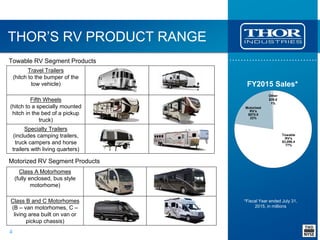

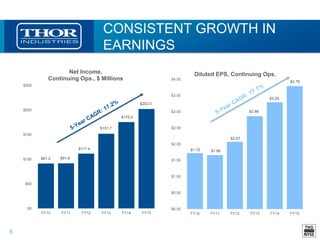

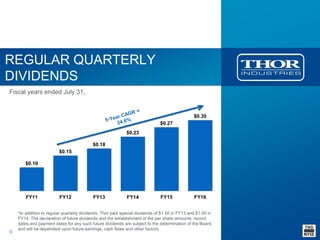

Thor Industries is one of the world's largest manufacturers of recreational vehicles. It has two main business segments: towable RVs such as travel trailers and fifth wheels, and motorized RVs including Class A, B, and C motorhomes. Thor has experienced consistent sales growth and increasing profits and earnings per share over the past decade. It aims to provide superior RV products through innovation while maintaining strong relationships with consumers, dealers, and suppliers for long-term sustainable growth.