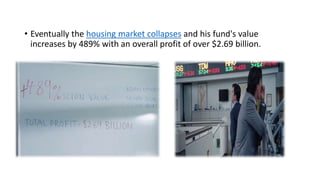

Christian Bale plays eccentric hedge fund manager Michael Burry who anticipates the collapse of the US housing market in 2007 due to unstable subprime loans. He creates a market for credit default swaps to bet over $1 billion against mortgage-backed securities. Though clients are unhappy with costs, Burry refuses to back down. He discovers banks manipulated ratings to offload losing bonds. When the market crashes as predicted, Burry's fund profits over $2 billion despite initially restricting withdrawals amid client anger.