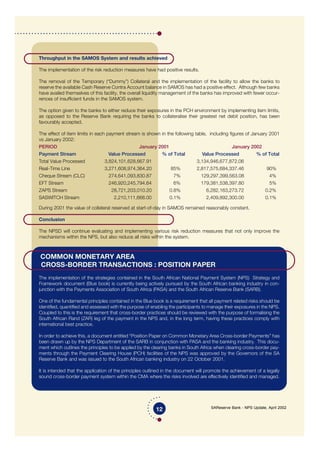

The document provides an update on the South African National Payment System (NPS) in April 2002. It discusses several ongoing projects and initiatives:

1. SAMOS Version 4.0 was implemented, including a Continuous Batch Processing Line functionality that allows banks to meet only net obligations in batches.

2. Risk reduction measures for the NPS are being reviewed, including business continuity plans for components like SAMOS, SWIFT, and collateral systems.

3. The SARB-Link infrastructure connecting banks to SAMOS is being renewed to replace outdated equipment and improve redundancy.

4. Oversight of the NPS by the South African Reserve Bank is aimed at promoting a smooth functioning payment