Project Management Challenges in an Effluent Treatment Plant Construction

The Indian Ferroalloy Industry At Cross Roads

1. The Indian Ferro Alloy Industry At Cross Roads

Invited Paper

The Indian Ferro Alloy Industry At Cross Roads

Prabhash Gokarn, Tata Steel

1.0 INTRODUCTION TO THE INDIAN FERRO ALLOY INDUSTRY

The Indian Ferro Alloy Industry; a part of the Core Sector under Ministry of Steel; is

engaged in supplying crucial intermediates to the Steel Industry; namely ferroalloys.

The Industry has completed five decades of its existence.

Bulk Ferroalloys (viz. Ferro Manganese, Ferro Silico Manganese, Ferro Silicon, Ferro

Chrome, etc., manufactured through Submerged Arc furnaces), and Noble Ferroalloys

(viz. Ferro Molybdenum, Ferro Vanadium, Ferro Tungsten, Ferro Silico Magnesium,

Ferro Titanium, Ferro Boron, etc. manufactured through the Alumino-Thermic process),

are used in the production of steel (as deoxidants, for refining and for alloying).

Depending upon the process of steel making and the type of steel being made, the

requirement of different ferroalloys varies widely. The principal functions of alloying

steel is for increasing its resistance to corrosion and oxidation, improving hardenability,

tensile strength, high temperature properties (such as creep strength), wear and

abrasion resistance, etc. Since noble ferroalloys

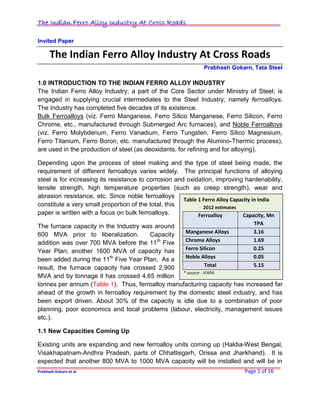

Table 1 Ferro Alloy Capacity in India

constitute a very small proportion of the total, this 2012 estimates

paper is written with a focus on bulk ferroalloys. Ferroalloy Capacity, Mn

TPA

The furnace capacity in the Industry was around

Manganese Alloys 3.16

600 MVA prior to liberalization. Capacity

addition was over 700 MVA before the 11th Five Chrome Alloys 1.69

Year Plan; another 1600 MVA of capacity has Ferro Silicon 0.25

been added during the 11th Five Year Plan. As a Noble Alloys 0.05

result, the furnace capacity has crossed 2,900 Total 5.15

* source - IFAPA

MVA and by tonnage it has crossed 4.65 million

tonnes per annum (Table 1). Thus, ferroalloy manufacturing capacity has increased far

ahead of the growth in ferroalloy requirement by the domestic steel industry, and has

been export driven. About 30% of the capacity is idle due to a combination of poor

planning, poor economics and local problems (labour, electricity, management issues

etc.).

1.1 New Capacities Coming Up

Existing units are expanding and new ferroalloy units coming up (Haldia-West Bengal,

Visakhapatnam-Andhra Pradesh, parts of Chhattisgarh, Orissa and Jharkhand). It is

expected that another 800 MVA to 1000 MVA capacity will be installed and will be in

Prabhash Gokarn et al. Page 1 of 16

2. The Indian Ferro Alloy Industry At Cross Roads

commercial production in the next two to three years. These units are also setting new

capacities for electricity generation and it is expected that about 1000 MVA of CPP

capacity will be added in next two years.

2.0 GLOBAL TRENDS IMPACTING THE INDIAN FERRO ALLOY INDUSTRY

2.1 Global Shift in Stainless Steel and Carbon Steel Production

2.1.1 Stainless Steel production has seen shift

in production from EU and Japan to China. There

has been a steep reduction in stainless steel

production in EU (due to the economic crisis) and

in Japan(partly due to effects of the Tsunami and

due to global recession). This reduction in

stainless steel production in the developed

economies is likely to continue. (Figure 2)

On the other hand stainless steel production in

China and India has seen significant growth: with

over 45% of global stainless steel likely to be

produced in China by 2015 as against 35% today;

India is also likely to see a growth in stainless steel production at ~ 7% in the next 5

years.

2.1.2 Carbon Steel production in China has grown at a CAGR of 12% and in India at

8% since early 2000 and this growth is not

likely to taper off anytime soon. On the other

hand the developed economies of Japan, US,

and EU grew in single digits in the same

period and are now declining. (Figure 3)

Thus the demand for ferroalloys too has

become Asia Centric. Given both China and

India are also large producers of ferroalloys

(China & India - FeCr, Mn alloys, additionally,

China – FeSi, refined alloys and most noble

ferroalloys), and are large exporters to the

rest of the world; the growing consumption at

home has very significant impact on global

Prabhash Gokarn et al. Page 2 of 16

3. The Indian Ferro Alloy Industry At Cross Roads

trade. China has imposed export taxes on ferroalloy exports and has in many cases

become a net importer; India seems to be going the same way.

2.2 Borderless World

2.2.1 Trade Barriers : Globally, trade barriers to imports are decreasing, for example

the decrease on duties on ferro alloy imports has reduced from a peak of 105% in 1993

to 0% in 2008 with duties currently just 5% (Figure 4)

Source : IFAPA

2.2.2 Ocean Freight : With development of shipping infrastructure, ocean freight no

longer remains a significant cost, a step towards making geography, history (Figure 5)

Source : ICDA Kyoto Conference

Prabhash Gokarn et al. Page 3 of 16

4. The Indian Ferro Alloy Industry At Cross Roads

2.3 Reducing Differential in Power Situation in Major Ferroalloy Producing

Countries :

Power is the second most important requirement for bulk ferroalloy production. India

has historically suffered from huge power shortages, inefficient power generation &

transmission and high cost, partly due to cross subsidies and T&D losses (which include

power theft). However, privatization of power generation (both CPPs & IPPs) and power

distribution has brought significant improvement in the Indian power situation in the last

decade.

While India is still at a disadvantage with respect to power cost in South Africa and

Kazakhstan, the gap between China and South Africa on the one hand and India on the

other regarding cost of power and its availability has clearly reduced, making ferroalloy

production in India much more sustainable. The power crisis in South Africa is well

known, while China too has seen acute seasonal shortages of power and rising power

costs.

3.0 OPPORTUNITIES FOR GROWTH OF THE FERRO ALLOY INDUSTRY IN INDIA

The above factors have given the Indian Ferro Alloy Industry immense and very

significant growth opportunities that have led to a very rapid growth in ferro alloy

production and exports in the last decade. (Figure 6).

Source : IFAPA

3.1 Exports from India : China is the world’s largest Manganese Ore producer by

volume and by Manganese content producing 35% of the world’s total production. China

has traditionally been a large exporter of Manganese Alloys.

Prabhash Gokarn et al. Page 4 of 16

5. The Indian Ferro Alloy Industry At Cross Roads

Since late 2009, China has become a net importer of SiMn. Ironically, it was China that

in the past exported the highest volume of SiMn. Also, the steep increase in the

production of stainless steel and carbon steel in China (Figures 2 and 3) means it has

become a significant market for ferroalloys, located at India’s doorstep.

China’s withdrawal from supplying bulk ferro alloys and instead importing them on a

large scale has led to a steep increase in Indian exports of ferro alloys. (Figure 7).

Source IFAPA

Prabhash Gokarn et al. Page 5 of 16

6. The Indian Ferro Alloy Industry At Cross Roads

3.2 Domestic Consumption of Ferroalloys : The increase in production of both

carbon and stainless steel in India over the last decade has led to a significant increase

in the domestic consumption of Ferroalloys in India (Figure 8)

Source IFAPA

The projected growth of over 8% of stainless steel and carbon steel till 2015 augurs well

for the continued growth of ferro alloy production in India (Figure 9A and 9B).

Source : IFAPA 5 year document

Prabhash Gokarn et al. Page 6 of 16

7. The Indian Ferro Alloy Industry At Cross Roads

Source : IFAPA 5 year document

4,0 FERROALLOY INDUSTRY IN INDIA - ADVANTAGES

To summarize, the Indian Ferro Alloy industry has many advantages that have so far

augured well and resulted in the spectacular growth of ferro alloy production in India.

These advantages are :

4.1 Ability to immediately scale up :

1. Large Capacity for Ferroalloys

2. Industry currently operating at 60% of rated capacity

3. New capacities coming up - near ports (Vizag, Haldia).

4.2 Location near high growth regions:

4. Freight advantage in markets such as China, Korea and Japan compared

to Ukraine, Kazakhstan and South Africa

5. Short sailing time, freight advantage

4.3 Cost Advantages over China:

6. Domestically sourced LG & MG Mn Ore available for blending with

imported HG Mn Ore.

7. Power, labour and inland freight costs comparable to China.

4.4 Power availability no longer such a large differentiator:

8. Commissioning of many new power plants including captive ones(CPP)-

may help reduce power availability issues (faced today by SA, China)

(Figure 12)

Prabhash Gokarn et al. Page 7 of 16

8. The Indian Ferro Alloy Industry At Cross Roads

4.5 Backward linkage to Ore:

9. Chrome Ore - Indigenous Chrome ore of high grade quality available to

some players (integrated players like IMFA & Tata Steel, and those based

in Orissa with allocations from OMC)

10. Manganese Ore – Low and medium grade Manganese ores abundantly

available but need to be sweetened by import of high grade/high Mn/Fe

Manganese ores.

4.6 Reductants :

11. Coke : India has been almost totally reliant on imports of coke from China

specially for making Ferro Chrome. High coke prices and the 40% export

tax levied on coke exports by the Chinese government have reduced the

cost competitiveness of the ferro alloy industry in India.

Increasing use of alternative reductants including indigenous coke/coal for

ferro alloy making has helped the industry to mitigate the high cost to

some extent. The slowing GDP growth in China and the global recession

have prompted the Chinese government to withdraw this tax, which will

further help the Indian industry to grow.

4.7 Rising domestic consumption of ferroalloys :

The projected ~8% growth in carbon steel and ~10% growth in stainless

steel production augurs well for the ferroalloy industry in India.

5.0 THEN WHY IS THE INDIAN FERRO ALLOY INDUSTRY AT THE

CROSS ROADS ?

There are however significant developments that can either derail the Indian ferro alloy

growth story or propel it to greater heights. These developments are :

1. Increasing restrictions in the availability of the key raw materials – i.e.

Manganese and Chrome Ores

India has been self sufficient in both Manganese and Chrome Ore and till

recently was even a very significant exporter.

Prabhash Gokarn et al. Page 8 of 16

9. The Indian Ferro Alloy Industry At Cross Roads

However, because of a deficiency in lumpy chrome ore and restrictions in the

free availability of friable chrome ore due to internal policies of the largest

supplier (OMC); imports of chrome ore into India are rising rapidly.

High Grade Manganese ore being in short supply, imports of Manganese ore into

India have risen dramatically. Manganese ore imports into India are at 1.6 Mn

tonnes for Jan-Aug 2012, a rise of 78% from the same period in 2011.

(Figure 10)

Source : IMnI, own estimates

India, like China, is highly dependent on South Africa, Gabon, Australia and

Brazil for sourcing of Manganese ore; these four countries account for ~ 90% of

the imports in 2011.

What is worrying is China’s use of its financial muscle to buy mining assets and

securing exclusive tie ups that may make sourcing of ores costlier for India and

hamper the growth of ferro alloy production.

2. Electricity As explained

earlier, with the increase

in generation of

electricity by public

sector utilities, IPPs

(Independent Power

Projects) and

CPPs(Captive Power

Plants); Power

Shortages which were

Prabhash Gokarn et al. Page 9 of 16

Source : Data Monitor

10. The Indian Ferro Alloy Industry At Cross Roads

the bugbear of power intensive industries in India such as the ferro alloy industry

were mitigated to a large extent and that allowed for the spectacular growth of

this sector(Figure 12).

However, there is likely

to be an impending

power crisis in this

country due to thermal

coal availability issues,

coal linkage issues;

delay in startup of new

coal mines and de-

allocation of coal blocks

due to the “Coal-gate”

scam. The rising cost of

thermal coal globally and

restrictions imposed in Indonesia on thermal coal asset ownership and

preferential allocation agreements too have been affecting the growth of the

power sector.

3. Infrastructure Indian industry has had to grapple with inadequate and crumbling

infrastructure – stretched

and overburdened

roadways, railways and

ports - that raises the

cost of business.

However we are seeing a

rapid improvement in

infrastructure :

a. Roads - India

plans to spend

approximately

Source : Data Monitor

US$70 Billion by

2013 to modernize its roads. India has rebuilt over 18,300 kilometers of 4

or 6-lane highways(including the 4-lane Golden Quadrilateral) inter-

connecting major manufacturing centers and ports. The country is adding

~11 kilometers of new highways daily, and it is likely that we would add

about 600 kilometers of modern highway per month till 2014.

Prabhash Gokarn et al. Page 10 of 16

11. The Indian Ferro Alloy Industry At Cross Roads

b. Railways - India has one of the world's largest railway networks

comprising 115,000 km of track over 65,000 km carrying 2.8 million tons of

freight daily. Despite this the rail network is stretched and requires urgent

expansion and modernization. Improvements in the form of “own your own

wagon”, freight rationalization etc have helped.

c. Sea Ports - India has a long 7500km coastline in which there are 13 major

ports and 187 smaller ports, handling about 560 million tonnes of cargo

(which is growing at a rate of 7.7%) annually. While many major ports are

stretched to capacity, specially Paradip, Vishakapatnam and Haldia, which

handle most of the ferroalloy traffic; upcoming ports like Dhamra in the

east; Pipavav, Adani, Dahej, Mundra and Hazira in the west and

Vallaradam in the south would help reduce traffic congestion.

These improvements in infrastructure will help in the further growth of the

ferroalloy industry. The concern is that these improvements will not happen

rapidly enough.

4. Capital – Lack of capital and high rates of interest on loans have in many ways

stymied the growth of ferroalloy units in the past. With many units having fallen

sick due to poor project planning, execution and economics, Indian banks have

become wary of exposure to this sector.

Like in other sectors, there is increasing foreign investor interest in the ferroalloy

sector. This has come in terms of both investments through the stock exchanges

in listed entities (FIIs) and more recently, in form of direct investments through

JVs (FDI). This increased availability of finance for well planned projects could

result in further rapid expansion of the ferroalloy industry. However, talks of

lowering India’s Credit Rating due to the slow pace of reforms, the negative

sentiments caused by issues such as debate over FDI in Retail and the feeling of

Government inaction could badly affect availability of foreign funds.

5. Lack of Technology Infusion and Innovation While Indians have been past

masters of local innovations (jugaad – Figure 13), systematic industrial research,

(that allowed the US, Japan, the former Soviet Union, South Korea and some

countries in the EU to leapfrog in industry led GDP growth) is severely lacking in

India.

Prabhash Gokarn et al. Page 11 of 16

12. The Indian Ferro Alloy Industry At Cross Roads

Source : TQMS

As a result India risks being continually overshadowed by China and significant

development of new technologies in ferroalloy making bypassing the Indian

ferroalloy industry (Figure 14).

Figure 14 : Some New Technologies in Ferroalloy Making

Source : Metal Junction Conference, 2011

6. Markets – The rapid growth in exports of ferroalloys (Figure 7) led to rapid

growth in ferroalloy production in India(Figure 6) and today exports form a

substantial proportion(~50%) of the market for ferroalloys (Figure 15). Ferroalloys

Prabhash Gokarn et al. Page 12 of 16

13. The Indian Ferro Alloy Industry At Cross Roads

from India were exported to EU, Japan and South Korea. The first exports of

ferroalloys to China (hitherto a major ferroalloy exporter) from India occurred in

2004.

Figure 15 : Rising Proportion of Exports (kT)

47%

52%

32%

1,533

38% 40%

1,555

30%

863

961

28%

960

640

517

1,819

1,740

1,558

1,520

1,460

1,424

1,308

2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12

Dom Exp, %Exp

Source : IFAPA

The shift in steel production from the developed nations to China (Figures 2 and

3) has led to China becoming the largest consumer (and in some cases

producer) of ferroalloys. Thus, till recently, China has been the dominant

destination for ferroalloys from India. With slowing Chinese steel growth and a

healthy growth in demand for ferroalloys domestically, it is likely that exports,

currently almost 50% of total production, will fall to a level of 30-35%(level

attained during 2005-08) in 2013. The two factors of concern are :

a) With reduction in export duties in China, the re-emergence of China as a large

exporter of ferroalloys may make it difficult for Indian ferroalloy players to

retain market share in a shrinking global market and

b) The domestic demand for ferroalloys, although growing, will not be able to

take up the slack if exports are hit.

This would mean that the bulk ferroalloy industry could see a period of de-growth

in the short term.

Prabhash Gokarn et al. Page 13 of 16

14. The Indian Ferro Alloy Industry At Cross Roads

Source : IFAPA

7. Rising Ferro Alloy Imports into India

Although India is a large exporter of Ferroalloys due to the uncertain economic

condition in the developed world, many ferro alloy companies (mainly from the

CIS, Russia and Kazakhstan) which restricted themselves to supplying to

customers in the developed world(US, EU, Japan) and to China have started

making in-roads into India.

This has led to a steep rise in imports of ferroalloys (25% CAGR over last 5

years) and does not augur well for the Indian Ferro Alloy industry (Figure 11).

6.0 CONCLUSION

Thus while there are many positives for the ferroalloy industry in India, viz. scalability,

location near high growth markets, cost advantages of labour, technical manpower

domestically available ore and reducing price of reductant blend; the growth in ferroalloy

production is stymied by inadequate infrastructure, rising cost & availability issues in

thermal coal, fear of getting saddled with old technology, and lack of capital. The global

slowing of demand for ferroalloys, the re-emergence of China as a major exporter and

the threat of imports are other factors that the Indian ferroalloy industry would need to

tackle.

Therefore it is very difficult to predict if the ferroalloy industry in India can repeat the

spectacular double digit growth of the last five years. The only certainty is of ferroalloy

prices; which have been volatile and unpredictable in the past – they will remain volatile

and unpredictable in the future: some things will never change!!

Prabhash Gokarn et al. Page 14 of 16

15. The Indian Ferro Alloy Industry At Cross Roads

Acknowledgements

The author (Prabhash Gokarn) would like to thank the management of Tata Steel

for allowing him to write this paper. The views expressed in this paper are his own

and should not be construed as the official opinion of Tata Steel or the prevalent

views within the company.

References & Sources of Data

1. Indian Ferro Alloy Producer’s Association : Annual Reports & Presentations

2. International Manganese Institute and International Chromium Development

Association : Reports & Conference Presentations

3. CRU, Metal Bulletin & TEX Publications : NiCrMo, Bulk FAM, Ferroalloys Market

Track, Tex Report

4. Data Monitor : Trends & Developments in the Indian Power Market (May’10)

5. Prayas Energy Group : Overview of Indian Energy Trends (2009)

6. Tata Quality Management Service Publication on Innovation (2011)

7. Metal Junction Conference : Indian Steel 2011 (Nov’11)

8. iMaritime : India Port Report (Aug’03)

9. Wikipedia and other sources on the internet.

Abbreviations

Fe – Ferro, c/lb – US cents per pound of GDP – Gross Domestic

Mn – Manganese, Chrome Content, Product,

Si – Silicon, LG - low grade, CIS – Confederation of

Cr – Chrome, MG – medium grade, Independent States,

Ch – Charge HG – high grade, US – United States,

MVA – Million Volt Ampere, T&D – Transmission & CAGR – Compounded Annual

MT – Metric Tons, Distribution, Growth Rate,

IPP – Independent Power OMC – Orissa Mining FII – foreign institutional

Plant, Corporation, investment,

CPP -Captive Power Plant, SA – South Africa FDI – foreign direct

EU – European Union, investment

Prabhash Gokarn et al. Page 15 of 16

16. The Indian Ferro Alloy Industry At Cross Roads

Prabhash Gokarn et al. Page 16 of 16