Download to read offline

![_____________________________________________________________________________________________________________________

Please refer to disclaimer Epic Research Ltd w w w . e p i c r e s e a r c h . c o

Special Report

09-May-2018

Global markets at a glance

Wall Street cut losses to end little changed on Tuesday

while energy stocks rallied after US President Donald

Trump said the United States would quit the Iran nuclear

deal, confirming what many investors had expected.

In a televised speech, Trump said the United States would

withdraw from a 2015 international agreement designed to

deny Tehran the ability to build nuclear weapons, and also

reinstate sanctions on Iran.

The S&P energy sector erased earlier losses to end the day

up 0.78 percent as oil prices reduced earlier declines on

bets that the sanctions would disrupt global crude supplies.

Asian shares crept higher on Monday after a tame reading

on US wages lessened the risk of faster rate hikes by the

Federal Reserve, although Sino-US trade tensions and a

looming deadline for the Iranian nuclear deal argued for

caution.

The week ahead also has important readings on the health

of the Chinese economy, and hence global demand, as well

as the latest data on US consumer price inflation.The early

action was limited with MSCI’s broadest index of Asia-

Pacific shares outside Japan up 0.2 percent.

Japan's Nikkei was flat, while Australian stocks added 0.3

percent. E-Mini futures for the S&P 500 also inched up 0.2

percent.

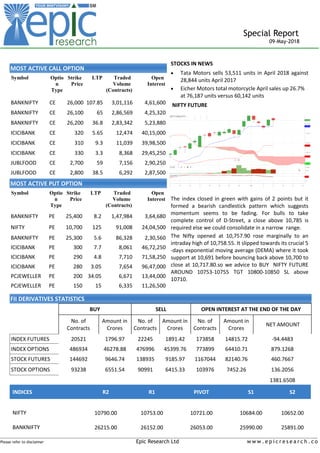

Previous day Roundup

The index closed in green with gains of 2 points but it

formed a bearish candlestick pattern which suggests

momentum seems to be fading. For bulls to take complete

control of D-Street, a close above 10,785 is required else

we could consolidate in a narrow range.

The Nifty opened at 10,757.90 rose marginally to an

intraday high of 10,758.55. It slipped towards its crucial 5-

days exponential moving average (DEMA) where it took

support at 10,691 before bouncing back above 10,700 to

close at 10,717.80.

India VIX moved up by 2.14 percent at 14.05. On the

options front, maximum Put OI is placed at 10,500 followed

by 10,600 strikes while maximum Call OI is placed at 11,000

followed by 10,800 strikes.

Index stats

The Market was very volatile in last session. The sartorial in

dices performed as follow; Commodities[9.80],

Consumption[-15.00pts],PSE[25.60pts],CPSE[5.80

pts],Energy[17.50pts],FMCG[ -31.35pts],Auto[-

52.40pts],Pharma[-21.15pts],IT[-45.25pts],Metal[-

6.85pts],Realty[3.70 pts], Fin Serv sector[ 50.95 pts].

World Indices

Index Value % Change

DJI 24,360.21 0.01

S&P500 2,670.00 0.22

NASDAQ 7,266.90 0.22

FTSE100 7,565.75 -0.02

NIKKEI 22,428.14 -0.36

HANG SENG 30,533.81 0.34

Top Gainers

Company CMP Change % Chg

ICICI Bank 309.30 19.50 6.73

HPCL 307.00 10.00 3.37

Eicher Motors 30,427.05 660.20 2.22

BPCL 392.60 6.80 1.76

Power Grid Corp 212.75 3.45 1.65

Top Losers

Company CMP Change % Chg

M&M 865.30 -20.30 -2.29

Idea Cellular 61.15 -1.25 -2.00

Larsen 1,364.90 -24.25 -1.75

Infosys 1,165.55 -17.45 -1.48

Bajaj Finance 1,868.40 -27.05 -1.43

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

5PAISA 486.85 -6.55 -1.35

AHLUCONT 425.1 -2.6 -0.61

ASHOKLEY 165.35 0 0

ASTERDM 178.75 7.9 4.42

ASTRAL 960 10 1.04

BOMDYEING 310.25 3.45 1.11

CUB 186.05 3.1 1.67

ARVSMART

Indian Indices

Company CMP Change % Chg

NIFTY 10717.80 2.30 0.02

SENSEX 35216.32 8.18 0.02

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

A2ZINFRA 25.6 -0.55 -2.15

ADHUNIK 3.35 0 0

ADROITINFO 30.15 -0.85 -2.82](https://image.slidesharecdn.com/special-report-09-may-2018-epic-research-180509051946/85/Special-report-09-may-2018-epic-research-1-320.jpg)

![_____________________________________________________________________________________________________________________

Please refer to disclaimer Epic Research Ltd w w w . e p i c r e s e a r c h . c o

Special Report

09-May-2018

Global markets at a glance

Wall Street cut losses to end little changed on Tuesday

while energy stocks rallied after US President Donald

Trump said the United States would quit the Iran nuclear

deal, confirming what many investors had expected.

In a televised speech, Trump said the United States would

withdraw from a 2015 international agreement designed to

deny Tehran the ability to build nuclear weapons, and also

reinstate sanctions on Iran.

The S&P energy sector erased earlier losses to end the day

up 0.78 percent as oil prices reduced earlier declines on

bets that the sanctions would disrupt global crude supplies.

Asian shares crept higher on Monday after a tame reading

on US wages lessened the risk of faster rate hikes by the

Federal Reserve, although Sino-US trade tensions and a

looming deadline for the Iranian nuclear deal argued for

caution.

The week ahead also has important readings on the health

of the Chinese economy, and hence global demand, as well

as the latest data on US consumer price inflation.The early

action was limited with MSCI’s broadest index of Asia-

Pacific shares outside Japan up 0.2 percent.

Japan's Nikkei was flat, while Australian stocks added 0.3

percent. E-Mini futures for the S&P 500 also inched up 0.2

percent.

Previous day Roundup

The index closed in green with gains of 2 points but it

formed a bearish candlestick pattern which suggests

momentum seems to be fading. For bulls to take complete

control of D-Street, a close above 10,785 is required else

we could consolidate in a narrow range.

The Nifty opened at 10,757.90 rose marginally to an

intraday high of 10,758.55. It slipped towards its crucial 5-

days exponential moving average (DEMA) where it took

support at 10,691 before bouncing back above 10,700 to

close at 10,717.80.

India VIX moved up by 2.14 percent at 14.05. On the

options front, maximum Put OI is placed at 10,500 followed

by 10,600 strikes while maximum Call OI is placed at 11,000

followed by 10,800 strikes.

Index stats

The Market was very volatile in last session. The sartorial in

dices performed as follow; Commodities[9.80],

Consumption[-15.00pts],PSE[25.60pts],CPSE[5.80

pts],Energy[17.50pts],FMCG[ -31.35pts],Auto[-

52.40pts],Pharma[-21.15pts],IT[-45.25pts],Metal[-

6.85pts],Realty[3.70 pts], Fin Serv sector[ 50.95 pts].

World Indices

Index Value % Change

DJI 24,360.21 0.01

S&P500 2,670.00 0.22

NASDAQ 7,266.90 0.22

FTSE100 7,565.75 -0.02

NIKKEI 22,428.14 -0.36

HANG SENG 30,533.81 0.34

Top Gainers

Company CMP Change % Chg

ICICI Bank 309.30 19.50 6.73

HPCL 307.00 10.00 3.37

Eicher Motors 30,427.05 660.20 2.22

BPCL 392.60 6.80 1.76

Power Grid Corp 212.75 3.45 1.65

Top Losers

Company CMP Change % Chg

M&M 865.30 -20.30 -2.29

Idea Cellular 61.15 -1.25 -2.00

Larsen 1,364.90 -24.25 -1.75

Infosys 1,165.55 -17.45 -1.48

Bajaj Finance 1,868.40 -27.05 -1.43

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

5PAISA 486.85 -6.55 -1.35

AHLUCONT 425.1 -2.6 -0.61

ASHOKLEY 165.35 0 0

ASTERDM 178.75 7.9 4.42

ASTRAL 960 10 1.04

BOMDYEING 310.25 3.45 1.11

CUB 186.05 3.1 1.67

ARVSMART

Indian Indices

Company CMP Change % Chg

NIFTY 10717.80 2.30 0.02

SENSEX 35216.32 8.18 0.02

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

A2ZINFRA 25.6 -0.55 -2.15

ADHUNIK 3.35 0 0

ADROITINFO 30.15 -0.85 -2.82](https://image.slidesharecdn.com/special-report-09-may-2018-epic-research-180509051946/75/Special-report-09-may-2018-epic-research-1-2048.jpg)

![_____________________________________________________________________________________________________________________

Please refer to disclaimer Epic Research Ltd w w w . e p i c r e s e a r c h . c o

Special Report

09-May-2018

STOCK RECOMMENDATION [CASH]

NIITECH [CASH]

The particular script has rebounded from its support level

of 1006 and closed with a good volume since it has clsoed

above its previous day spinning top candle so we can

remark a good bullish sign so we advice you to BUY

NIITECH 1066 TGT 1076-1086 SL BELOW 1057.

MACRO NEW

Trends on SGX Nifty indicate a flat to positive opening

for the broader index in India, a rise of 10.5 points or

0.1 percent. Nifty futures were trading around 10,756-

level on the Singaporean Exchange.

ICICI Bank reported 49.6 percent year-on-year drop in

net profit at Rs 1,020 crore for the fourth quarter

ending March 2018. Net profit for Q4FY17 was Rs

2,024.60 crore. The results were in line with estimates.

A Reuters poll had estimated net profit at Rs 955.7

crore.NII or net interest income inched up marginally

to Rs 6,021.67 crore in the quarter from Rs 5,962 crore

a year ago.

Oil prices retreated from three-and-a-half-year highs

on Tuesday as investors waited on an announcement

by President Donald Trump on whether the United

States will reimpose sanctions on Iran.US West Texas

Intermediate crude futures fell 63 cents, or 0.9

percent, to USD 70.10 a barrel. Brent crude futures

were down 53 cents, or 0.7 percent, at USD 75.64,

having jumped 1.7 percent to settle at USD 76.17 a

barrel in the previous session.

BlackRock, the US-based investment management firm

is in the final stage of talks with DSP to exit the mutual

fund joint venture--DSP BlackRock Investment

Managers--and the announcement is likely to be made

shortly, sources told Moneycontrol. DSP BlackRock

Investment Managers is a 40:60 joint venture between

BlackRock and DSP Group. As of March 31, 2018, DSP

BlackRock Investment Managers managed assets

worth Rs 86,325 crore, with a 50:50 mix of equity and

debt.

RECOMMENDATIONS [FUTURE]

1.BPCL [FUTURE ]

The particular script has rebounded from its support level of

374 and can break its crucial resistance level of 397.50 ,now

it has closed with a good volume so today we can witness a

good breakout since its making double bottom price

pattern , so buy on high would be a good opportunity to

trade. Here we recommend you to buy BPCL FUTURE

around 397.9-398.5 tgt 404-410 sl below 392.50.

2.JETAIRWAYS [FUTURE]

This particular counter is continuosly maitaining its

downtrend , below 507 there is no support level so sell on

low wowuld be a good startegy to follow so we recommend

to sell PRABHAT BELOW 507 TGT 500-490 SL ABOVE 512.](https://image.slidesharecdn.com/special-report-09-may-2018-epic-research-180509051946/85/Special-report-09-may-2018-epic-research-2-320.jpg)

The report discusses recent market movements following President Trump's decision to withdraw from the Iran nuclear deal, leading to gains in energy stocks as oil prices stabilized. It highlights fluctuations in Asian markets and provides insights into the performance of Indian stocks, including recommendations for specific trades based on current trends, particularly in the banking and commodities sectors. Additionally, macroeconomic indicators and company earnings are examined, with guidance on future trading strategies.