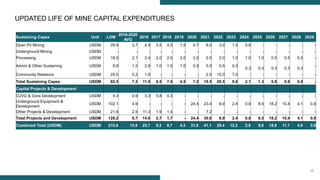

Download to read offline

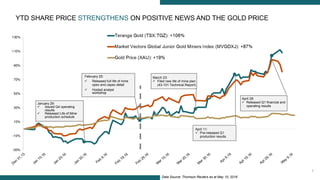

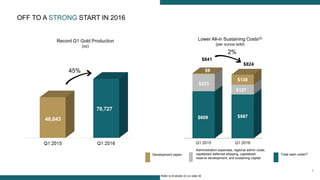

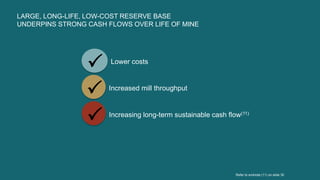

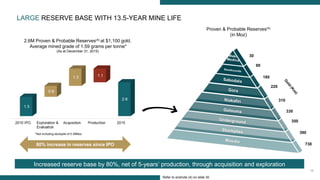

This investor presentation provides an overview of Teranga Gold Corporation and highlights its strong value proposition as an emerging gold producer in West Africa. Key points include: - Teranga is an emerging gold producer with operations in Senegal, located within a prospective gold belt along the Senegal-Mali border where over 50 million ounces have been discovered. - In the first quarter of 2016, Teranga achieved record gold production of 45,000 ounces at lower all-in sustaining costs of $824 per ounce sold. - Teranga has a large, long-life reserve and resource base that supports strong cash flows over the mine life based on the current life of mine plan. There is also potential to

![Productivity in Mining[998]](https://cdn.slidesharecdn.com/ss_thumbnails/29da160e-a9b3-4f62-a817-2e42cc5c3219-161115105342-thumbnail.jpg?width=640&height=640&fit=bounds)