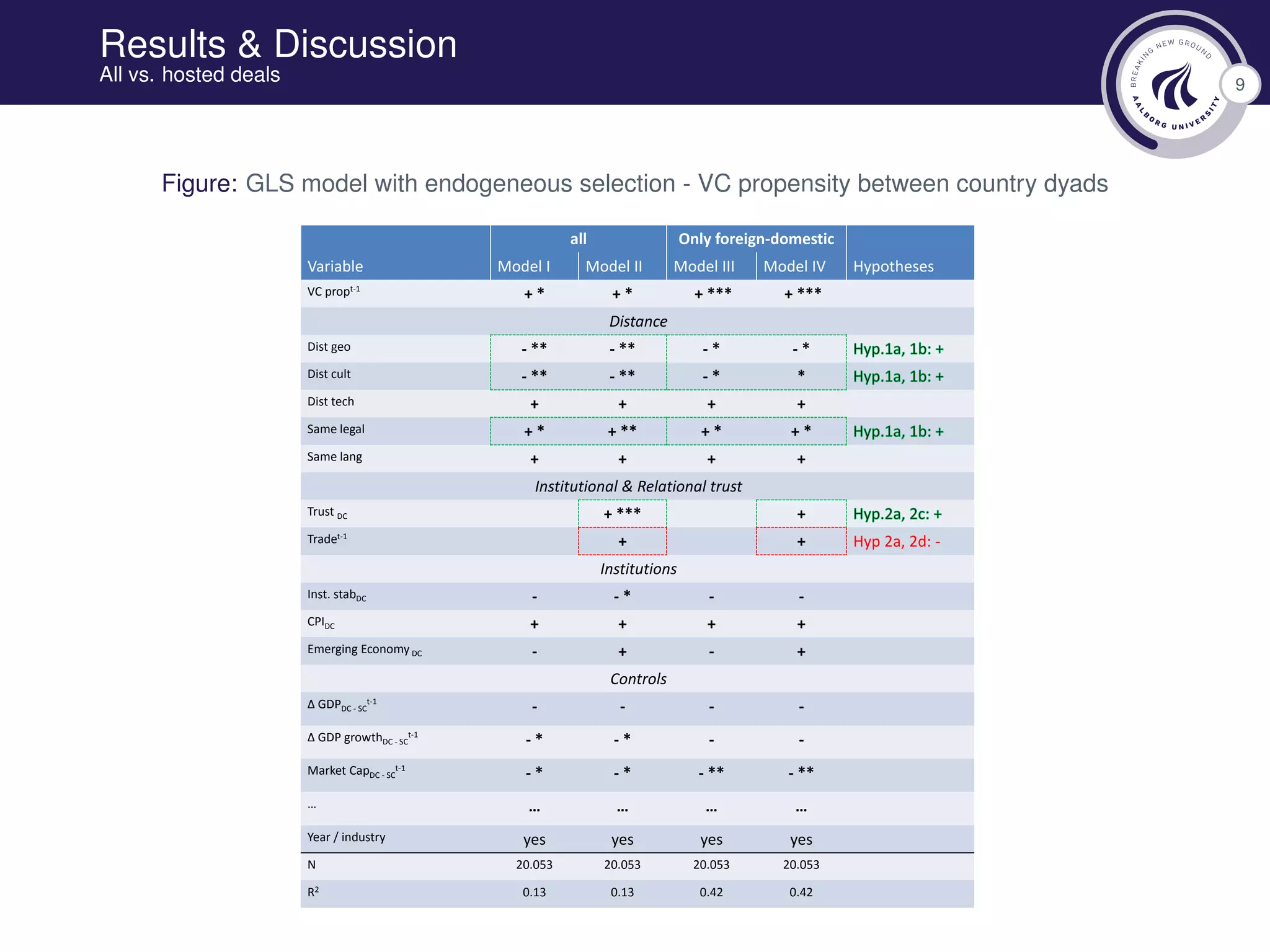

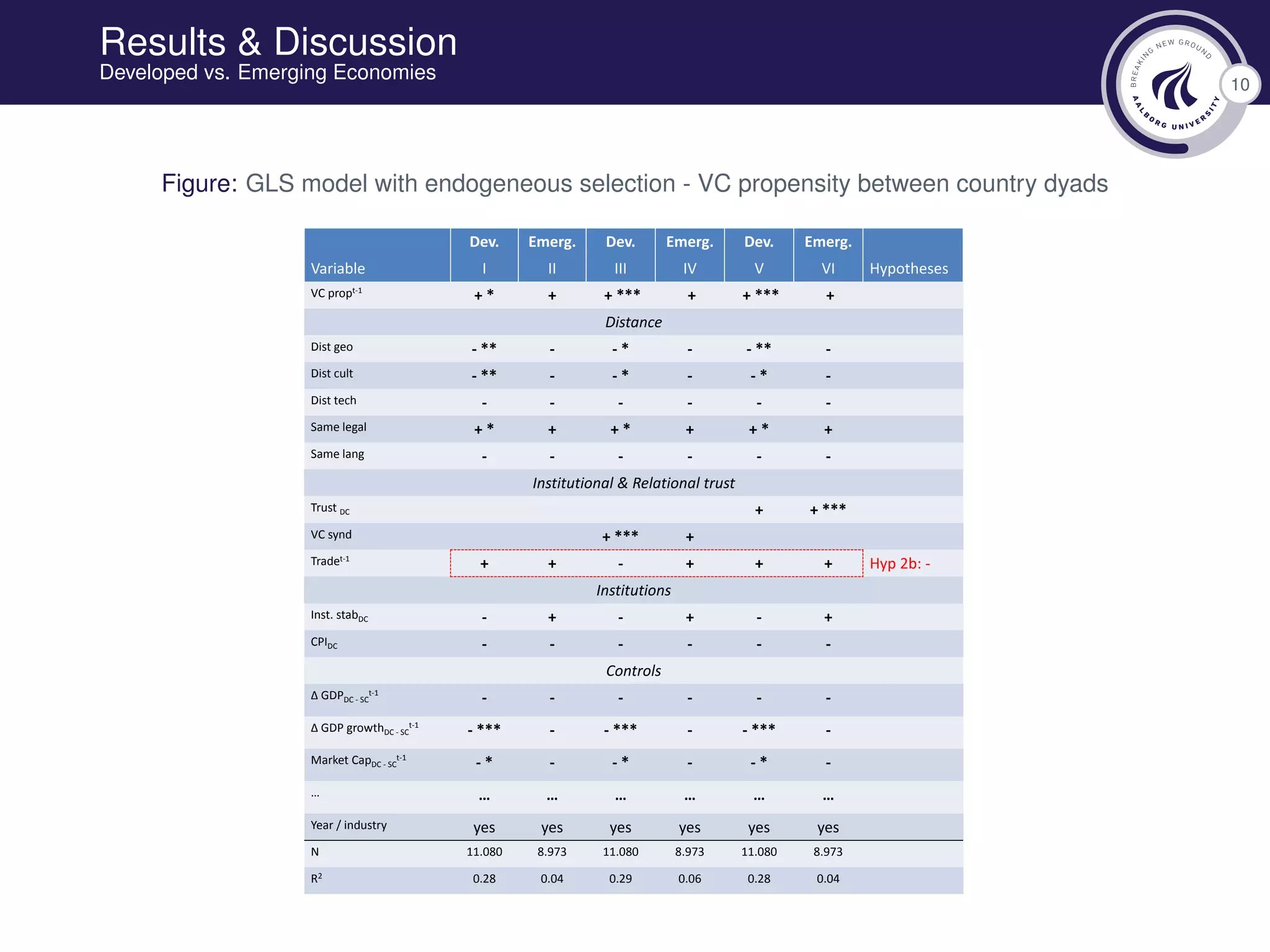

- The document discusses cross-border venture capital syndication between countries.

- It presents hypotheses that geographical, cultural, and institutional distance negatively impact cross-border investments, but this effect is lessened when investments are syndicated with a domestic venture capitalist.

- Institutional and relational trust are hypothesized to positively influence investments by diminishing the negative effects of distance, especially for emerging economies.

![[TOUCH] The Original Undeniable Charismatic Homme](https://cdn.slidesharecdn.com/ss_thumbnails/touch-140603114803-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)