English - 5 - Strategic benchmarking in the supply chain triangle.

TIME INCORPORATED

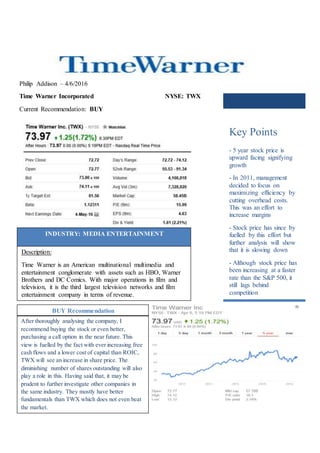

1. Philip Addison – 4/6/2016

Time Warner Incorporated NYSE: TWX

Current Recommendation: BUY

INDUSTRY: MEDIA ENTERTAINMENT

Description:

Time Warner is an American multinational multimedia and

entertainment conglomerate with assets such as HBO, Warner

Brothers and DC Comics. With major operations in film and

television, it is the third largest television networks and film

entertainment company in terms of revenue.

BUY Recommendation

After thoroughly analysing the company, I

recommend buying the stock or even better,

purchasing a call option in the near future. This

view is fuelled by the fact with ever increasing free

cash flows and a lower cost of capital than ROIC,

TWX will see an increase in share price. The

diminishing number of shares outstanding will also

play a role in this. Having said that, it may be

prudent to further investigate other companies in

the same industry. They mostly have better

fundamentals than TWX which does not even beat

the market.

Key Points

- 5 year stock price is

upward facing signifying

growth

- In 2011, management

decided to focus on

maximizing efficiency by

cutting overhead costs.

This was an effort to

increase margins

- Stock price has since by

fuelled by this effort but

further analysis will show

that it is slowing down

- Although stock price has

been increasing at a faster

rate than the S&P 500, it

still lags behind

competition

2. Financial Management

The horizontal trend

analysis (2011-2015) shows

a bit of a hit and miss

approach to Time Warner’s

finances for the period.

Although management was

meeting their goal of

increasing margins, 2014

took a big hit and the

company has still not seen

2011 revenue numbers. The

table below shows that in

all but one of the years,

Gross Income has grown. Sales growth also shows a positive

correlation with COGS growth.

Technical Analysis

Vertical trend

analysisforthe

past 10 shows how

Time Warner has

gradually

decreasedits

proportionof

intangible assetsas

well asitsNetPPE,

whilstincreasingits

OtherLong Term

Assetsand

Accounts

Receivables.

Evidence also

pointstowardsthe greaterreliance of debtuse inthe firmas Total Liabilities encompassagreaterportionof the

balance sheet.

Time Warner has faced a tumultuous time in the past five years. After

reaching an all-time 5 year high revenue of 29.8 billion in FY2013,

FY2016 is still trying to recover from the losses suffered in FY2014 and

FY2015. Stock price has gradually increased over the past five years at a

pace quicker than the S&P 500 as shown on page 5. The 5 day moving

average and average number of shares traded indicates that whilst TWX

might be stable in the midterm, it will increase in the long run.

3. ROA & ROE

Since the recession in 2008,

ROE has been steadily

increasing albeit at a slower

rate than the market.

ROE reached an all-time

high of 16.23% due to the

decreasing amount of

shareholders equity and the

increasing amount of net

income attributable to them.

In comparison to its

competitors, Time Warner

boasts the third highest ROA

numbers at 6% behind Walt

Disney’s 9.51% and

Twentieth Century Fox’s

16.6%

Since the recession, Time

Warner has always posted

gradual increases in its ROA

with the 4 other major

competitors all posting losses

at some stage.

Risk Analysis

TWX operates in a highly

competitive, consumer driven and

rapidly changing environment. As

reported in the fundamental

analysis, macroeconomic factors

can greatly affect firm and

industry performance. With the

advent of the internet of things,

more and more consumers are

switching from traditional cable

based viewing systems to a more

online medium. Furthermore, with

a high proportion of assets being

intangible, management is

expecting to incur significant

legal fees involving resolution,

defence and creation of IP.

Price to Earnings (P/E)

When compared to the

industry, Time Warner has

had an inferior price to

earnings ratio in each of the

past 10 years as shown in

Exhibit 4.3.

A negative EPS of -11.21

during the crisis of 2008

meant that there was no P/E

ratio for that year.

As share price has increased,

so too has Earnings per

share. This can be attributed

to the diminishing number of

shares outstanding in the

market as shown in Exhibit

4.1. EPS has increased in

each of the past 7 years with

the P/E ratio declining three

times in 2011, 2013 and

2015.

Compared to its 4 major

competitors, Time Warner

has the second worst P/E

ratio with investors willing to

pay $13.74 for every dollar

as shown in Exhibit 4.2

Time Warner Inc

Comcast Corp

Time Warner Cable Inc

Walt Disney Co

Twenty-First Century Fox Inc

Price to Book Value (P/BV)

Time Warner has the lowest

P/BV of any of its 4 major

competitors with investors

only willing to pay a 2.23

premium as opposed to Time

Warner Cable Inc’s 5.83, as

shown in Exhibit 3.2.

Although Time Warner has

increased its price to book

value ratio consistently after

2008, it has however, lagged

behind the industry in each

of those years as shown in

Exhibit 3.3.

4. $0

$1,000,000,000

$2,000,000,000

$3,000,000,000

$4,000,000,000

$5,000,000,000

$6,000,000,000

$7,000,000,000

2016 2017 2018 2019 2020

Future Free Cash Flow for TWX

FCF

Current

Month

Last

Month

Two

Months

Ago

Three

Months

Ago

Strong Buy 8 8 8 8

Buy 20 20 18 18

Hold 10 10 10 10

Underperfo

rm

0 0 0 0

Sell 0 0 0 0

Recommendation Trends

Company Valuation

At present, Time Warner is undervalued relative

to its intrinsic stock price value. The company

valuation was fuelled by assumptions that I

made in part to reflect how past performance

can have an impact on future performance. This

why I chose a growth rate constant of 4.57% in

revenue as that was the 5 year average. With an

increasing free cash flow, Time Warner will

gradually start to see financial numbers it had

before the recession. With a cost of capital that

is less than its ROIC,Time Warner can expect

to see an increase in its stock price over the

coming years. Exhibit (?) shows further details

on how the valuation process was carried out.

Upgrades & Downgrades History

Analyst Opinion

Common consensus

amongst brokers is that

Time Warner is expected

to appreciate in value over

the coming years.

Moreover, 2 brokers

expect it to outperform

relative to the market

although neither one has

stated whether it expects

them to outperform their

industry peers. Given the

fundamental analysis

however, this would seem unlikely.

Figure 1.1 shows how optimistic people are about TWX.

Date ResearchFirm Action From To

Feb 5, 2016 Telsey Advisory Group Initiated Outperform

Jan 14, 2016 Drexel Hamilton Initiated Buy

Nov 5, 2015 CreditAgricole Downgrade Buy Outperform

Nov 5, 2015 BofA/Merrill Downgrade Buy Neutral

Nov 5, 2015 Wells Fargo Downgrade Outperform Market Perform

Oct 20, 2015 Pivotal Research Group Initiated Buy

Aug 20, 2015 Bernstein Downgrade Outperform Mkt Perform

Apr 28, 2015 CreditAgricole Initiated Buy

Mar 5, 2015 Deutsche Bank Initiated Buy

Jan 16, 2015 Stifel Downgrade Buy Hold