1. Date - 26th November, 2013Date - 26th November, 2013Date - 26 November, 2013

Tata global beverages ltd. - BUYTata global beverages ltd. - BUYTata global beverages ltd. - BUYTata global beverages ltd. - BUYTata global beverages ltd. - BUY

CMP - INR 142.00 TP - INR 162.00 RiskCMP - INR 142.00 TP - INR 162.00 RiskCMP - INR 142.00 TP - INR 162.00 Risk

TH - 12 Months Up Side - 15.00 % ReturnTH - 12 Months Up Side - 15.00 % Return

We initiate investment note on Tata global beverages ltd. (TataWe initiate investment note on Tata global beverages ltd. (TataWe initiate investment note on Tata global beverages ltd. (Tata

with a DCF valuation based Price target of 162 over a periodwith a DCF valuation based Price target of 162 over a periodwith a DCF valuation based Price target of 162 over a period

representing a potential upside of 15%. At CMP of 142, therepresenting a potential upside of 15%. At CMP of 142, therepresenting a potential upside of 15%. At CMP of 142, the

19.52x and 17.50x its estimated earnings for FY14 and FY15,19.52x and 17.50x its estimated earnings for FY14 and FY15,

global presence, strong brand image and favorable raw materialglobal presence, strong brand image and favorable raw materialglobal presence, strong brand image and favorable raw material

attractive points of TGBL which lead the top and bottom lineattractive points of TGBL which lead the top and bottom lineattractive points of TGBL which lead the top and bottom line

9.24% and 14.54% respectively, over the period of FY13A to9.24% and 14.54% respectively, over the period of FY13A to9.24% and 14.54% respectively, over the period of FY13A to

stock as a potential investment opportunity.stock as a potential investment opportunity.stock as a potential investment opportunity.

Investment rationaleInvestment rationaleInvestment rationale

Strong brand equity with acquisitions and partnerships with Starbucks & PepsiCoStrong brand equity with acquisitions and partnerships with Starbucks & PepsiCo

Strong brand image of “Tea products” are the major strengthStrong brand image of “Tea products” are the major strengthStrong brand image of “Tea products” are the major strength

contributed 72% of revenue in top line number. Tea revenue grewcontributed 72% of revenue in top line number. Tea revenue grewcontributed 72% of revenue in top line number. Tea revenue grew

over last five years at a CAGR of 8.85%, instead of an expectedover last five years at a CAGR of 8.85%, instead of an expectedover last five years at a CAGR of 8.85%, instead of an expected

respectively over the period of FY13A to FY18E. TGBL hasrespectively over the period of FY13A to FY18E. TGBL hasrespectively over the period of FY13A to FY18E. TGBL has

opportunity not only in India but across the globe. Acquisitionsopportunity not only in India but across the globe. Acquisitionsopportunity not only in India but across the globe. Acquisitions

Starbucks & Pepsico offer a huge market potential for the companyStarbucks & Pepsico offer a huge market potential for the companyStarbucks & Pepsico offer a huge market potential for the company

its products in local & global markets.its products in local & global markets.its products in local & global markets.

Impressive global presence helps to continue the growth at sameImpressive global presence helps to continue the growth at same

Healthy growth has been added by its global presence in tea segment,Healthy growth has been added by its global presence in tea segment,Healthy growth has been added by its global presence in tea segment,

value share of Tata Tea), Canada (Tetley), UK (27% value sharevalue share of Tata Tea), Canada (Tetley), UK (27% value sharevalue share of Tata Tea), Canada (Tetley), UK (27% value share

of leading brands across the globe, Joekels in South Africa (thirdof leading brands across the globe, Joekels in South Africa (thirdof leading brands across the globe, Joekels in South Africa (third

Earth in US (21% volume share), Jemca in Czech Republic (whichEarth in US (21% volume share), Jemca in Czech Republic (whichEarth in US (21% volume share), Jemca in Czech Republic (which

and Vitax in Poland (16% share of fruit tea market). Withand Vitax in Poland (16% share of fruit tea market). Withand Vitax in Poland (16% share of fruit tea market). With

presence, we believe that TGBL would continue to grow its teapresence, we believe that TGBL would continue to grow its teapresence, we believe that TGBL would continue to grow its tea

pace further.pace further.

Favorable fall down in Kenya tea pricesFavorable fall down in Kenya tea pricesFavorable fall down in Kenya tea prices

Majority of Tetley Teas requirement is sourced from Kenya. SinceMajority of Tetley Teas requirement is sourced from Kenya. SinceMajority of Tetley Teas requirement is sourced from Kenya. Since

are fall down by 24.86% on a yoy basis till Oct 2013 it will helpare fall down by 24.86% on a yoy basis till Oct 2013 it will helpare fall down by 24.86% on a yoy basis till Oct 2013 it will help

material cost across geographies which would also help supportmaterial cost across geographies which would also help supportmaterial cost across geographies which would also help support

BUYBUYBUYBUYBUY

Risk - MediumRisk - MediumRisk - Medium

Return - Medium “Over 15 % “Return - Medium “Over 15 % “

(Tata Global) as a BUY(Tata Global) as a BUY(Tata Global) as a BUY

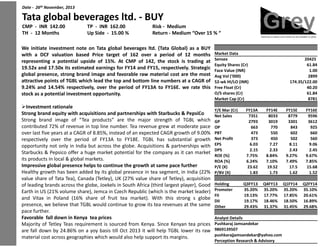

period of 12 months Market Dataperiod of 12 months Market Data

Sensex 20425

period of 12 months

the stock is trading at Sensex 20425

the stock is trading at Sensex 20425

Equity Shares (Cr) 61.84

the stock is trading at

respectively. Strategic

Equity Shares (Cr) 61.84

Face Value (INR) 1.00

respectively. Strategic

material cost are the most

Face Value (INR) 1.00

material cost are the most

Face Value (INR) 1.00

Avg Vol (‘000) 2899material cost are the most

numbers at a CAGR of

Avg Vol (‘000) 2899

numbers at a CAGR of

Avg Vol (‘000) 2899

52-wk HI/LO (INR) 174.35/122.00numbers at a CAGR of

to FY16E. we rate this

52-wk HI/LO (INR) 174.35/122.00

Free Float (Cr) 40.20to FY16E. we rate this Free Float (Cr) 40.20to FY16E. we rate this Free Float (Cr) 40.20

O/S shares (Cr) 61.84O/S shares (Cr) 61.84O/S shares (Cr) 61.84

Market Cap (Cr) 8781Market Cap (Cr) 8781

Y/E Mar (Cr) FY13A FY14E FY15E FY16E

cquisitions and partnerships with Starbucks & PepsiCo

Y/E Mar (Cr) FY13A FY14E FY15E FY16E

Net Sales 7351 8033 8779 9596

cquisitions and partnerships with Starbucks & PepsiCo

strength of TGBL which

Net Sales 7351 8033 8779 9596

strength of TGBL which

Net Sales 7351 8033 8779 9596

GP 2793 3019 3301 3612strength of TGBL which

grew at moderate pace

GP 2793 3019 3301 3612

grew at moderate pace

GP 2793 3019 3301 3612

OP 663 770 843 925grew at moderate pace

CAGR growth of 9.00%

OP 663 770 843 925

PBT 473 550 602 660CAGR growth of 9.00% PBT 473 550 602 660CAGR growth of 9.00%

has substantial growth

PBT 473 550 602 660

Net Profit 373 450 502 560has substantial growth Net Profit 373 450 502 560has substantial growth

Acquisitions & partnerships with

Net Profit 373 450 502 560

EPS 6.03 7.27 8.11 9.06Acquisitions & partnerships with EPS 6.03 7.27 8.11 9.06

DPS 2.15 2.33 2.43 2.45

Acquisitions & partnerships with

company as it can market

DPS 2.15 2.33 2.43 2.45

company as it can market

DPS 2.15 2.33 2.43 2.45

ROE (%) 7.75% 8.84% 9.27% 9.67%

company as it can market

ROE (%) 7.75% 8.84% 9.27% 9.67%

ROA (%) 6.24% 7.10% 7.49% 7.85%ROA (%) 6.24% 7.10% 7.49% 7.85%

same pace further

ROA (%) 6.24% 7.10% 7.49% 7.85%

P/E (X) 23.62 19.52 17.5 15.68same pace further

segment, in India (22%

P/E (X) 23.62 19.52 17.5 15.68

segment, in India (22%

P/E (X) 23.62 19.52 17.5 15.68

P/BV (X) 1.83 1.73 1.62 1.52segment, in India (22%

share of Tetley), acquisition

P/BV (X) 1.83 1.73 1.62 1.52

share of Tetley), acquisitionshare of Tetley), acquisition

(third largest player), Good Holding Q3FY13 Q4FY13 Q1FY14 Q2FY14(third largest player), Good Holding Q3FY13 Q4FY13 Q1FY14 Q2FY14(third largest player), Good

(which is the market leader)

Holding Q3FY13 Q4FY13 Q1FY14 Q2FY14

Promoter 35.20% 35.20% 35.20% 35.10%(which is the market leader) Promoter 35.20% 35.20% 35.20% 35.10%

FII 19.13% 17.77% 17.85% 20.61%

(which is the market leader)

With this strong s globe

FII 19.13% 17.77% 17.85% 20.61%

With this strong s globe

FII 19.13% 17.77% 17.85% 20.61%

DII 19.17% 18.46% 18.50% 16.89%

With this strong s globe

tea revenues at the same

DII 19.17% 18.46% 18.50% 16.89%

Other 29.43% 31.37% 31.45% 29.68%tea revenues at the same Other 29.43% 31.37% 31.45% 29.68%tea revenues at the same Other 29.43% 31.37% 31.45% 29.68%

Analyst Details

Since Kenyan tea prices

Analyst Details

Pushkaraj JamsandekarSince Kenyan tea prices Pushkaraj JamsandekarSince Kenyan tea prices

help TGBL lower its raw

Pushkaraj Jamsandekar

9869139507help TGBL lower its raw 9869139507help TGBL lower its raw

support its margins.

9869139507

pushkarajjamsandekar@yahoo.com

support its margins. pushkarajjamsandekar@yahoo.com

Perception Research & Advisory

support its margins.

Perception Research & AdvisoryPerception Research & Advisory

2. Company backgroundCompany backgroundCompany background

Tata Global Beverages Limited, through its subsidiaries, joint venturesTata Global Beverages Limited, through its subsidiaries, joint venturesTata Global Beverages Limited, through its subsidiaries, joint ventures

a global beverages company engaged in the trading, productiona global beverages company engaged in the trading, productiona global beverages company engaged in the trading, production

tea, coffee and water. The Company operates in three segments,tea, coffee and water. The Company operates in three segments,tea, coffee and water. The Company operates in three segments,

cultivation and manufacture of black tea and instant tea, tea buying/blendingcultivation and manufacture of black tea and instant tea, tea buying/blending

tea in bulk or value added form; Coffee and Other Produce, which

cultivation and manufacture of black tea and instant tea, tea buying/blending

tea in bulk or value added form; Coffee and Other Produce, whichtea in bulk or value added form; Coffee and Other Produce, which

coffee, pepper and other plantation crops and conversion of coffeecoffee, pepper and other plantation crops and conversion of coffeecoffee, pepper and other plantation crops and conversion of coffee

as roast and ground coffee and instant coffee, and Others, whichas roast and ground coffee and instant coffee, and Others, whichas roast and ground coffee and instant coffee, and Others, which

mineral water, other minor crops, curing operations of coffeemineral water, other minor crops, curing operations of coffeemineral water, other minor crops, curing operations of coffee

required for coffee plantations.required for coffee plantations.required for coffee plantations.

Share holding patternShare holding patternShare holding pattern

Y/E March 31 FY13Q2 FY13Q3 FY13Q4Y/E March 31 FY13Q2 FY13Q3 FY13Q4

(A) Promoter Group 35.57% 35.57% 35.55%(A) Promoter Group 35.57% 35.57% 35.55%(A) Promoter Group 35.57% 35.57% 35.55%

Bodies Corporate 35.57% 35.57% 35.55%Bodies Corporate 35.57% 35.57% 35.55%

(B) Public Shareholding(B) Public Shareholding(B) Public Shareholding

(1) Institutions 0.40% 0.39% 0.37%(1) Institutions 0.40% 0.39% 0.37%

Mutual Funds / UTI 4.86% 4.22% 4.29%Mutual Funds / UTI 4.86% 4.22% 4.29%Mutual Funds / UTI 4.86% 4.22% 4.29%

Financial Institutions / Banks 13.14% 10.93% 10.69%Financial Institutions / Banks 13.14% 10.93% 10.69%

Government State / Central 0.03% 0.03% 0.03%

Financial Institutions / Banks 13.14% 10.93% 10.69%

Government State / Central 0.03% 0.03% 0.03%Government State / Central 0.03% 0.03% 0.03%

Insurance Companies 5.43% 4.18% 3.62%Insurance Companies 5.43% 4.18% 3.62%Insurance Companies 5.43% 4.18% 3.62%

Foreign Institutional Investors 16.69% 19.33% 17.94%Foreign Institutional Investors 16.69% 19.33% 17.94%

(2) Non-Institutions 0.02% 0.03% 0.03%(2) Non-Institutions 0.02% 0.03% 0.03%(2) Non-Institutions 0.02% 0.03% 0.03%

Bodies Corporate 2.43% 2.96% 2.83%Bodies Corporate 2.43% 2.96% 2.83%

(3) Individuals 0.22% 0.23% 0.25%(3) Individuals 0.22% 0.23% 0.25%(3) Individuals 0.22% 0.23% 0.25%

Individual holding up to Rs. 1 lakh 20.25% 20.98% 22.83%Individual holding up to Rs. 1 lakh 20.25% 20.98% 22.83%

Individual holding excess of Rs. 1 lakh 0.84% 0.96% 1.06%Individual holding excess of Rs. 1 lakh 0.84% 0.96% 1.06%Individual holding excess of Rs. 1 lakh 0.84% 0.96% 1.06%

Others 0.77% 0.83% 1.14%Others 0.77% 0.83% 1.14%

Total 100.00% 100.00% 100.00%

Others 0.77% 0.83% 1.14%

Total 100.00% 100.00% 100.00%Total 100.00% 100.00% 100.00%

ventures and associates, isventures and associates, isventures and associates, is

production and distribution ofproduction and distribution ofproduction and distribution of

segments, Tea, which includessegments, Tea, which includessegments, Tea, which includes

buying/blending and sale ofbuying/blending and sale of

which includes cultivation of

buying/blending and sale of

which includes cultivation ofwhich includes cultivation of

coffee into products, suchcoffee into products, suchcoffee into products, such

which includes sale of naturalwhich includes sale of naturalwhich includes sale of natural

coffee and trading of itemscoffee and trading of itemscoffee and trading of items

FY13Q4 FY14Q1 FY14Q2 % QOQ % SPLYFY13Q4 FY14Q1 FY14Q2 % QOQ % SPLY

35.55% 35.54% 35.61% 0.20% 0.11%35.55% 35.54% 35.61% 0.20% 0.11%

Q2FY14

35.55% 35.54% 35.61% 0.20% 0.11%

35.55% 35.54% 35.61% 0.20% 0.11% Q2FY1435.55% 35.54% 35.61% 0.20% 0.11% Q2FY14Q2FY14

0.37% 0.37% 0.38% 3.62% -5.23% Promoter FII DII Other0.37% 0.37% 0.38% 3.62% -5.23%

4.29% 4.64% 4.28% -7.76% -11.93%

Promoter FII DII Other

4.29% 4.64% 4.28% -7.76% -11.93%4.29% 4.64% 4.28% -7.76% -11.93%

10.69% 10.52% 9.64% -8.37% -26.64%10.69% 10.52% 9.64% -8.37% -26.64%

0.03% 0.03% 0.08% 166.67% 166.67%

10.69% 10.52% 9.64% -8.37% -26.64%

0.03% 0.03% 0.08% 166.67% 166.67%0.03% 0.03% 0.08% 166.67% 166.67%

3.62% 3.50% 3.14% -10.29% -42.17%3.62% 3.50% 3.14% -10.29% -42.17%

29%

3.62% 3.50% 3.14% -10.29% -42.17%

17.94% 18.03% 20.91% 15.97% 25.28% 34%29%17.94% 18.03% 20.91% 15.97% 25.28%

0.03% 0.03% 0.02% -23.76% -4.94%

34%29%

0.03% 0.03% 0.02% -23.76% -4.94%0.03% 0.03% 0.02% -23.76% -4.94%

2.83% 3.03% 2.31% -23.76% -4.94%2.83% 3.03% 2.31% -23.76% -4.94%

0.25% 0.25% 0.24% -2.79% 9.93% 17%0.25% 0.25% 0.24% -2.79% 9.93%

20%

17%0.25% 0.25% 0.24% -2.79% 9.93%

22.83% 22.47% 21.88% -2.63% 8.05% 20%

17%

22.83% 22.47% 21.88% -2.63% 8.05%

1.06% 1.01% 0.98% -2.97% 16.67%

20%

1.06% 1.01% 0.98% -2.97% 16.67%1.06% 1.01% 0.98% -2.97% 16.67%

1.14% 1.24% 1.17% -5.65% 51.95%1.14% 1.24% 1.17% -5.65% 51.95%

100.00% 100.00% 100.00% 0.00% 0.00%

1.14% 1.24% 1.17% -5.65% 51.95%

100.00% 100.00% 100.00% 0.00% 0.00%100.00% 100.00% 100.00% 0.00% 0.00%

3. Investment rationaleInvestment rationale

Strong brand equity with acquisitions and partnerships with Starbucks & PepsicoStrong brand equity with acquisitions and partnerships with Starbucks & PepsicoStrong brand equity with acquisitions and partnerships with Starbucks & Pepsico

Strong brand image of “Tea products” are the major strength ofStrong brand image of “Tea products” are the major strength ofStrong brand image of “Tea products” are the major strength of

72% of revenue in top line number. Tea revenue grew at moderate72% of revenue in top line number. Tea revenue grew at moderate72% of revenue in top line number. Tea revenue grew at moderate

years at a CAGR of 8.85%, instead of an expected CAGR growthyears at a CAGR of 8.85%, instead of an expected CAGR growthyears at a CAGR of 8.85%, instead of an expected CAGR growth

over the period of FY13A to FY18E. TGBL has substantial growthover the period of FY13A to FY18E. TGBL has substantial growthover the period of FY13A to FY18E. TGBL has substantial growth

India but across the globe. Acquisitions & partnerships with StarbucksIndia but across the globe. Acquisitions & partnerships with StarbucksIndia but across the globe. Acquisitions & partnerships with Starbucks

huge market potential for the company as it can market its productshuge market potential for the company as it can market its productshuge market potential for the company as it can market its products

markets.markets.

Exhibit 01: Growth in Tea revenueExhibit 01: Growth in Tea revenueExhibit 01: Growth in Tea revenue

6851 12%8000

6285

6851

11%

12%8000

5290

5766

6285

6851

11%

10%

4767

5290

5766

9% 9% 9%

10%

6000

4767

5290 9% 9% 9%

8%

6000

6% 6%

8%

4000 6% 6%4000

4%

6%4000

4%

2000

2%

4%

2000

2%

2000

0%0 0%0

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16E

Tea GrowthTea Growth

Source: Perception Research & AdvisorySource: Perception Research & Advisory

Exhibit 03: Growth in paper and other revenueExhibit 03: Growth in paper and other revenue

50%120

100

50%120

90 95 100

42%

50%

100

120

80

86 90 95

42% 40%100

80

8642% 40%

80

100

30%

80

30%

60

80

20%

60

20%

40

20%

40

8% 10%20 8%

5% 5% 5%

10%20

5% 5% 5%

0%0 0%0

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16E

Paper & Other Growth

Source: Perception Research & Advisory

Paper & Other Growth

Source: Perception Research & AdvisorySource: Perception Research & Advisory

cquisitions and partnerships with Starbucks & Pepsicocquisitions and partnerships with Starbucks & Pepsicocquisitions and partnerships with Starbucks & Pepsico

of TGBL which contributedof TGBL which contributedof TGBL which contributed

moderate pace over last fivemoderate pace over last fivemoderate pace over last five

growth of 9.00% respectivelygrowth of 9.00% respectivelygrowth of 9.00% respectively

growth opportunity not only ingrowth opportunity not only ingrowth opportunity not only in

Starbucks & Pepsico offer aStarbucks & Pepsico offer aStarbucks & Pepsico offer a

products in local & globalproducts in local & globalproducts in local & global

Exhibit 02: Growth in Coffee revenueExhibit 02: Growth in Coffee revenueExhibit 02: Growth in Coffee revenue

25%3000

2472

25%3000

2043

2247

2472

20% 20%2500

1857

2043

2247

20% 20%2500

1706

1857

2043

15%

2000 1706

15%

1500

2000

15%

1500

9% 10% 10% 10% 10%

1000

1500

9% 10% 10% 10% 10%

1000

5%500

1000

5%500

0%0 0%0

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16E

Coffee GrowthCoffee Growth

Source: Perception Research & AdvisorySource: Perception Research & Advisory

Exhibit 04:NIM - Growth in Total revenueExhibit 04:NIM - Growth in Total revenue

12%12000 12%12000

8781

9597

12%

10000

12000

8034

8781

9597

11% 11%

11%10000

6633

7352

8034

8781

11% 11%

11%

8000

10000

6633

735211% 11%

11%

8000 6633

11%

6000

10%

6000

10%

4000

10%

4000

9% 9%

10%2000

9% 9% 9%

10%2000

9% 9% 9%

9%0 9%0

FY12A FY13A FY14E FY15E FY16EFY12A FY13A FY14E FY15E FY16E

Total Revenue Growth

Source: Perception Research & Advisory

Total Revenue Growth

Source: Perception Research & AdvisorySource: Perception Research & Advisory

4. Impressive global presence helps to continue the growth at sameImpressive global presence helps to continue the growth at same

Healthy growth has been added by its global presence in teaHealthy growth has been added by its global presence in teaHealthy growth has been added by its global presence in tea

value share of Tata Tea), Canada (Tetley), UK (27% value sharevalue share of Tata Tea), Canada (Tetley), UK (27% value sharevalue share of Tata Tea), Canada (Tetley), UK (27% value share

leading brands across the globe, Joekels in South Africa (third largestleading brands across the globe, Joekels in South Africa (third largestleading brands across the globe, Joekels in South Africa (third largest

in US (21% volume share), Jemca in Czech Republic (which isin US (21% volume share), Jemca in Czech Republic (which isin US (21% volume share), Jemca in Czech Republic (which is

Vitax in Poland (16% share of fruit tea market). With this strongVitax in Poland (16% share of fruit tea market). With this strongVitax in Poland (16% share of fruit tea market). With this strong

believe that TGBL would continue to grow its tea revenues at thebelieve that TGBL would continue to grow its tea revenues at thebelieve that TGBL would continue to grow its tea revenues at the

Favorable fall down in Kenya tea pricesFavorable fall down in Kenya tea pricesFavorable fall down in Kenya tea prices

Majority of Tetley Teas requirement is sourced from Kenya. SinceMajority of Tetley Teas requirement is sourced from Kenya. Since

fall down by 24.86% on a yoy basis till Oct 2013 it will help TGBLfall down by 24.86% on a yoy basis till Oct 2013 it will help TGBLfall down by 24.86% on a yoy basis till Oct 2013 it will help TGBL

cost across geographies which would also help support its marginscost across geographies which would also help support its marginscost across geographies which would also help support its margins

Exhibit 05: Kenya tea pricesExhibit 05: Kenya tea pricesExhibit 05: Kenya tea prices

400400

300300

200200200

100100

00

11

11

11

12

12

12

12

12

12

12

12

12

12

12

12

13

13

13

Oct-11

Nov-11

Dec-11

Jan-12

Feb-12

Mar-12

Apr-12

May-12

Jun-12

Jul-12

Aug-12

Sep-12

Oct-12

Nov-12

Dec-12

Jan-13

Feb-13

Mar-13

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Nov

Dec

Feb

Mar

May

Aug

Sep

Nov

Dec

Feb

Mar

PricePrice

Source: Perception Research & AdvisorySource: Perception Research & Advisory

Exhibit 06: Change in Kenya tea pricesExhibit 06: Change in Kenya tea prices

4.00%4.00%

2.00%

4.00%

2.00%

0.00%

-2.00%

0.00%

-2.00%

11

11

11

12

12

12

12

12

12

12

12

12

12

12

12

13

13

-4.00%

-2.00%

Oct-11

Nov-11

Dec-11

Jan-12

Feb-12

Mar-12

Apr-12

May-12

Jun-12

Jul-12

Aug-12

Sep-12

Oct-12

Nov-12

Dec-12

Jan-13

Feb-13

-4.00%

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

-6.00%

Nov

Mar

May

Aug

Nov

-8.00%

-6.00%

-8.00%

-10.00%

-8.00%

-10.00%

-12.00%-12.00%

Source: Perception Research & AdvisorySource: Perception Research & AdvisorySource: Perception Research & Advisory

same space furthersame space further

tea segment, in India (22%tea segment, in India (22%tea segment, in India (22%

share of Tetley), acquisition ofshare of Tetley), acquisition ofshare of Tetley), acquisition of

largest player), Good Earthlargest player), Good Earthlargest player), Good Earth

is the market leader) andis the market leader) andis the market leader) and

strong s globe presence, westrong s globe presence, westrong s globe presence, we

the same space further.the same space further.the same space further.

Since Kenyan tea prices areSince Kenyan tea prices are

TGBL lower its raw materialTGBL lower its raw materialTGBL lower its raw material

margins.margins.margins.

13

13

13

13

13

13

13

13

Mar-13

Apr-13

May-13

Jun-13

Jul-13

Aug-13

Sep-13

Oct-13

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Mar

May

Aug

Sep

13

13

13

13

13

13

13

13

Mar-13

Apr-13

May-13

Jun-13

Jul-13

Aug-13

Sep-13

Oct-13

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Mar

May

Aug

6. ValuationValuation

Exhibit 08: Tata global beverages ltd. Valuation (Rs In Cr)Exhibit 08: Tata global beverages ltd. Valuation (Rs In Cr)

ValuationValuation

Risk Free Rate 7.00% FCFFRisk Free Rate 7.00% FCFFRisk Free Rate 7.00% FCFF

Market return 13.76% Terminal ValueMarket return 13.76% Terminal Value

Market Premium 6.76% Discount RateMarket Premium 6.76% Discount RateMarket Premium 6.76% Discount Rate

Beta 0.33 PeriodBeta 0.33 PeriodBeta 0.33 Period

Ke 9.24% Discount PV of FCFFKe 9.24% Discount PV of FCFF

Kd 8.50% PV of FCFFKd 8.50% PV of FCFFKd 8.50% PV of FCFF

G 3.00% PV of TVG 3.00% PV of TV

Equity 4810.12 Enterprise valueEquity 4810.12 Enterprise valueEquity 4810.12 Enterprise value

Debt 1016.83 Net debt & Minority IncomeDebt 1016.83 Net debt & Minority Income

We 0.83 Equity ValueWe 0.83 Equity ValueWe 0.83 Equity Value

Wd 0.17 No of sharesWd 0.17 No of shares

WACC 9.11% Stock PriceWACC 9.11% Stock PriceWACC 9.11% Stock Price

Source: Perception Research & AdvisorySource: Perception Research & AdvisorySource: Perception Research & Advisory

At CMP of 142 the stock is trading at 19.52x & 17.50x its FY14At CMP of 142 the stock is trading at 19.52x & 17.50x its FY14At CMP of 142 the stock is trading at 19.52x & 17.50x its FY14

global presence, strong brand image and favorable raw materialglobal presence, strong brand image and favorable raw materialglobal presence, strong brand image and favorable raw material

attractive points of TGBL which lead the top and bottom lineattractive points of TGBL which lead the top and bottom lineattractive points of TGBL which lead the top and bottom line

9.24% and 14.54% respectively, over the period of FY13A to FY9.24% and 14.54% respectively, over the period of FY13A to FY9.24% and 14.54% respectively, over the period of FY13A to FY

valuation we arrive at the target price of 162 with a BUY ratingvaluation we arrive at the target price of 162 with a BUY ratingvaluation we arrive at the target price of 162 with a BUY rating

15%.15%.15%.

FY14E FY15E FY16E FY17E FY18EFY14E FY15E FY16E FY17E FY18E

612.89 653.80 689.19 733.36 779.57612.89 653.80 689.19 733.36 779.57612.89 653.80 689.19 733.36 779.57

13143.7813143.78

0.92 0.84 0.77 0.71 0.650.92 0.84 0.77 0.71 0.650.92 0.84 0.77 0.71 0.65

1 2 3 4 51 2 3 4 51 2 3 4 5

561.73 549.19 530.59 517.46 504.14561.73 549.19 530.59 517.46 504.14

2663.102663.102663.10

8499.978499.97

11163.0811163.0811163.08

Income 1116.80Income 1116.80

10046.2810046.2810046.28

61.8461.84

162.46162.46162.46

14E & FY15E EPS. Strategic14E & FY15E EPS. Strategic14E & FY15E EPS. Strategic

material cost are the mostmaterial cost are the mostmaterial cost are the most

line numbers at a CAGR ofline numbers at a CAGR ofline numbers at a CAGR of

FY16E. Based on our DCFFY16E. Based on our DCFFY16E. Based on our DCF

rating and a potential upside ofrating and a potential upside ofrating and a potential upside of

7. Investment Criteria & DisclaimerInvestment Criteria & DisclaimerInvestment Criteria & Disclaimer

Rating Low RiskRating Low RiskRating Low Risk

Buy Over 15 %Buy Over 15 %

Accumulate 10 % to 15 %Accumulate 10 % to 15 %Accumulate 10 % to 15 %

Hold 0% to 10 %Hold 0% to 10 %

Sell Negative Returns Negative ReturnsSell Negative Returns Negative ReturnsSell Negative Returns Negative Returns

Risk DescriptionRisk Description

Low Risk High predictabilityLow Risk High predictabilityLow Risk High predictability

Medium Risk Moderate predictabilityMedium Risk Moderate predictability

High Risk Low predictabilityHigh Risk Low predictabilityHigh Risk Low predictability

Analyst DetailsAnalyst DetailsAnalyst Details

Pushkaraj JamsandekarPushkaraj JamsandekarPushkaraj Jamsandekar

MMS - FinanceMMS - Finance

Contact - +09869139507Contact - +09869139507Contact - +09869139507

Email ID - pushkarajjamsandekar@yahoo.comEmail ID - pushkarajjamsandekar@yahoo.com

Perception Research & AdvisoryPerception Research & AdvisoryPerception Research & Advisory

DisclaimerDisclaimerDisclaimer

This document is for private circulation and information purposes only andThis document is for private circulation and information purposes only andThis document is for private circulation and information purposes only and

taxation or legal advice. Investors should seek financial advice regarding thetaxation or legal advice. Investors should seek financial advice regarding the

investment strategies discussed or recommended in this publication andinvestment strategies discussed or recommended in this publication andinvestment strategies discussed or recommended in this publication and

future prospects may not be realized. In no circumstances it be used or consideredfuture prospects may not be realized. In no circumstances it be used or considered

offer to buy or sell the securities mentioned in it. We and our affiliates, officers,offer to buy or sell the securities mentioned in it. We and our affiliates, officers,offer to buy or sell the securities mentioned in it. We and our affiliates, officers,

involved in the preparation or issuance of this material may: (a) from timeinvolved in the preparation or issuance of this material may: (a) from time

or sell the securities thereof, of company(ies) mentioned herein or (b) beor sell the securities thereof, of company(ies) mentioned herein or (b) beor sell the securities thereof, of company(ies) mentioned herein or (b) be

securities and earn brokerage or other compensation or act as a marketsecurities and earn brokerage or other compensation or act as a market

company(ies) dis-cussed herein or act as an advisor or lender or borrower to

securities and earn brokerage or other compensation or act as a market

company(ies) dis-cussed herein or act as an advisor or lender or borrower tocompany(ies) dis-cussed herein or act as an advisor or lender or borrower to

of interest with respect to any recommendation and re-lated informationof interest with respect to any recommendation and re-lated informationof interest with respect to any recommendation and re-lated information

publication may have been taken from trade and statistical services and otherpublication may have been taken from trade and statistical services and other

does not guarantee that such information is accurate or complete and it shoulddoes not guarantee that such information is accurate or complete and it shoulddoes not guarantee that such information is accurate or complete and it should

pressed reflects judgments at this date and are subject to change withoutpressed reflects judgments at this date and are subject to change without

investment can be substantial. You should carefully consider whether tradinginvestment can be substantial. You should carefully consider whether tradinginvestment can be substantial. You should carefully consider whether trading

your experience, objectives, financial resources and other relevant circumstancesyour experience, objectives, financial resources and other relevant circumstances

Perception Research & AdvisoryPerception Research & Advisory

Medium Risk High RiskMedium Risk High RiskMedium Risk High Risk

Over 20% Over 25%Over 20% Over 25%

15% to 20% 20% to 25%15% to 20% 20% to 25%15% to 20% 20% to 25%

0% to 15% 0% to 20%0% to 15% 0% to 20%

Negative Returns Negative ReturnsNegative Returns Negative ReturnsNegative Returns Negative Returns

Predictability Price VolatilityPredictability Price Volatility

High predictability Low volatilityHigh predictability Low volatilityHigh predictability Low volatility

Moderate predictability Average volatilityModerate predictability Average volatility

Low predictability High volatilityLow predictability High volatilityLow predictability High volatility

and should not be regarded as an investment,and should not be regarded as an investment,and should not be regarded as an investment,

the appropriateness of investing in any securities orthe appropriateness of investing in any securities or

and should under-stand that statements regardingand should under-stand that statements regardingand should under-stand that statements regarding

considered as an offer to sale or a solicitation of anyconsidered as an offer to sale or a solicitation of any

officers, directors and employees including personsofficers, directors and employees including personsofficers, directors and employees including persons

to time, have long or short positions in, and buyto time, have long or short positions in, and buy

engaged in any other transaction involving suchengaged in any other transaction involving suchengaged in any other transaction involving such

market maker in the financial instruments of themarket maker in the financial instruments of the

to such company or have other potential conflict

market maker in the financial instruments of the

to such company or have other potential conflictto such company or have other potential conflict

and opinions. The information contained in thisand opinions. The information contained in thisand opinions. The information contained in this

other sources, which we believe are reliable. Weother sources, which we believe are reliable. We

should not be relied upon as such. Any opinion ex-should not be relied upon as such. Any opinion ex-should not be relied upon as such. Any opinion ex-

without notice. Caution: Risk of loss in trading &without notice. Caution: Risk of loss in trading &

trading & investment is appropriate for you in light oftrading & investment is appropriate for you in light oftrading & investment is appropriate for you in light of

circumstances.circumstances.