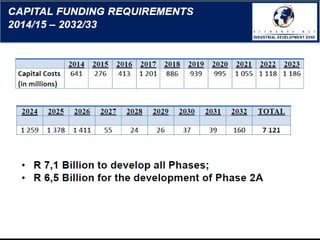

Download as PDF, PPTX

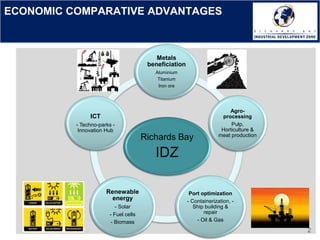

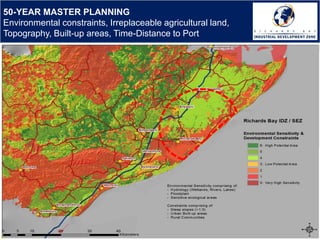

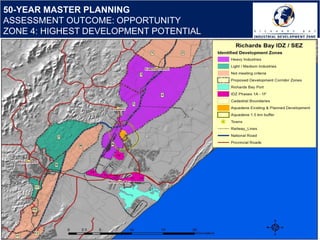

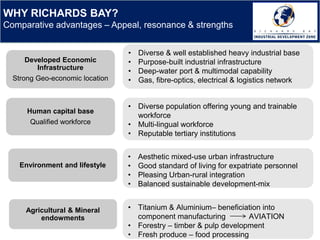

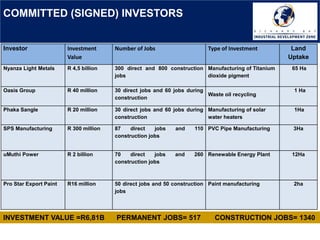

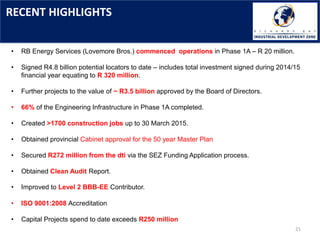

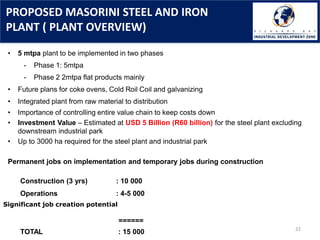

The Richards Bay Industrial Development Zone provides economic opportunities in metals beneficiation, agro-processing, port operations, renewable energy, and ICT. It has an existing land portfolio of 237 hectares and plans to expand into additional zones identified through a 50-year master plan. Recent highlights include signing investment agreements totaling R4.8 billion and creating over 1,700 construction jobs. The zone aims to attract further investments in steel production, oil and gas infrastructure, and shipbuilding through initiatives like Operation Phakisa. It also signed a memorandum of understanding with a technical college to develop workforce skills.