46.00 3.4 216.7 63.8

Qatar Islamic Insurance Co. 82.00 3.3 225.2 41.6

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Barwa Real Estate Co. 42.75 3.0 1,681.0 43.5

Ezdan Holding Group 23.41 (0.4) 1,028.7 37.7

Vodafone Qatar 19.43 0.7 823.0 81.4

United Development Co. 25.45 1.2 746.1 18.2

Mesaieed Petrochemical Holding 32.55 (0.3) 565.6 225.5

Market Indicators 15 Jul 14 14 Jul 14 %Chg.

Value Traded (QR mn) 569.0 536.1 6.1

Exch. Market Cap. (QR mn) 707,330.9 703,756.1 0.5

Volume (mn) 10.9 12.1 (9.7)

Number of Transactions 6,177 6,354 (2.8)

Companies Traded 40 40 0.0

Market Breadth 31:8 21:15 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 19,539.19 0.8 1.4 31.8 N/A

All Share Index 3,307.00 0.8 1.2 27.8 15.7

Banks 3,173.04 0.7 0.9 29.8 15.6

Industrials 4,363.76 (0.0) 1.0 24.7 17.0

Transportation 2,279.68 0.6 1.9 22.7 14.7

Real Estate 2,782.64 2.3 1.7 42.5 13.9

Insurance 3,775.45 3.4 6.1 61.6 9.4

Telecoms 1,648.32 1.1 (0.2) 13.4 22.7

Consumer 6,943.69 0.7 1.2 16.7 27.3

Al Rayan Islamic Index 4,373.17 1.3 1.1 44.0 18.9

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Arabtec Holding Co Dubai 4.86 13.6 317,825.3 137.1

Deyaar Development Dubai 1.29 12.2 124,792.7 27.7

Dubai Financial Market Dubai 3.45 5.8 21,648.8 39.7

Sharjah Islamic Bank Abu Dhabi 1.90 5.6 216.5 23.4

Qatar Islamic Bank Qatar 107.00 5.4 482.0 55.1

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Com. Bank Of Dubai Dubai 5.90 (5.6) 6.3 36.9

Abu Dhabi Nat. Energy Abu Dhabi 1.09 (4.4) 2,342.2 (25.9)

Saudi Ceramic Saudi Arabia 140.02 (4.1) 365.7 25.6

Agility Kuwait 0.78 (3.7) 1,691.2 18.7

Jazeera Airways Kuwait 0.41 (3.6) 63.3 (18.2)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Qatar Electricity & Water Co. 189.00 (1.7) 51.2 14.3

Al Khalij Commercial Bank 22.29 (1.4) 173.3 11.5

Qatari Investors Group 56.10 (1.2) 40.6 28.4

Qatar German Co for Med. Dev. 14.11 (0.6) 149.6 1.9

QNB Group 177.90 (0.5) 438.8 3.4

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

QNB Group 177.90 (0.5) 77,517.5 3.4

Barwa Real Estate Co. 42.75 3.0 71,103.7 43.5

Qatar Islamic Bank 107.00 5.4 51,011.3 55.1

Gulf International Services 108.50 (0.5) 36,806.0 122.3

Commercial Bank of Qatar 70.00 2.0 27,417.8 18.6

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 13,100.44 0.8 1.4 14.0 26.2 156.29 194,303.8 16.3 2.2 3.8

Dubai 4,765.64 3.4 4.2 20.9 41.4 775.32 91,412.3 25.6 1.9 2.2

Abu Dhabi 4,927.62 0.3 1.7 8.3 14.9 124.65 136,575.5 14.6 1.8 3.4

Saudi Arabia 9,798.33 (0.1) (0.1) 3.0 14.8 1,452.77 534,475.7 19.4 2.4 2.9

Kuwait 7,105.18 (0.8) 0.4 1.9 (5.9) 54.23 111,383.3 16.9 1.1 3.9

Oman 7,166.90 (0.3) (0.3) 2.3 4.9 9.22 26,414.1 12.3 1.7 3.9

Bahrain 1,471.42 0.7 2.1 3.1 17.8 2.59 54,175.4 11.5 1.0 4.7

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,950

13,000

13,050

13,100

13,150

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 8

Qatar Market Commentary

The QE index rose 0.8% to close at 13,100.4. The Insurance and

Real Estate indices led the gains. The index rose on the back of

buying support from non-Qatari shareholders despite selling

pressure from Qatari shareholders.

Qatar Islamic Bank and Widam Food Co. were the top gainers,

rising 5.4% and 3.8%, respectively. Among the top losers, Qatar

Electricity & Water Co. fell 1.7%, while Al Khalij Commercial

Bank declined 1.4%.

Volume of shares traded on Tuesday fell by 9.7% to 10.9mn

from 12.1mn on Monday. Further, as compared to the 30-day

moving average of 16.0mn, volume for the day was 31.8% lower.

Barwa Real Estate Co. and Ezdan Holding Group were the most

active stocks, contributing 15.4% and 9.4% to the total volume

respectively.

Source: Qatar Exchange (* as a % of traded value)

Earnings and Global Economic Data

Earnings Releases

Company Market Currency

Revenue

(mn)2Q2014

% Change

YoY

Operating Profit

(mn) 2Q2014

% Change

YoY

Net Profit (mn)

2Q2014

% Change

YoY

The National Shipping Co.

(Bahri)

Saudi SR – – 119.3 -22.4% 130.4 -20.7%

National Agriculture

Development Co. (NADEC)

Saudi SR – – 34.6 -8.2% 28.0 -6.7%

Saudi Arabian Mining

Company (Maaden)

Saudi SR – – 501.5 512.1% 370.8 804.8%

Sahara Petrochemical Co. Saudi SR – – 90.3 -10.0% 185.0 46.0%

Saudi Pharmaceutical

Industries & Medical

Appliances Corp.

(SPIMACO)

Saudi SR – – 42.6 4.9% 97.7 -14.1%

Alkhaleej Training &

Education Co.

Saudi SR – – 23.3 13.6% 21.5 17.4%

Aldrees Petroleum &

Transport Services Co.

(APTSCO)

Saudi SR – – 39.3 38.4% 35.4 29.2%

Advanced Petrochemical

Co. (APC)

Saudi SR – – 183.2 30.7% 184.6 35.1%

Saudi Chemical Co. (SCC) Saudi SR – – 93.7 5.5% 86.6 12.3%

Shuaa Capital Dubai AED 52.0 19.8% – – 6.2 376.9%

Dhofar Beverages Food

Stuff Co.**

Oman OMR 2.4 11.5% – – 0.1 48.7%

Dhofar Poultry Co. (DPC)* Oman OMR 1.5 -32.1% – – -0.9 NA

The Financial Corporation

(FINCORP)

Oman OMR 0.3 -22.3% – – -0.2 NA

Gulf Mushroom Products

Co. (GMPC)*

Oman OMR 3.3 -1.7% – – 0.2 -57.9%

Takaful Oman Insurance Oman OMR 0.1 NA – – -0.1 NA

Oman National Engineering

& Investment Co. (ONEIC)

Oman OMR 19.1 8.1% – – 1.1 -21.8%

Source: Company data, DFM, ADX, MSM (** FY2014 results, *1H2014 results)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

07/15 US Federal Reserve NY Empire Manufacturing July 25.6 17.0 19.9

07/15 US BLS Import Price Index MoM June 0.10% 0.40% 0.30%

07/15 US BLS Import Price Index YoY June 1.20% 1.10% 0.60%

07/15 US US Census Bureau Business Inventories May 0.50% 0.60% 0.60%

07/15 EU ZEW ZEW Survey Expectations July 48.1 – 58.4

07/15 Germany ZEW ZEW Survey Current Situation July 61.8 67.4 67.7

07/15 Germany ZEW ZEW Survey Expectations July 27.1 28.2 29.8

07/15 UK ONS CPI MoM June 0.20% -0.10% -0.10%

07/15 UK ONS CPI YoY June 1.90% 1.60% 1.50%

07/15 UK ONS CPI Core YoY June 2.00% 1.70% 1.60%

07/15 UK ONS Retail Price Index June 256.3 255.9 255.9

07/15 UK ONS RPI MoM June 0.20% 0.00% 0.10%

Overall Activity Buy %* Sell %* Net (QR)

Qatari 54.19% 65.40% (63,834,670.49)

Non-Qatari 45.82% 34.59% 63,834,670.49

3. Page 3 of 8

07/15 UK ONS RPI YoY June 2.60% 2.50% 2.40%

07/15 UK ONS ONS House Price YoY May 10.50% 10.10% 9.90%

07/15 Italy ISTAT CPI FOI Index Ex Tobacco June 107.4 – 107.3

07/15 Italy ISTAT CPI EU Harmonized YoY June 0.20% 0.20% 0.20%

07/15 China NBS New Yuan Loans June 1080.0B 955.0B 870.8B

07/15 China NBS Aggregate Financing RMB June 1970.0B 1425.0B 1404.5B

07/15 China PBC Money Supply M0 YoY June 5.30% 7.00% 6.70%

07/15 China PBC Money Supply M2 YoY June 14.70% 13.60% 13.40%

07/15 China PBC Money Supply M1 YoY June 8.90% 6.30% 5.70%

07/15 China NBS Foreign Reserves June $3990.0B $3980.0B $3948.1B

07/15 China NBS Foreign Direct Investment YoY June 0.20% -7.00% -6.70%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

MARK to resume trading after disclosing details of JV sale

– Masraf Al Rayan (MARK) offered more details into the sale of

its stake in a real estate JV to a state fund, after the country's

stock exchange suspended the bank's shares for a lack of clarity

on the deal. MARK, which has the largest MSCI weighting of

any Qatari stock, said it was selling its 50% stake in Seef Lusail

Real Estate Development Co to the real estate arm of the Gulf

state's sovereign wealth fund. MARK provided information on

the split going to each of the two arms of Qatari Diar. As a

result, the regulatory authorities in the Gulf state suspended the

stock prior to trading on Tuesday until more clarity was given.

MARK said the sale price would be QR1.53bn, which would

generate a gain of QR466mn for the bank spread over three

years. (Reuters)

QATI posts a strong set of results, to set up subsidiary in

Malta – Strong performance in 2Q2014: Qatar Insurance (QATI)

posted a net profit of ~QR319.0mn in 2Q2014 vs. QR316.5mn in

1Q2014 and QR133.7mn in 2Q2013. On a QoQ basis, the net

income was up 0.8%. However, on a YoY basis the net income

was up 138.7%. 2Q2014 analysis: QATI’s gross written premium

(GWP) stood at QR2.1bn vs. QR1.1bn (growth of 88.2% QoQ

and 114.8% YoY). This is a very strong number as due to

seasonal factors the first and third quarters are usually the

strong quarters for the insurance business. We believe

international operations, primarily the reinsurance business,

could be the primary driver of this strong growth. Overall net

underwriting results increased to QR208.3mn in 2Q2014 vs.

QR178.5mn in 1Q2014, a growth of 16.7% QoQ (150.5% YoY).

On the investment front, investment income increased to

QR290.2mn vs. QR221.9mn, a growth of 30.8% QoQ. We

believe the strong performance of regional equity markets

allowed the firm to post a strong show despite the absence of

dividends in the second quarter. This lead to total income

reaching QR532.8mn vs. QR445.5mn, a growth of 19.6% QoQ

(134.4% YoY). Meanwhile, QATI’s board of directors have

approved the issuance of five-year convertible bonds into shares

of QATI with a total value of $250mn, in order to meet the future

capital requirements as well as match the growth rates expected

for the insurance activities over the next few years. The BoD

also approved the establishment of a subsidiary insurance

company in Malta to attract good and strategic risks from the

various European countries. (QNBFS, QE)

QGTS posts QR446mn net profit in 1H2014, up 24% – Qatar

Gas Transport Company (QGTS) posted a net profit of

QR446mn in 1H2014, up 24% on a YoY basis. Nakilat’s strong

earnings reflected the strength and stability of its financial

position, and the prudent & effective strategic plan related to the

development of its main business activities in the transportation

of LNG to international markets. This has resulted in an increase

in the number of operating vessels in Nakilat fleet in 1H2014.

The board of directors pointed out that the positive effect of the

remarkable improvement in the international charter rate for the

transportation of liquefied petroleum gas vessels, and the

increased operating activities at the shipyard facilities, will

continue to underpin the future financial results of the company.

The board has affirmed Nakilat’s commitment to pursue its

development and growth strategy in order to achieve strong

returns for its shareholders. The company said it will continue to

look for good opportunities to acquire new vessels, and to

increase the utilization rate for its facilities at “Erhama Bin Jaber

Al Jalahma Shipyard”. (Gulf-Times.com)

MDPS: Qatar June CPI stands at 117.7 – The Ministry of

Development Planning & Statistics (MDPS) released the

Consumer Price Index (CPI) for the month of June, 2014. The

CPI of June 2014 is estimated at 117.7, showing a decrease of

0.1% as compared to the CPI of May 2014, indicating an

increase of 2.8% as compared to the CPI of June 2013. The

overall decrease of 0.1% in the CPI of June, 2014 when

compared to the CPI of May 2014 is a result of the combined

effect of price increases recorded in the main groups: rentals,

fuel & energy by 0.6%, food, beverages & tobacco by 0.2% and

transport & communication by 0.1%; and price falls witnessed in:

garments & footwear by 2.6%, entertainment, recreation &

culture by 0.9%, furniture, textiles & home appliances and

miscellaneous goods & services by 0.1% each, while medical

care remaining stable at previous month’s level. The 2.8% YoY

increase in CPI of June resulted from the price increases

observed in most of the groups: rentals, fuel & energy by 7.4%,

furniture, textiles & home appliances by 4.9%, transport &

communication by 1.4%, entertainment, recreation & culture by

1.2%, garments & footwear by 1.1% and medical care by 0.6%,

On the other hand, the food the beverages & tobacco index

declined by 0.6%. (QSA)

Qatar’s gross national income rises 3.2% to QR183.6bn in

1Q2014 – The Ministry of Development Planning & Statistics

(MDPS) said that Qatar’s gross national income (GNI) rose by

3.2% to QR183.6bn in 1Q2014, as compared to 1Q2013. MDPS

said that the GNI was derived by adding the country’s net

property income from the rest of the world to its national GDP.

GNI has gone up by 4% in 1Q2014 on a QoQ basis. The

comparable rise in GDP was 2.1% over the same period. The

Household Final Consumption Expenditure (HFCE) for 1Q2014

was estimated at QR26.5bn as compared to QR24.83bn in

1Q2013, showed an increase of 6.7%. The MDPS said that the

country’s rising population has been the prime cause of such a

rise. The share of HFCE in the GDP in 1Q2013 and 2014 are

estimated at 13.2% and 13.8% respectively. The Government

Final Consumption Expenditure (GFCE) was estimated at

QR24.98bn in Q1, 2014 as compared to QR23.74bn in Q1,

2013, showing a rise of 5.2%. The share of GFCE in nominal

4. Page 4 of 8

GDP during 1Q2013 and 1Q2014 were estimated at 12.7% and

13.0% respectively. The total value of exports (at FOB) from the

country was placed at QR146.03bn in 1Q2014 as compared to

QR141.15bn in 1Q2013, indicating an increase of 3.5%. This

YoY increase in 1Q2014 was mainly driven by the rising exports

of chemicals & related products, mineral fuels, lubricants &

related materials; besides an increase that was seen in some of

the services such as travel and transportation. The total value of

imports (at FOB) in the country was placed at QR59.37bn in

1Q2014 as compared to QR52.45bn in 1Q2013, reflecting an

increase of 13.2%. This YoY jump in imports was primarily

because of the increases seen in the imports of machinery &

transport equipment, miscellaneous manufactured articles, food

& live animals, chemicals & related products, other

manufactured goods & travel and transportation services. The

MDPS said that the share of imports in 1Q2013 and 1Q2014

were estimated at 28.0% and 30.9%, respectively. (Gulf-

Times.com)

Real estate deals stood at QR1,865.4mn between July 6-10 –

The real estate registration department at the Ministry said that

the real estate transactions registered at the Ministry of Justice

between July 6 and 10 were worth QR1,865.4mn. The list of

properties that were traded by sale includes open plots of land,

two-floor villas, annexes, houses, towers, residential buildings

and complexes and shops located in the municipalities of Umm

Salal, Al Khor, Al Dhakira, Doha, Al Rayyan, Al Shamal, Al

Daayen and Al Wakrah. (Gulf-Times.com)

MCCS to announce results on August 8 – Mannai

Corporation (MCCS) will disclose its financial reports for the

period ending June 30, 2014, on August 8, 2014. (QE)

International

Yellen: Weak job market shows US still needs stimulus;

sees risk of bubbles in leveraged loan market – Federal

Reserve Chairman Janet Yellen told lawmakers that the central

bank must press on with record monetary stimulus to combat

persistent job-market weakness. Yellen said there are mixed

signals concerning the economy. She stated that the Fed needs

to be careful to ensure the economy is on a solid trajectory

before it considers raising interest rates. While her “overall view

is more positive,” Yellen said low wages are one sign of

“significant slack” in labor markets, even after the jobless rate

fell to an almost six-year low. In an unusually emotive language

for a central banker, she talked about the “psychological trauma”

suffered by the unemployed and their families. Meanwhile,

Yellen warned of asset price bubbles forming in some markets

such as those for leveraged loans and lower-rated corporate

debt, while indicating stocks are not overvalued. She sees

deterioration in lending standards, and stressed on being

attentive to risks that can develop in this low interest rate

environment. Yellen said the low interest rates can be conducive

to the formation of bubbles, and that the Fed was carefully

watching for signs of such increased risk-taking. She cautioned

that the central bank will not “be able to catch every asset

bubble.” (Bloomberg)

Carney: BoE only giving guidance on rates in medium-term

– Bank of England (BoE) Governor Mark Carney said the bank

will not give guidance on the timing of the first rate increase and

warned officials it will only provide an outlook for the medium-

term. Carney said the policy makers are focused on the inflation

target and do not aim to satisfy the market expectations on

rates. The governor also said that there is an illusion of liquidity

in the market because of low volatility and that this may adjust

when rates begin to rise. Carney’s comments follow his warning

last month that a rate increase this year was more likely than

investors were anticipating. While the governor has softened

that stance since then, improving data has heightened the

debate over when the monetary policy committee will lift

borrowing costs from a record low. A report today showed

inflation accelerated to the fastest annual pace since January.

(Bloomberg)

UK inflation jumps in June, rate hike bets brought forward –

British inflation surged to a five-month high last month and

house prices rose at their fastest rate in years, prompting

investors to increase bets on an interest rate rise before the end

of 2014. Underlining the challenge facing the Bank of England

as it tries to manage Britain's accelerating economic recovery,

consumer prices rose 1.9% on the year in June, official ONS

data showed. According to a Reuters poll of economists, the

jump from a four-and-a-half-year low of 1.5% in May far

outstripped forecasts for only a slight rise. The separate figures

showed the real estate market also picked up speed as London

property prices leapt by a record 20.1% over the 12 months to

May. Speaking after the data - which brought consumer price

growth close to the bank's 2% target - BoE Governor Mark

Carney said inflation expectations were "extremely well

anchored" and had improved over the last year. (Reuters)

BNP fine spotlights banks need for in-house police force –

Ignoring the rules has never been so pricey for European

lenders, spurring them to hire more people to ferret out

wrongdoing and offer salaries more in line with the bankers they

police. After the US extracted almost $12bn in fines in

settlements with France’s BNP Paribas SA (BNP) and Zurich-

based Credit Suisse Group AG (CSGN) since May, European

firms say they are overhauling culture and boosting pay for

compliance staff faster than for revenue-earning bankers. Still

lawyers question whether this will be enough to deter future

misdeeds as authorities around the world probe alleged

manipulation of interest rate, foreign exchange and gold

benchmarks. According to a Morgan Stanley report for banks,

there is an incentive to change: European firms may have to set

aside $50bn, on top of the $80bn already provisioned or paid, to

cover litigation and settlement costs. European banks are not

alone in paying dearly for misdeeds. Citigroup Inc. agreed this

week to pay $7bn in fines and consumer relief to end an

investigation into allegations the New York-based firm misled

investors in mortgage-backed bonds. (Bloomberg)

BRICS agree on $50bn bank with something for everyone –

Leaders of the five BRICS nations agreed on the structure of a

$50bn development bank by granting China its headquarters

and India its first rotating presidency. Brazil, Russia and South

Africa were also granted posts or units in the new bank.

According to a statement issued at a summit in Fortaleza, Brazil,

the leaders also formalized the creation of a $100bn currency

exchange reserve, which member states can tap in case of

balance of payment crises. Both initiatives, which require

legislative approval, are designed to provide an alternative to

financing from the IMF and the World Bank, where BRICS

countries have been seeking more say. According to economists

surveyed by Bloomberg, the measures coincide with a slowing

of economic growth in the five countries to about 5.4% this year

from 10.7% in 2007. Brazilian President Dilma Rousseff said the

BRICS are gaining political weight and demonstrating their role

in the international arena. (Bloomberg)

China growth data to show stimulus kicking in but more

support may be needed – China’s leaders are expecting to see

a dividend from three months of stimulus spending in second-

quarter growth data on Wednesday, but the economy may need

even more state support to meet this year’s growth target of

7.5%. An unexpectedly hefty increase in bank loans in June is

5. Page 5 of 8

being taken as a signal of Beijing’s alarm at the slowdown, and

how far it is prepared to go to ensure growth gets back on track.

A Reuters poll showed China's economy likely grew 7.4% in

April-June from the same period a year earlier, unchanged from

the pace in the first quarter thanks to a raft of government

stimulus measures. The first-quarter reading was the weakest in

18 months. But there could be a modest upside surprise, given

that Premier Li Keqiang said last week that the growth

quickened in the second quarter from the previous three

months. Still, many economists believe more policy support may

be needed in the coming months to sustain any recovery,

particularly if the cooling property market begins to deteriorate

more sharply. (Reuters)

Goldman Sachs second-quarter profit up 5% – Goldman

Sachs Group Inc reported a 5% increase in second-quarter

profit, driven by higher revenue from its investing and lending

business. The Wall Street bank earned $1.95bn, or $4.10 per

share, in the three months ended 30 June 2014, up from

$1.86bn, or $3.70 per share, in the same period a year earlier.

(Reuters)

Regional

Visa partners with Borderfree to offer special promotions –

Visa, a global payments technology company, has partnered

with Borderfree, an e-commerce company, to offer special

promotions from retailers in the US to customers in the UAE,

Saudi Arabia, Kuwait, Qatar, Bahrain and Jordan. Borderfree

operates a technology and services platform that allows US

retailers to transact with customers in more than 100 countries

and territories. (GulfBase.com)

KEFI Minerals’ Saudi drilling returns more strong results –

KEFI Minerals has unveiled more strong drill results from its

Jibal Qutman gold project in Saudi Arabia. Targeting the South

Zone and 4K Hill, the latest stage of the exploration program

returned 3.72 grams per ton of the precious metal over 17

meters, 3.22 grams over 8 meters and 22 meters at 2.51 grams.

KEFI also revealed a total of 16 new trenches for 1,970 meters

were excavated in the South Zone southeastern extension and

4K Hill zone with the results pending. The preliminary feasibility

study for Jibal Qutman completed in March is currently being

reviewed by the firm’s partner ARTAR as well as by the Saudi

authorities. The company is the operator of Jibal Qutman under

its 40% owned Gold & Minerals joint venture. (GulfBase.com)

Tadawul deposits AlHokair’s bonus shares – The Saudi

Stock Exchange (Tadawul) announced that the bonus shares of

Fawaz Abdulaziz AlHokair Company (AlHokair) have been

deposited into investor’s portfolios. The fluctuation limits for

AlHokair on July 15, 2014 will be based on a share price of

SR107.13. Earlier, on July 14, 2014 AlHokair’s EGM had

approved the capital increase via bonus shares. (Tadawul)

SADAFCO to distribute SR113.75mn dividend – Saudia Dairy

& Foodstuff Company’s (SADAFCO) extraordinary general

meeting has approved the distribution of dividends amounting to

SR113.75mn (SR3.5 per share) for the financial year ended

March 31, 2014. Shareholders who are on the Tadawul list at

the closing of trade on the annual general meeting date of July

24, 2014 can avail the dividends. The dividends will be

distributed on July 21, 2014. (Tadawul)

Herfy Food to distribute SR69.3mn dividend for 1H2014 –

Herfy Food Services Company’s board of directors has

recommended the distribution of 15% dividend (SR1.5 per

share) amounting to SR69.3mn for 1H2014. The shareholders

registered in the registers of the Securities Depository Center

(Tadawul) on July 24, 2014 will be eligible for dividends.

(Tadawul)

Al Rajhi Bank lowers dividend for 1H2014 – Al Rajhi Bank

has proposed a cash dividend of SR1 per share for 1H2014.

This is below the SR1.38 per share the bank paid for the

corresponding period of 2013. (Reuters)

Abraaj Group acquires majority stake in Tunisia hospital –

Abraaj Group has acquired a majority stake in a Tunisia-based

private hospital Polyclinique Taoufi. The hospital currently treats

75,000 patients per year, offering services such as general

surgery, heart surgery, neurosurgery and obstetrics. The

investment is expected to increase patient capacity and add new

services. (GulfBase.com)

Emirates NBD appoints Country Head for India – Emirates

NBD has appointed Sharad Agarwal as its Chief Representative

and Country Head for India. Earlier, Agarwal headed trade

sales, factoring and escrow business for Emirates NBD based at

the bank’s head office, Dubai. The appointment is part of

Emirates NBD's objective to capture a greater share of bilateral

trade flows, and also identify other business opportunities.

(Bloomberg)

Moody’s: Emirates NBD economic recovery lifts franchise,

but problems persist – According to Moody’s, Emirates NBD

has benefited greatly from the ongoing economic recovery.

However, the issues of credit concentrations and asset quality

weakness continue to persist. Moody’s said that the ongoing

economic recovery will lead to further declines in Emirates

NBD’s non-performing loans (NPLs) and support profitability.

Moody’s expects the bank’s NPL ratio to decline to below 14%

in the next twelve months. As core sectors register solid growth

and the real estate sector recovers, Moody’s expects corporate

and retail borrowers’ repayment capacity to improve and

recoveries on impaired real estate and construction exposures

to increase. Moody’s states that despite the expected

improvements, Emirates NBD’s risk profile will continue to

remain constrained by its high exposure to its majority

shareholder, the Dubai government, and related government

enterprises. In marked contrast to other UAE financial

institutions that have actively reduced risk concentrations in their

loan books, the related-party lending at Emirates NBD has

continued to rise significantly over the last five years.

(GulfBase.com)

EFS wins contracts worth AED400mn in 1H2014 – EFS

Facilities Service Group has won new contracts worth more than

AED400mn in 1H2014. The new deals included contracts for the

provision of integrated facilities management services for Abu

Dhabi Education Council (ADEC) schools, Abu Dhabi

government buildings, local and international banks as well as

Fortune 500 multinationals. (GulfBase.com)

DFM distributes Agility’s bonus shares – Dubai Financial

Market (DFM) announced that the bonus shares distribution

action was executed for Agility Public Warehousing Company on

July 14, 2014. The action was executed on shareholders’

accounts whether with brokers or with the CSD, depending on

the balances status as of the closing date of July 9, 2014.

Earlier, Agility announced to distribute 5% bonus shares (5

shares for every 100 shares). (DFM)

NBAD broadens scope of regional funds – The National Bank

of Abu Dhabi (NBAD) has rebranded several of its equity funds

moving investment focus to a broader MENA focus from a UAE

emphasis. The expanded scope, diversification and geography

of the rebranded regional funds will offer new opportunities to

institutional and retail investors. The adjustment applies to

6. Page 6 of 8

NBAD UAE Islamic Fund (Al Naeem), rebranded to NBAD

Islamic MENA Growth Fund; NBAD GCC Opportunities (AJAJ),

rebranded to NBAD MENA Growth Fund; and NBAD UAE

Distribution, rebranded to NBAD MENA Income & Growth Fund.

(GulfBase.com)

ADNOC Distribution launches new service station in

Sharjah – Abu Dhabi National Oil Company for Distribution

(ADNOC Distribution) announced the opening of the Al Weshah

service station at Al Zaid City in Sharjah, marking an important

milestone in enhancing the operational capacity of the company

and boosting its expansion plans. The 40,000 sq feet facility on

the Al Madam road is fitted with six fuel dispensers and offers

round-the-clock allied services, including oil change and the

distribution of a wide range of lubricants and LPG cylinders.

(GulfBase.com)

Gulf Bank 2Q2014 profit rises 9% – Gulf Bank reported a net

profit of KD6.87mn in 2Q2014 as compared to KD6.3mn in

2Q2013, reflecting an increase of 9%, according to Reuters

calculations. The bank posted a net profit of KD15.6mn in

1H2014, up 9.5% YoY. (Reuters)

Iraqi court lifts freeze on Zain Iraq earnings – Zain Kuwait

announced that an Iraqi court has lifted a freeze on revenues of

its subsidiary Zain Iraq, after a $4.5bn lawsuit against the Iraqi

firm was dismissed earlier this month. Earlier, in April 2014, Zain

revealed that its Iraqi unit was being sued by a local

telecommunications firm over the $1.2bn acquisition of rival

operator Iraqna from Egypt's Orascom Telecom in 2007. The

unidentified plaintiff also sought damages from Iraq's

telecommunications regulator, the Communications and Media

Commission (CMC). However, Zain last week said an Iraqi court

had dismissed the case against both Zain Iraq and the CMC.

This cleared the way for Zain Iraq to apply for the freeze on its

money to be lifted. (Reuters)

CGC wins KD81.97mn contract to build crude oil pipelines –

Combined Group Contracting Company (CGC) has won a

KD81.97mn tender on July 10, 2014 to build crude oil pipelines

and any related works in North Kuwait region, which belongs to

Kuwait Oil Company (KOC) within a period of 66 months as of

September 1, 2014. (Bloomberg)

CMA disapproves Al Deera’s share buyback proposal – Al

Deera Holding Company announced that the Capital Markets

Authority (CMA) did not approve buying back a maximum of

10% of its shares due to lack of balance in the company's

reserves to cover the purchase procedures and selling 302.110

of its shares for 6 months as of July 13, 2014. (Bloomberg)

HSBC Bank Oman appoints new GM & Head of RBWM –

HSBC Bank Oman has appointed Abdul Qader bin Ahmed Al

Sumali as its new General Manager (GM) and Head of Retail

Banking & Wealth Management (RBWM). Al Sumali will be

responsible for driving and expanding the bank's retail banking

and wealth management presence in Oman. He had joined the

bank in 2013 as Deputy General Manager, RBWM.

(GulfBase.com)

Bank Muscat wins StanChart award for fund transfer – Bank

Muscat has won an award from Standard Chartered Bank for

outstanding performance in fund transfer related to dollar

payments. The bank received the straight through processing

(STP) Excellence Award for USD payments for the year 2013.

The award is testimony to the bank’s commitment to high

standards in meeting the stringent fund transfer criteria.

(GulfBase.com)

ORPIC awards contracts worth $80mn – Oman Oil Refineries

& Petroleum Industries Company (ORPIC) has awarded five

technology licensor contracts valued at around $80mn for its

$3.6bn Liwa Plastic Project (LPP). The contracts relate to

various LPP units, namely, NGL Extraction, PyGas

Hydrogenation, MTBE, Polypropylene, and Polyethylene. The

NGL extraction technology will be provided by Randall and put

to use in a natural gas extraction plant located in Fahud. The

technology for the PyGas Hydrogenation unit is going to be

provided by Axens. This unit is designed to produce a number of

high-value components, such as isoprene, benzene, toluene

and xylenes. A licensor contract has also been awarded to

Basell Poliolefine, who will be providing the technological

requirement for the Polypropylene unit. In addition, Univation will

be the technology provider for the polyethylene unit.

(GulfBase.com)

Ithraa partners with TRC to promote R&D – Ithraa has signed

a MoU with The Research Council (TRC) to drive investment

into Oman’s Research & Development (R&D) sector. Key to the

MoU is Rusayl-based Innovation Park Muscat (IPM), which is

slated to become an incubator for innovation and home to world-

class hi-tech companies. Ithraa through their extensive network

of international representatives, will help TRC to promote the

benefits and incentives offered by IPM to investment funds as

well as private R&D institutions. (GulfBase.com)

OOCEP’s Musandam Gas Plant to be operational by 4Q2014

– Oman Oil Company’s (OOC) subsidiary, Oman Oil Company

Exploration and Production (OOCEP), is planning to launch its

Musandam Gas Plant before the end of 2014. The project is

being developed with an investment of around $600 million at a

waterfront location in Tibat in Wilayat Bukha. Designed as an

integrated processing plant, the facility will process well fluids

from the existing Bukha field offshore platforms. The well fluids

will be transported from the platform to the Musandam Gas

Plant (MGP) through a newly-installed subsea pipeline where

they will be processed to produce sales quality gas, oil, LPG and

sulphur, according to OOCEP. At full capacity, the plant will

process 45mn standard cubic feet per barrels per day of crude

oil. A part of the project’s output of natural gas will be used as

fuel for the governorate’s first ever gas-based power plant

planned for implementation next door. Another offshore export

pipeline will transport sales gas from Musandam to Saqr Port in

Ras Al Khaimah. (GulfBase.com)

Oman Air signs heavy maintenance agreement with

JorAMCo – Oman has entered into an agreement with

JorAMCo to provide Omani national carrier with base

maintenance services for two Embraer 175 and three Airbus

A330 aircraft in its fleet. The maintenance checks are scheduled

to be carried out between May 2014 and November 2014. The

move continues a collaborative effort between the two

companies, with JorAMCo successfully carrying out similar

checks on two additional Oman Air Embraers in 2013.

(Bloomberg)

NBO’s profit jumps 22% to OMR23mn in 1H2014 – National

Bank of Oman (NBO) posted a net profit of OMR23mn in

1H2014 as compared to OMR18.8mn in 1H2013, reflecting an

increase of 22%. The bank’s total assets stood at OMR3.52bn at

the end of June 2014 as compared to OMR2.77bn a year

earlier. Loans & advances stood at OMR2.22bn at the end of

June 2014, 7% higher YoY, with customer deposits rising 34%

over the same period to OMR2.79bn. (MSM)

Tamkeen, BMI Bank extend partnership for Shari’ah-

compliant financing – Tamkeen and Al Salam Bank Bahrain’s

subsidiary, BMI Bank, have extended their partnership for

providing Shari’ah-compliant financing to local enterprises. This

marks the fourth contribution of BHD10mn by BMI Bank,

7. Page 7 of 8

expanding its portfolio to a total of BHD40m while the total value

of the scheme is BHD302mn. Initially launched in November

2010, the joint scheme offers SMEs including startups, a suite of

financial products at a competitive cost. Under the scheme,

which is run through several banks including BMI Bank,

Tamkeen guarantees 50% of the total financing amount and

subsidizes 50% of the profit payments due from customers.

Enterprises are eligible to receive financing ranging from

BHD10,000 to BHD500,000. The scheme features repayment

options of up to 10 years with a two-year grace period according

to finance procedures. (GulfBase.com)

Investcorp Bank redeems preference shares – Investcorp

Bank has redeemed 52,382 of the Investcorp Bank preference

shares for an aggregate redemption price of $52.382mn.

Investcorp Bank has also given notice to redeem a further

21,243 of the Investcorp Bank preference shares on August 12,

2014 for an aggregate redemption price of $21,243mn. (Bahrain

Bourse)

8. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 8 of 8

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

200.0

210.0

Jul-10 Jul-11 Jul-12 Jul-13 Jul-14

QE Index S&P Pan Arab S&P GCC

(0.1%)

0.8%

(0.8%)

0.7%

(0.3%)

0.3%

3.4%

(1.5%)

0.0%

1.5%

3.0%

4.5%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,294.07 (1.0) (3.3) 7.3 DJ Industrial 17,060.68 0.0 0.7 2.9

Silver/Ounce 20.69 (1.1) (3.5) 6.3 S&P 500 1,973.28 (0.2) 0.3 6.8

Crude Oil (Brent)/Barrel (FM

Future)

106.02 (0.9) (0.6) (4.3) NASDAQ 100 4,416.39 (0.5) 0.0 5.7

Natural Gas (Henry

Hub)/MMBtu

4.11 0.2 0.7 (5.3) STOXX 600 338.42 (0.4) 0.4 3.1

LPG Propane (Arab Gulf)/Ton 103.75 0.4 0.4 (18.0) DAX 9,719.41 (0.7) 0.5 1.8

LPG Butane (Arab Gulf)/Ton 123.00 (0.4) (0.4) (9.4) FTSE 100 6,710.45 (0.5) 0.3 (0.6)

Euro 1.36 (0.4) (0.3) (1.3) CAC 40 4,305.31 (1.0) (0.3) 0.2

Yen 101.68 0.1 0.4 (3.4) Nikkei 15,395.16 0.6 1.5 (5.5)

GBP 1.71 0.3 0.2 3.5 MSCI EM 1,066.35 0.3 0.7 6.3

CHF 1.12 (0.5) (0.4) (0.3) SHANGHAI SE Composite 2,070.36 0.2 1.1 (2.2)

AUD 0.94 (0.2) (0.2) 5.1 HANG SENG 23,459.96 0.5 1.0 0.7

USD Index 80.39 0.3 0.3 0.4 BSE SENSEX 25,228.65 0.9 0.8 19.2

RUB 34.39 0.2 0.5 4.6 Bovespa 55,973.61 0.4 2.2 8.7

BRL 0.45 (0.2) 0.1 6.5 RTS 1,352.15 (0.7) (2.2) (6.3)

188.2

153.6

139.2