Questions 16 through 20 are based on the following information. The.pdf

•

0 likes•2 views

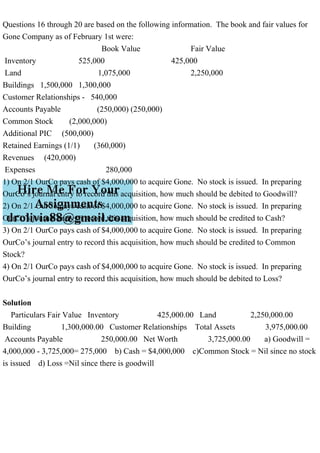

This document provides the book and fair values of assets and liabilities for Gone Company as of February 1. It also states that OurCo paid $4 million in cash to acquire Gone with no stock issued. To record the acquisition, OurCo would debit Goodwill for $275,000 (the difference between the $4 million cash paid and Gone's $3.725 million net worth). OurCo would also credit Cash for $4 million (the amount paid) and credit Common Stock for $0 since no stock was issued. No loss would be recorded.

Report

Share

Report

Share

Download to read offline

Recommended

Recommended

More Related Content

Similar to Questions 16 through 20 are based on the following information. The.pdf

Similar to Questions 16 through 20 are based on the following information. The.pdf (20)

4.(TCO E) During 20X3, Edwards Co. sold inventory to its paren.docx

4.(TCO E) During 20X3, Edwards Co. sold inventory to its paren.docx

Acc 401 advanced accounting week 11 quiz – final exam

Acc 401 advanced accounting week 11 quiz – final exam

Acc 401 advanced accounting week 11 quiz – final exam

Acc 401 advanced accounting week 11 quiz – final exam

Acc 401 advanced accounting week 11 quiz – final exam

Acc 401 advanced accounting week 11 quiz – final exam

Acc 401 advanced accounting week 11 quiz – final exam

Acc 401 advanced accounting week 11 quiz – final exam

Fred and George have been in partnership for many years. The partn.docx

Fred and George have been in partnership for many years. The partn.docx

More from suretheboss10

More from suretheboss10 (14)

R. Moore, Inc. assembles collections of records from the 1980s, secu.pdf

R. Moore, Inc. assembles collections of records from the 1980s, secu.pdf

Questions 11-15 are based on the followingRose Corporation acquir.pdf

Questions 11-15 are based on the followingRose Corporation acquir.pdf

Questions 1-2 go with the following information Terry Dactel is.pdf

Questions 1-2 go with the following information Terry Dactel is.pdf

QuestionGive one example for each of the three generations of cel.pdf

QuestionGive one example for each of the three generations of cel.pdf

QuestionDetails 13) Prove that a is an accumulation point of S if.pdf

QuestionDetails 13) Prove that a is an accumulation point of S if.pdf

QuestionBriefly explain why modulation is needed in wireless comm.pdf

QuestionBriefly explain why modulation is needed in wireless comm.pdf

Question1On January 1, 2014, Flip Company purchased 10,000 shares.pdf

Question1On January 1, 2014, Flip Company purchased 10,000 shares.pdf

Question-Whatare Fused Sentences How they can be avoidedQue.pdf

Question-Whatare Fused Sentences How they can be avoidedQue.pdf

Question1 30 pointsOn December 31, 2014, Flimsy Incorporated, h.pdf

Question1 30 pointsOn December 31, 2014, Flimsy Incorporated, h.pdf

Question is as follows, please show all steps of working. Le.pdf

Question is as follows, please show all steps of working. Le.pdf

Question In how many ways can 5 people be seated on 5 chairs around.pdf

Question In how many ways can 5 people be seated on 5 chairs around.pdf

Question Details lim x-2 (X^2 - 3) when finding delta i get to .pdf

Question Details lim x-2 (X^2 - 3) when finding delta i get to .pdf

Question 6Question textSelect onea. the company matched the e.pdf

Question 6Question textSelect onea. the company matched the e.pdf

Recently uploaded

https://app.box.com/s/x7vf0j7xaxl2hlczxm3ny497y4yto33i80 ĐỀ THI THỬ TUYỂN SINH TIẾNG ANH VÀO 10 SỞ GD – ĐT THÀNH PHỐ HỒ CHÍ MINH NĂ...

80 ĐỀ THI THỬ TUYỂN SINH TIẾNG ANH VÀO 10 SỞ GD – ĐT THÀNH PHỐ HỒ CHÍ MINH NĂ...Nguyen Thanh Tu Collection

Mehran University Newsletter is a Quarterly Publication from Public Relations OfficeMehran University Newsletter Vol-X, Issue-I, 2024

Mehran University Newsletter Vol-X, Issue-I, 2024Mehran University of Engineering & Technology, Jamshoro

https://app.box.com/s/7hlvjxjalkrik7fb082xx3jk7xd7liz3TỔNG ÔN TẬP THI VÀO LỚP 10 MÔN TIẾNG ANH NĂM HỌC 2023 - 2024 CÓ ĐÁP ÁN (NGỮ Â...

TỔNG ÔN TẬP THI VÀO LỚP 10 MÔN TIẾNG ANH NĂM HỌC 2023 - 2024 CÓ ĐÁP ÁN (NGỮ Â...Nguyen Thanh Tu Collection

Recently uploaded (20)

UGC NET Paper 1 Mathematical Reasoning & Aptitude.pdf

UGC NET Paper 1 Mathematical Reasoning & Aptitude.pdf

80 ĐỀ THI THỬ TUYỂN SINH TIẾNG ANH VÀO 10 SỞ GD – ĐT THÀNH PHỐ HỒ CHÍ MINH NĂ...

80 ĐỀ THI THỬ TUYỂN SINH TIẾNG ANH VÀO 10 SỞ GD – ĐT THÀNH PHỐ HỒ CHÍ MINH NĂ...

Kodo Millet PPT made by Ghanshyam bairwa college of Agriculture kumher bhara...

Kodo Millet PPT made by Ghanshyam bairwa college of Agriculture kumher bhara...

HMCS Vancouver Pre-Deployment Brief - May 2024 (Web Version).pptx

HMCS Vancouver Pre-Deployment Brief - May 2024 (Web Version).pptx

Jual Obat Aborsi Hongkong ( Asli No.1 ) 085657271886 Obat Penggugur Kandungan...

Jual Obat Aborsi Hongkong ( Asli No.1 ) 085657271886 Obat Penggugur Kandungan...

Beyond_Borders_Understanding_Anime_and_Manga_Fandom_A_Comprehensive_Audience_...

Beyond_Borders_Understanding_Anime_and_Manga_Fandom_A_Comprehensive_Audience_...

ICT role in 21st century education and it's challenges.

ICT role in 21st century education and it's challenges.

Food safety_Challenges food safety laboratories_.pdf

Food safety_Challenges food safety laboratories_.pdf

Interdisciplinary_Insights_Data_Collection_Methods.pptx

Interdisciplinary_Insights_Data_Collection_Methods.pptx

TỔNG ÔN TẬP THI VÀO LỚP 10 MÔN TIẾNG ANH NĂM HỌC 2023 - 2024 CÓ ĐÁP ÁN (NGỮ Â...

TỔNG ÔN TẬP THI VÀO LỚP 10 MÔN TIẾNG ANH NĂM HỌC 2023 - 2024 CÓ ĐÁP ÁN (NGỮ Â...

Sensory_Experience_and_Emotional_Resonance_in_Gabriel_Okaras_The_Piano_and_Th...

Sensory_Experience_and_Emotional_Resonance_in_Gabriel_Okaras_The_Piano_and_Th...

Questions 16 through 20 are based on the following information. The.pdf

- 1. Questions 16 through 20 are based on the following information. The book and fair values for Gone Company as of February 1st were: Book Value Fair Value Inventory 525,000 425,000 Land 1,075,000 2,250,000 Buildings 1,500,000 1,300,000 Customer Relationships - 540,000 Accounts Payable (250,000) (250,000) Common Stock (2,000,000) Additional PIC (500,000) Retained Earnings (1/1) (360,000) Revenues (420,000) Expenses 280,000 1) On 2/1 OurCo pays cash of $4,000,000 to acquire Gone. No stock is issued. In preparing OurCo’s journal entry to record this acquisition, how much should be debited to Goodwill? 2) On 2/1 OurCo pays cash of $4,000,000 to acquire Gone. No stock is issued. In preparing OurCo’s journal entry to record this acquisition, how much should be credited to Cash? 3) On 2/1 OurCo pays cash of $4,000,000 to acquire Gone. No stock is issued. In preparing OurCo’s journal entry to record this acquisition, how much should be credited to Common Stock? 4) On 2/1 OurCo pays cash of $4,000,000 to acquire Gone. No stock is issued. In preparing OurCo’s journal entry to record this acquisition, how much should be debited to Loss? Solution Particulars Fair Value Inventory 425,000.00 Land 2,250,000.00 Building 1,300,000.00 Customer Relationships Total Assets 3,975,000.00 Accounts Payable 250,000.00 Net Worth 3,725,000.00 a) Goodwill = 4,000,000 - 3,725,000= 275,000 b) Cash = $4,000,000 c)Common Stock = Nil since no stock is issued d) Loss =Nil since there is goodwill