Download to read offline

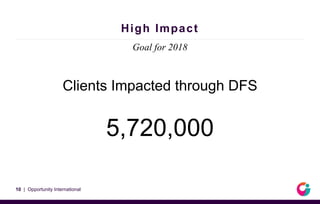

The document discusses the importance of digital financial services (DFS) for enhancing access to formal financial services among underserved populations, particularly in sub-Saharan Africa. It highlights the advantages of DFS, including increased customer convenience and outreach to rural areas, and outlines Opportunity International's focus on leveraging technology, improving customer interactions, and expanding services, especially for women. The organization aims to impact 5.72 million clients through DFS by 2018, with plans for future growth in Asia.