This document discusses the results of a Corporate Governance Scorecard initiative for commercial and universal banks in the Philippines.

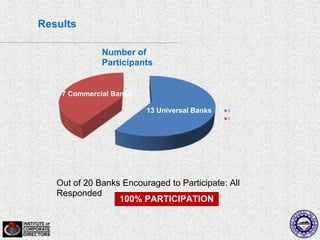

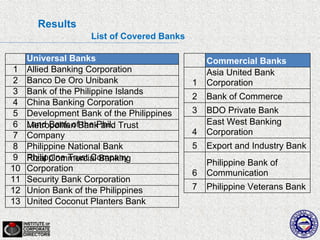

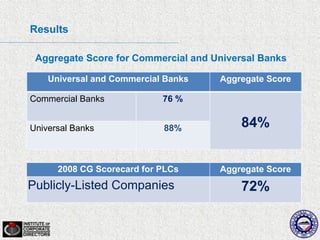

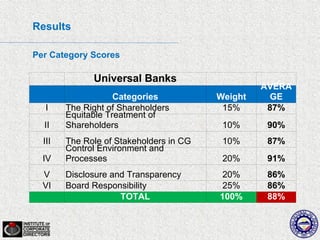

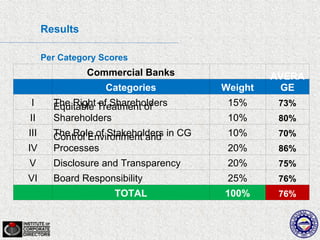

1) Twenty total banks participated, including 7 commercial banks and 13 universal banks. Universal banks scored higher on average, with a score of 88% compared to 76% for commercial banks.

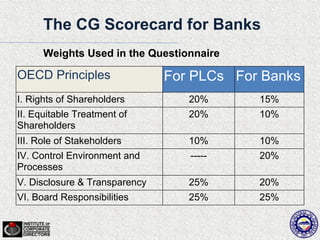

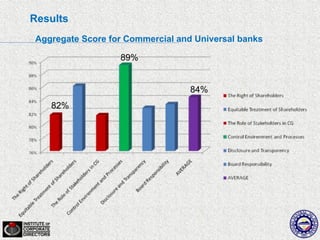

2) Scores were calculated based on categories related to shareholders' rights, treatment of stakeholders, control environment, disclosure and transparency, and board responsibilities. Universal banks scored highest in control environment and processes.

3) The results provide benchmark averages that individual banks can use for comparison, with the recommendation that banks be given time to improve their corporate governance practices and compliance based on the scorecard.