Download to read offline

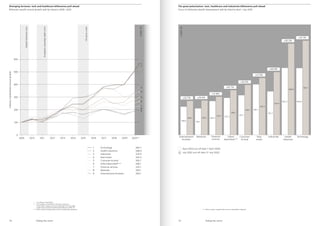

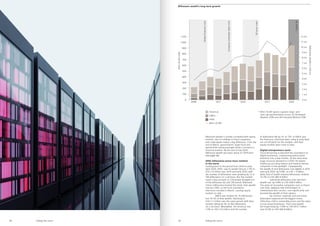

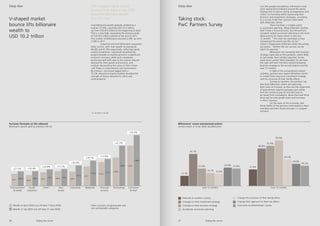

The report examines the impact of the COVID-19 pandemic on billionaires, revealing a significant polarization in their wealth, with innovators in technology and healthcare thriving while others lag. As of July 2020, total billionaire wealth reached a record $10.2 trillion, driven by a surge in tech and healthcare sectors, alongside increased philanthropic efforts during the pandemic. The document highlights a shift towards innovation and a new generation of entrepreneurs poised to reshape the economy through emerging technologies.