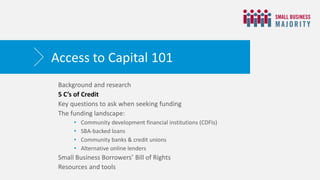

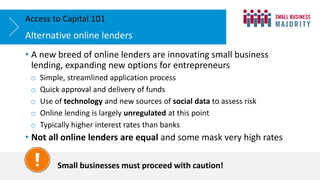

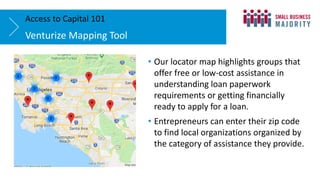

This document summarizes options for small business funding. It discusses community development financial institutions (CDFIs) that provide loans under $250k for underserved entrepreneurs. It also discusses SBA loan programs that guarantee portions of bank loans. Alternative online lenders are described as providing quick approval but at higher interest rates, so caution is advised. The document recommends researching funding options and understanding requirements like the 5 C's of credit before applying for loans. Resources like Venturize.org are provided to help small businesses compare funding options and become loan-ready.

![CQ Dallas ISD Board Presentation PowerPoint[1].pdf](https://cdn.slidesharecdn.com/ss_thumbnails/cqdallasisdboardpresentationpowerpoint1-230616004732-f56a83ce-thumbnail.jpg?width=640&height=640&fit=bounds)