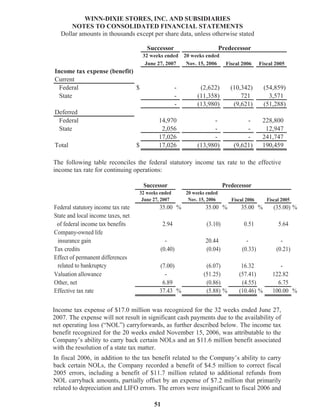

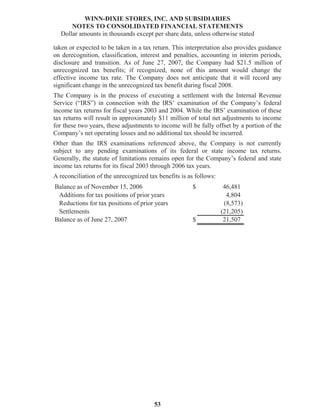

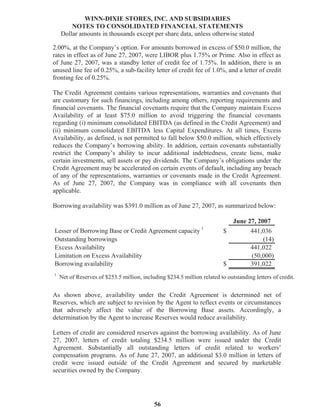

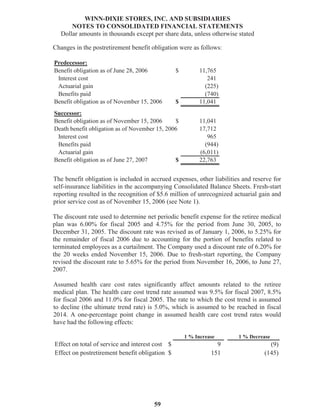

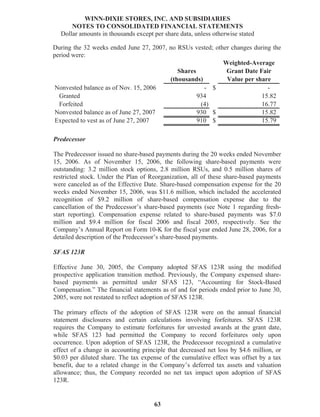

Download to read offline

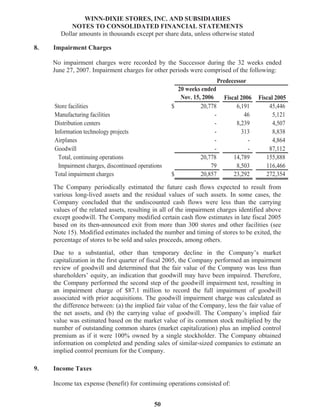

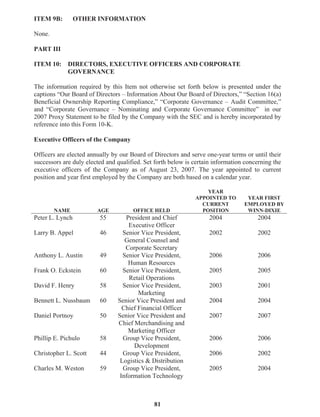

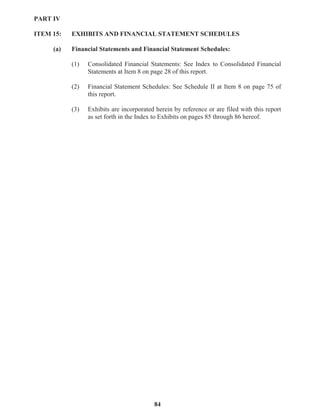

This document is the 2007 Annual Report of Winn-Dixie Stores, Inc. It provides information on the board of directors as of June 27, 2007 and contact information for investor inquiries. It also includes a letter from Peter Lynch, President, CEO, and Chairman, discussing Winn-Dixie's financial highlights for fiscal year 2007 and their multi-year turnaround plan focusing on rebuilding their brand, investing in store remodels, neighborhood marketing, associate training, and achieving profitable sales.