1. 1 | P a g e

PRASAL…. Easy Tax

Initiative of R.S.

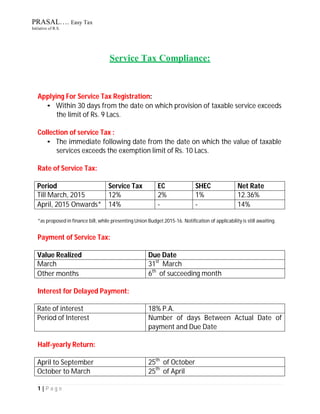

Service Tax Compliance:

Applying For Service Tax Registration:

• Within 30 days from the date on which provision of taxable service exceeds

the limit of Rs. 9 Lacs.

Collection of service Tax :

• The immediate following date from the date on which the value of taxable

services exceeds the exemption limit of Rs. 10 Lacs.

Rate of Service Tax:

Period Service Tax EC SHEC Net Rate

Till March, 2015 12% 2% 1% 12.36%

April, 2015 Onwards* 14% - - 14%

*as proposed in finance bill, while presenting Union Budget 2015-16. Notification of applicability is still awaiting.

Payment of Service Tax:

Value Realized Due Date

March 31st

March

Other months 6th

of succeeding month

Interest for Delayed Payment:

Rate of interest 18% P.A.

Period of Interest Number of days Between Actual Date of

payment and Due Date

Half-yearly Return:

April to September 25th

of October

October to March 25th

of April

2. 2 | P a g e

PRASAL…. Easy Tax

Initiative of R.S.

Late fees on delay filling of Return:

Delay in Days Late Fees Payable

Up to 15 Days Rs. 500

16 to 30 Days Rs.1000

More than 30 Days Rs 1,000/+ Rs 100 for each day of further

delay

Late fees will be subject to maximum Rs. 20,000.

Revision of Return:

• ST-3 form can be revised and submitted again within 90 days from the date

of filling original return.

Cenvat Credit:

• Cenvat credit can be taken on input services which facilitates in providing

taxable services.

• Service provider can not avail cenvat credit of inputs/input services after

expiry of six* months from the date of issue of invoice.

• Service provider has to make payment of gross value of invoices within 3

month, if such invoices have been considered for Cenvat Credit, if payment

for such invoices not made within prescribed limit then cenvat credit

already taken should be reversed by paying ”amount” equal to Cenvat

Credit availed on such Input Services. If later date, payment is made then

cenvat credit can be taken for the amount equal to cenvat credit revered

earlier.

*The word “Six” shall be substituted by “twelve” as proposed in Union Budget 2015-16.

3. 3 | P a g e

PRASAL…. Easy Tax

Initiative of R.S.

Accounting/Journal Entries:

• When Services are received:

Expenses A/c Dr. Expenses amount

Cenvat Credit Dr. Service tax amount

To Party A/c Gross Invoice value

(Being services expense recognized)

• When Services are provided:

Party A/c Dr. Gross value

Revenue A/c Income Amount

Service Tax payable A/c Service tax collected amount

(Being Income recognized)

• At the time of payment of Service Tax:

Service Tax Payable A/c Dr. Total S.T. collected amt. during the month

To Cenvat Credit A/c Cenvat credit amount applicable,

To Bank A/c. if cenvat is not sufficient to make

payment.

(Being service tax liability discharged by

utilizing cenvat credit available and balance

through bank)

Note:

1. Balance Cenvat credit shall be treated as asset.

2. Service tax payble shall be shown under liability.

The above entry may be presented in different manner as per the convenience of the entity,

but the ultimate effect shall remain same.