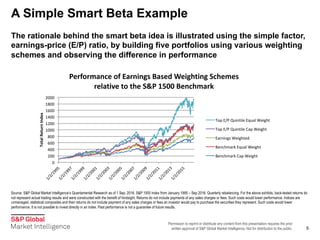

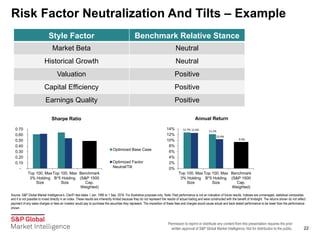

Download as PDF, PPTX

![Permission to reprint or distribute any content from this presentation requires the prior

written approval of S&P Global Market Intelligence. Not for distribution to the public.

Concluding Thoughts

23

• Avoid pitfalls of data mining

– Use economic intuition

– Check that the strategy is deriving returns (and risk) from intended exposures

• Combine complementary factors, e.g.

– Value & Quality/Capital Efficiency

– Momentum & Capacity Utilization [Aretz & Pope, 2015]

• Analyze investability with respect to liquidity, turnover, and transaction

costs/market impact

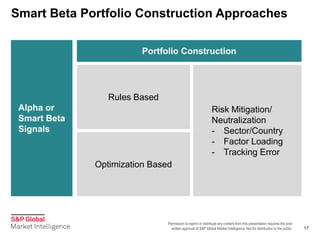

• Identify methods of risk control, e.g. risk model based vs. sector/country constraints

• Rules based vs. optimization based portfolio construction

– Tradeoff between transparency and flexibility](https://image.slidesharecdn.com/spglobalmarketintelligencesi2016-161013152336/85/Smarter-Beta-S-P-Global-Market-Intelligence-23-320.jpg)

The document discusses the concept of smart beta, defined as investment strategies that focus on better risk-adjusted returns through factor-based exposures, differing from traditional market-cap weighting. It highlights the growing adoption of smart beta ETFs among institutional investors and outlines various strategies and critiques surrounding smart beta, including performance concerns and the volatility of factor returns. Additionally, it presents a multi-factor approach as a way to enhance performance by combining different investment themes.