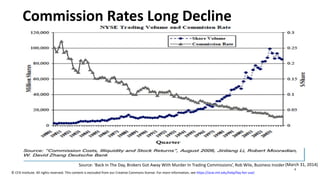

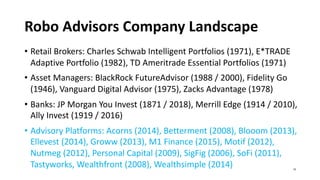

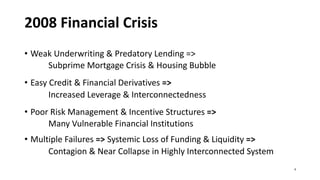

Class 5: Overview

•The Internet and the Payment Riddle

• Money

• Satoshi Nakamoto’s Innovation

• Crypto Markets

• Blockchain Technology Use Cases

• Challenges & Assessing Viability of Use Cases

• Central Bank Digital Currencies

• Ground Truths

2

41.

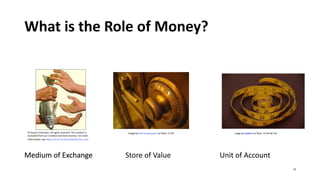

Internet and thePayments Riddle

• How to Move Value on the Internet

• Securely • As a Packet of Data – Peer to Peer

• Efficiently • While Prohibiting Double Spending

6

Money

Plato:

• Money isa ‘symbol’ devised for the purpose of exchanges

• Opposed using gold or silver for money

Aristotle:

• Solves the ‘problem of commensurability’

• ‘Money is a guarantee that we may have what we want in the future. Though we

need nothing at the moment it insures the possibility of satisfying a new desire

when it arises.’

• Four absolutes to have ‘Universal Value’:

• Durable, Portable, Divisible & Intrinsic Value

Modern Characteristics:

• Durable, Portable, Divisible, Uniform, Acceptable, & Stable

Image is in the public domain.

9

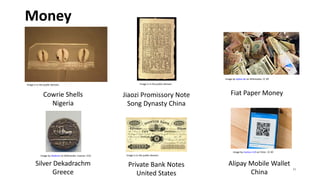

Money

Image by epSos.deon Wikimedia. CC BY

Image is in e p b i domain.

Image is in e p b i domain.

Cowrie Shells Jiaozi Promissory Note Fiat Paper Money

Nigeria Song Dynasty China

Image by ade o on Wikimedia. i ense CC . Image is in e p b i domain.

Image by ma k s on i k . CC BY

Silver Dekadrachm Private Bank Notes Alipay Mobile Wallet

Greece United States China

11

47.

Fiat Currency

• Representedby:

• Central Bank Notes Image by epSos.de on Wikimedia. CC BY

• Central Bank Reserves &

• Commercial Bank Deposits

• Relies upon System of Ledgers

• Very Significant Network Effects:

• Accepted for Taxes

• Legal Tender for All Debts Public & Private

• Accepted throughout Economy / Optimum Currency Area

12

Satoshi Nakamoto: BitcoinP2P e-cash paper

October 31, 2008

“I've been working on a new electronic cash system that's fully

peer-to-peer, with no trusted third party.”

14

50.

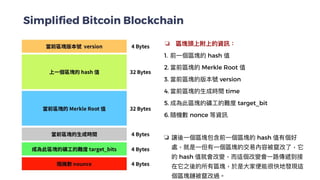

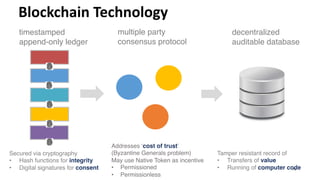

Blockchain Technology

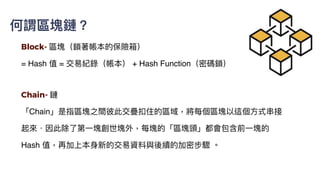

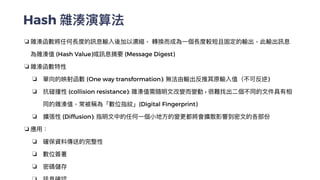

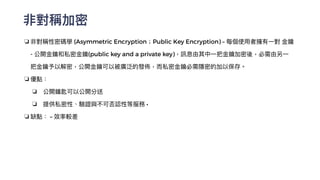

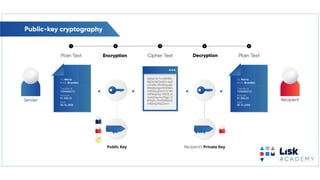

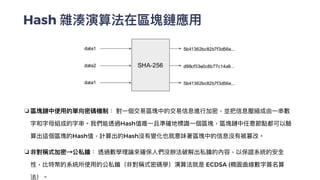

timestamped

append-only ledger

Securedvia cryptography

• Hash functions for integrity

• Digital signatures for consent

multiple party decentralized

consensus protocol auditable database

Addresses ‘cost of trust’

(Byzantine Generals problem)

May use Native Token as incentive

• Permissioned

• Permissionless

Tamper resistant record of

• Transfers of value

• Running of computer code

15

51.

Smart Contracts

• “Aset of promises,

• specified in digital form,

• including protocols

• within which the parties perform on these promises.”

Nick Szabo, 1996

However ….

• Smart Contracts may not be ‘Smart’

• Smart Contracts may not be ‘Contracts’ 16

52.

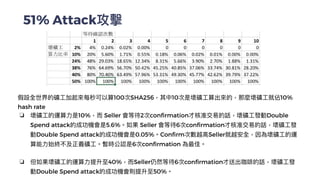

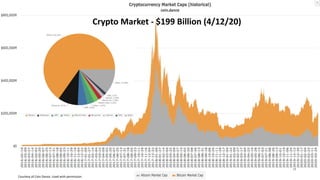

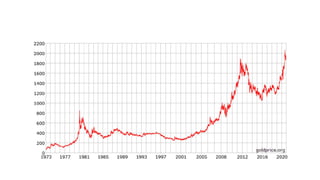

Crypto Market -$199 Billion (4/12/20)

17

Courtesy of Coin Dance. Used with permission.

53.

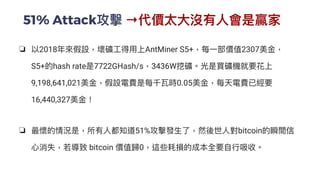

Crypto Token Sectors

•Payment/ Store of Value Tokens $152B – 76%

•Bitcoin ($128B), …

•Platform Tokens $29B – 15%

•Ethereum ($18B), …

•DApp Tokens $10B – 5%

•Binance Coin ($2.3B), …

•Stable Value Tokens $8B – 4%

•Tether ($6.4B), …

•Tokenized Securities and Assets

Source: Market Values from CoinMarketCap (4.12.20)

18

54.

Blockchain Tech PotentialUses

• Speculative Investing

• Crowdfunding through Initial Coin Offerings

• Tokens for Exchanges, Gaming, Gambling, DeFi & File Sharing

• Tokenized Fiat (Stable Value Coins), Securities & Assets

• Payment Systems

• Trade Finance & Supply Chain Management

• Clearing, Settlement & Processing

• Central Bank Initiatives

• Digital ID & MIT Diploma

• Medical Records, Property Records, Internet of Things, Voting … 19

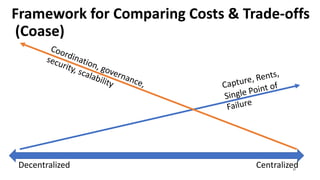

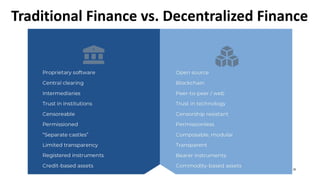

Framework for ComparingCosts & Trade-offs

(Coase)

Decentralized Centralized

Coordination, governance,

security, scalability Capture, Rents,

Single Point of

Failure

21

Assessing Use Cases–

First Considerations

Which side of a divide the project is on?

Is the project one that services the new crypto asset class?

Is the project one uses blockchain technology and cryptocurrencies?

Projects servicing the cryptocurrency space:

Custody solution – Coinbase, Fidelity Exchange operation – Binance, Coinbase

Software provider – Blockstream Wallet provider – Circle

Hardware company – BitMain Asset manager – Bitcoin Suisse, Galaxy

Mining pool operator – BTC, F2Pool, Poolin News service – CoinDesk

23

59.

Assessing Use Cases–

Strategic Considerations

• What value creation proposition is there?

• Decentralized vs. Centralized Computing?

• Native Token filling what Gaps in Fiat Currency system?

• What are competitors (Traditional & Blockchain) doing?

• Why use append only ledgers, multiple party consensus and native token?

• What verification or networking costs can actually be reduced?

24

60.

Assessing Use Cases–

Tactical Considerations

• Which data needs recording on append-only ledgers?

• Which multiple stakeholders need ‘write’ access to the shared ledger?

• What are the tradeoffs of performance, privacy, security, governance &

regulation?

• How can broad adoption and user interface be realized?

• If permissionless, what are the token incentive systems?

25

61.

Assessing Use Cases–

Deeper dive

• Why use multiple party shared ledger?

• Why choose a distributed ledger solution over a centralized one?

• Why not rely on a third-party authority or host?

• Is the value proposition well distributed amongst all parties?

• What is the adoption model?

• What specific verification or networking costs can be reduced?

• Authentication? Traceability? Trust?

• Are the transaction processes & data standardized?

• How much data needs to be stored?

26

62.

Incumbents’ Choices ofDatabases

Access

Client Server

Traditional Databases

Trusted Party Hosts Data

Trusted Party can Create, Read,

Update, & Delete (CRUD)

Client Server Architecture

Permissioned

Private Blockchain

Known Participants

Private Write Capability

Append Only Timestamped Log

Publicly Verifiable

No Native Currency Needed

Permissionless

Public Blockchain

Unknown Participants

No Central Intermediaries

Public Write Capability

Peer to Peer Transactions

Native Tokens & Incentives

? ?

?

?

?

27

63.

Central Bank Initiatives

RealTime Gross Settlement

• Brazil, Canada (Project Jasper), Europe and Japan (Project Stella), Singapore (Project

Ubin), South Africa (Project Khokha)

Digital Currency

• Central Bank Claim: Bahamas (Sand Dollar), Ecuador (Dinero Electrónico), Iran

(Payman), Sweden (E-Krona)

• Commercial Bank Claim: Philippines (ePiso), Senegal (eCFA), Tunisia (e-Dinar)

• Possible Hybrid: China (Digital Currency Electronic Payment)

• Commodity Backed: U.K. (Royal Mint Gold), Venezuela (Petro)

• Other: Dubai – emCash, Saudi & UAE (cross-border pilot), Uruguay (Digital Peso)

28

CBDC – Opportunities

•Continue Government Provision of a Means of Payment

• Promote Competition in Banking System

• Promote Financial Inclusion & P2P Payments

• Address Payment System ‘Pain Points’

• For Some Nations, Possibly Avert Sanctions

30

66.

CBDC - Challenges& Uncertainties

• Financial Stability and Potential to Increase Ease of Bank Runs

• Changes to Commercial Banks’ Deposits and Funding Models

• Effects on Credit Allocation and Economy

• Monetary Policy Implementation & Transmission

• Resilience of Open Payment Infrastructures

31

67.

Ground Truths

• Nakamotosolved the payments riddle - avoiding double spending

• Money is but a social & economic construct

• We already live in an age of digital money

• Append-only logs & multiparty consensus provides a peer-2-peer alternative

• Blockchain technology can address verification and networking costs

• Adoption rests on addressing comparative viability & value proposition

32

68.

Ground Truths

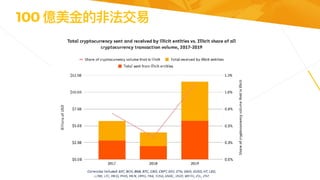

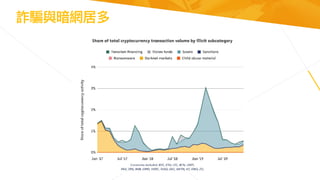

• Cryptomarkets are rife with scams, fraud, hacks & manipulation

• Cryptocurrencies have evolved into a speculative asset class

• Crowdfunding built on smart contracts & ICOs raised nearly $30 billion

• Lightly & non regulated markets provide retail investors direct way to trade

• The potential, though, to be a catalyst for change is real

33

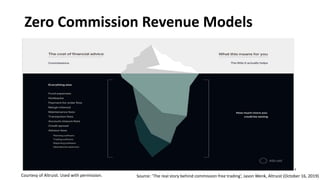

Zero Commission RevenueModels

9

Courtesy of Altruist. Used with permission. Source: ‘The real story behind commission free trading’, Jason Wenk, Altruist (October 16, 2019)

Capital Markets FinTechStartups

• Addepar (2009) – Wealth Management Platform for Financial Advisors

• Capitolis (2017) – Equities & FX Infrastructure

• Carta (2012) – Ownership Management Platform

• Cloud9 (2013) – Digitizing Voice Trading

• CloudMargin (2014) – Collateral Management

• Elefant (2018) – Digital Fixed Income Broker

• iCapital Network (2013) – Alternative Investment Platoform for

Financial Advisors

15

91.

Capital Markets FinTechStartups

• IEX (2012) – Stock Exchange

• Kantox (2011) – Institutional FX Trading

• Pitchbook (2007) – Private Capital Market Research

• Q4 (2006) – Investment Research

• Trumid (2014) – Bond Trading & Data Platform

• TruValue Labs (2013) – Analytics on ESG Investing

16

92.

Crypto Exchanges

• Actas agents (matching buyers & sellers) -- Traditional exchanges do as well

• Act as market makers (buying & selling from customers) -- Traditional exchanges don’t

• Hold customer funds in Custody -- Traditional exchanges don’t

• Public has direct access -- Traditional exchanges must go through a broker

• Lend money to customers for margin trading -- Securities markets use brokers or banks

• Crypto fees wide vs. Traditional markets

• Crypto Market Largely traded on Crypto only platforms – lacking direct fiat capabilities

• Not regulated for market integrity rules, rife with fake volumes and manipulation

• List tokens for fees similar to equity markets but different than currency markets

17

93.

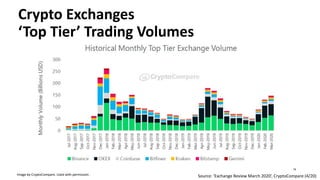

Crypto Exchanges

‘Top Tier’Trading Volumes

18

Image by CryptoCompare. Used with permission . Source: ‘Exchange Review March 2020’, CryptoCompare (4/20)

94.

Crypto Lending andBorrow

• Lending Crypto or Fiat collateralized by Crypto

•BlockFi, Celsius, CoinLoan, Crypto.com, ETHLend,

Genesis Capital, Nexo, Salt

19

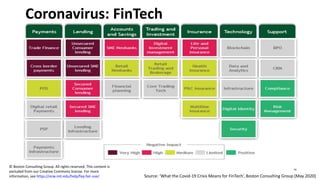

FinTech - Finance’sFertile Ground

Coronavirus Crisis

• Digitalization of Money, Securities and Credit

• Wide Public Acceptance of New Tech

• Legacy Customer Interface and Processing Systems

• Vast and Expanding Amounts of Customer Data

• Rapid Expansion of Computational & Analytical Power

• Reliance on Multiple Systems of Ledgers

• Infrastructure Systems’ Costs and Counterparty Risks

• Economic Rents and Centralized Concentrated Risks

10

105.

Coronavirus: FinTech Incumbents& Tech

• Big Finance

• Volumes: Capital Markets, Government Debt

• Stimulus Loan Programs

• Allocations for Loan Loss Reserves

• Reliance on Connectivity

• Big Tech

• Significant Online Growth

• Possible Shifts in Views on Data Usage - Contact Tracing

11

106.

Coronavirus: FinTech Startups

•Runway: Burn Rates, Cash, Revenue Model & Adoption Rates

• IPOs on Hold

• VC Investment will Slow

• Valuations Decline

• Consolidation Increases

• Sector Matters:

• Transaction fees & Consumer Credit?

• Retail, Travel, Events, Restaurants?

• Mobile Trading, Remittances, Compliance

12

107.

Coronavirus: FinTech

• AdditionalOpportunities

• Serving Those Tapping Fiscal Stimulus & Loan Programs

• Consumer & SME Refinancing's & Consolidation Loans

• New uses & sources of Alternative Data

• Additional Challenges

• Delinquencies & Defaults

• Loan Servicing

• Business Models relying on Float 13

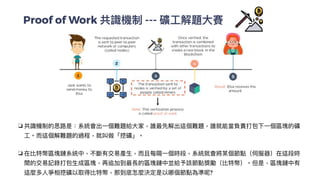

What is DeFi?

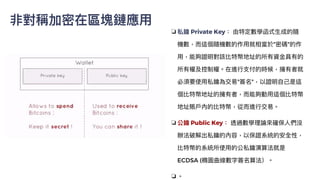

Ameme and a rallying cry A global mass movement

An industry of builders A reaction to failures in traditional finance

113.

Finance has noteven begun it’s equivalent to the printing press

phase of the information revolution!

— Joey Krug, CoFounder of Augur and Pantera

114.

1. Inaccessible

Financial servicesare

exclusionary based on

arbitrary criteria like

jurisdiction and investor

accreditation

2. Inefficient

Financial services are

plagued by human

intermediaries that are

costly in terms of money

and time

Finance is overdue for a revolution

Because despite all of its successes, finance remains:

3. Opaque

Financial services are

opaque, resulting in

“surprise” over-leveraging

or “too big to fail”

systemic risks

115.

3. Transparent

DeFi servicesare built on

publicly auditable

blockchains

2. Efficient

DeFi services use code to

eliminate intermediaries

with rote responsibilities

1. Accessible

DeFi services are globally

accessible to anyone with

an internet connection

DeFi is an attempt to correct these failures.

Flipping the script on traditional finance, DeFi services are:

116.

DeFi will doto Finance

what the Internet did to News Media

117.

DeFi democratizes creation

Blogsare permissionless news media.

DeFi is permissionless finance.

Insurance, Derivatives, Options

Augur

Baskets of Assets

Set

Lending Agreements

Dharma

Synthetic Financial Instruments

UMA

118.

DeFi democratizes access

NYTimes.comprovides anyone with an internet connection** access to news.

Dharma.io provides anyone with an internet connection access to dollar-denominated interest.

**Excluding government regimes that censor news media. One attack vector for DeFi may be government regimes that censor finance.

Hedging, Leverage, Shorting

dYdX

Exchange any value

AirSwap, 0x, Uniswap, Kyber

Compound your wealth

Dharma

Earn in the way you want

Whisp

119.

Smart contracts automatehuman processes that previously

needed to be “trusted”:

1. Custodians

2. Escrow agents

3. Paying agents

DeFi automates inefficient human processes

Who needs newspaper deliveries when you have the internet?

Who needs regulated custodians, escrow agents, or paying agents when you have smart contracts?

120.

DeFi is systemicallytransparent

In 2008, it was really hard to be Michael Burry.

In 2019, all it takes to be in The Big Short is Etherscan.

121.

DeFi is arevolution, creating the financial system that

was always meant to be.

122.

Ok we knowwhere we’re going,

but where are we today?

123.

DeFi growth willplay out in phases

PHASE 1 PHASE 2 PHASE 3

Market

Expansionary

Subsume

Legacy

Blockchain

Native

Today we’re in Phase 1, but by 2020 we’ll be market expansionary.

124.

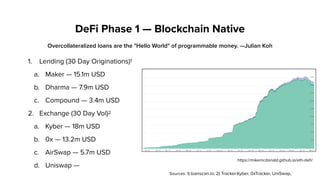

Overcollateralized loans arethe "Hello World" of programmable money. —Julian Koh

1. Lending (30 Day Originations)1

a. Maker — 15.1m USD

b. Dharma — 7.9m USD

c. Compound — 3.4m USD

2. Exchange (30 Day Vol)2

a. Kyber — 18m USD

b. 0x — 13.2m USD

c. AirSwap — 5.7m USD

d. Uniswap —

DeFi Phase 1 — Blockchain Native

https://mikemcdonald.github.io/eth-defi/

Sources: 1) loanscan.io; 2) Tracker.Kyber, 0xTracker, UniSwap,

125.

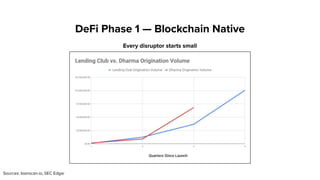

Every disruptor startssmall

DeFi Phase 1 — Blockchain Native

Sources: loanscan.io, SEC Edgar

126.

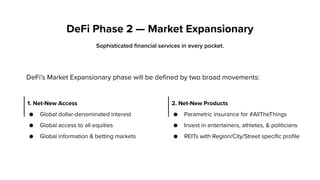

1. Net-New Access

●Global dollar-denominated interest

● Global access to all equities

● Global information & betting markets

Sophisticated financial services in every pocket.

DeFi’s Market Expansionary phase will be defined by two broad movements:

DeFi Phase 2 — Market Expansionary

2. Net-New Products

● Parametric insurance for #AllTheThings

● Invest in entertainers, athletes, & politicians

● REITs with Region/City/Street specific profile

Smart contract insurance

Smartcontracts fail. We need insurance for this.

Who’s cooking up a solution?

DeFi’s missing building blocks

What we need to go from here to there to everywhere

Better Fiat Onramps

Still takes far too long to move fiat to crypto.

Where’s my Stripe solution for this?

Better Oracles

Getting off-chain information on-chain still a

challenge. Who’s working on this?

Better Private Key Management

Hexadecimals, seed phrases, no recoverability.

Let’s fix these things!

130.

We know whatthe future can look like.

It’s up to the builders here to make it a reality.

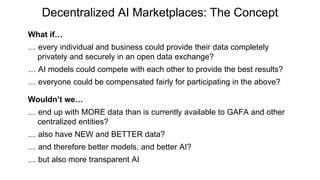

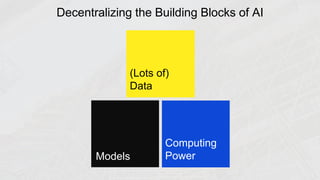

Decentralized AI Marketplaces:The Concept

What if…

e e d d a a d b e c d de e da a c e e

privately and securely in an open data exchange?

AI de c d c e e eac e de e be e ?

e e e c d be c e a ed a a c a e ab e?

Wouldn’t we…

e d MORE da a a c e a a ab e GAFA a d e

centralized entities?

a a e NEW a d BETTER da a?

a d e e e be e de , a d be e AI?

b a e a a e AI

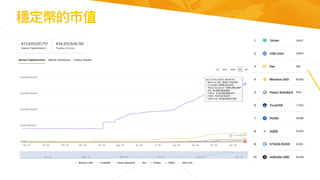

虛擬貨幣納入洗錢防制

FATF FinCEN

Proposed January2019 1997

Passed June 2019 2013

Effectiveness June 2020 in 37 G20 countries Enforcing now

Threshold 1,000 EUR 3,000 USD

DEXs Not covered* Potential covered

Private Coin and Mixers Must comply Must comply

Applies to

Financial Institutions

YES YES

* DEX is not covered by the FATF recommendation 16

![[GDC2010] Blizzard Design Process_KOR](https://cdn.slidesharecdn.com/ss_thumbnails/gdc2010presentationfinalv3korforwebv1-0-100421222645-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Crypto Course] Blockchain Security](https://cdn.slidesharecdn.com/ss_thumbnails/blockchain-201031054452-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ModernWeb2018] Web3.0 區塊鏈 DApp + 智能合約開發:你必要挑戰的坑坑洞洞](https://cdn.slidesharecdn.com/ss_thumbnails/web3-v1-180718031506-thumbnail.jpg?width=640&height=640&fit=bounds)