Monthly Economic Monitoring of Ukraine No 231, April 2024

Retrospective view on nigeria mrc

1. CDL Research

1 August 5, 2013 Mortgage Refinancing Report

Are the odds against the proposed Nigeria Mortgage

Refinance Company (MRC)?

Overview: The housing deficit in Nigeria is largely estimated to be around 16-18m units and

grows by about 2m units yearly; with the worth of this shortfall valued at about N25 trillion. The

twin issues of finance and the Land Use Act - an obnoxious statute from the military regime

which vests ultimate title for lands on the state governments represent major constraints to

meeting the housing needs of Nigeria. In tackling the issue of finance, the Central Bank of

Nigeria (CBN) recently released a framework for the establishment of a Mortgage Refinance

Company (MRC). The MRC is being established to provide short-term liquidity and/or medium-

to long-term funding or guarantees to housing finance lenders. It is expected to increase annual

mortgage origination in Nigeria to 200,000 from the current average of 20,000 mortgages within

the next few years, representing an increase of 900%.

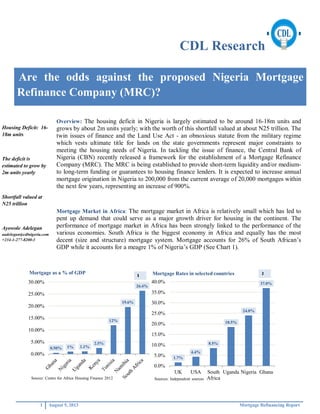

Mortgage Market in Africa: The mortgage market in Africa is relatively small which has led to

pent up demand that could serve as a major growth driver for housing in the continent. The

performance of mortgage market in Africa has been strongly linked to the performance of the

various economies. South Africa is the biggest economy in Africa and equally has the most

decent (size and structure) mortgage system. Mortgage accounts for 26% of South African s

GDP while it accounts for a meagre 1% of Nigeria s GDP (See Chart 1).

0.50% 1% 1.1%

2.5%

12%

19.6%

26.4%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Mortgage as a % of GDP

Source: Centre for Africa Housing Finance 2012

1.7%

4.4%

8.5%

18.5%

24.0%

37.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

UK USA South

Africa

Uganda Nigeria Ghana

Mortgage Rates in selected countries

Sources: Independent sources

Housing Deficit: 16-

18m units

The deficit is

estimated to grow by

2m units yearly

Shortfall valued at

N25 trillion

Ayowole Adelegan

aadelegan@cdlnigeria.com

+234-1-277-8200-3

2. CDL Research

2 August 5, 2013 Mortgage Refinancing Report

Nigeria which is sub-Sahara Africa s largest economy after South Africa has struggled to deliver

housing to the population because of the high prices of the homes in the market. This constricts

demand for housing in the country while also exposing mortgage finance institutions (MFIs) to

increased risk of default as mortgages are priced at unhealthy double digit rates. Across the

continent home financing has become largely accessible by mainly the upper class and the upper

middle class. This can be traced in large part to the preference of the mortgage lenders for mainly

corporate clients while individuals are left to access mortgage finance at exploitative rates (See

Chart 2).

World View of Mortgage Financing:

The gap created by housing is pertinent to many countries and has formed the basis of adoption

of a number of models in meeting this need. The models include Securitization of cash flow

(Freddie Mac in the United State), Portfolio Lender (Nationwide Building Society in the United

Kingdom) and Mortgage Refinancing Facility (Tanzania Mortgage Refinancing Company). A

diagrammatic representation of the models is given below:

Cash Flow Securitization Model:

Cash Cash Cash

Mortgage Mortgage Mortgage

Source: Economic Research Forum (ERF)

Portfolio Lender Model: Cash

Cash Deposit

Mortgage Cash

Debt

Source: Economic Research Forum (ERF)

Borrower Mortgage

Banker

Freddie

Mac

Capital

Market

Borrower

Nationwide

Building

Society

Deposit

Market

Capital

Market

3. CDL Research

3 August 5, 2013 Mortgage Refinancing Report

Refinancing Facility Model:

Cash

Cash Deposit

Mortgage Cash Cash

Collaterized debt Deposit

Source: Economic Research Forum

Estimating the Impact:

The capital market is positioned as a common terminator of the activities of the models under

review. The development of the capital market has become one of the foremost impacts of a

well-developed mortgage system. Increased housing needs and the presence of a well-established

system of meeting the housing needs create a huge capital gap. The mechanism of the capital

market provides an important opportunity in closing this gap and to a huge extent has led to the

development of the fundamentals associated with countries with strong mortgage systems (See

chart 3). In addition, growth in the mortgage/housing sector vis-à-vis construction is a vital

means of generating employment and has played pivotal role in enhancing productivity of the

populace in countries with a sound mortgage model (See chart 4).

Despite a relatively strong mortgage system in South Africa compared to other African countries,

the rate of unemployment is quite contradictory which may suggest the impact of other

underlying factors on the economy.

$0.015b $0.056b

$0.61b

$3.01b

$18.7b

14,000

2,014,000

4,014,000

6,014,000

8,014,000

10,014,000

12,014,000

14,014,000

16,014,000

18,014,000

20,014,000

Kenya Nigeria South

Africa

UK United

States

USDMillions

Stock Market Capitalization

Source: World Bank 2012

7.6% 7.7%

10.7% 11.0%

23.9%

25.2%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Unemployment Rate %

Sources: Independent Sources

3 4

Borrower Bank or

Savings

Loans

Deposit

Market

TMRC

Capital

Market

4. CDL Research

4 August 5, 2013 Mortgage Refinancing Report

A retrospective view on the Nigeria MRC:

The MRC is being set up to support mortgage originators such as Primary Mortgage Banks

(PMBs) and Deposit Money Banks (DMBs) to increase mortgage lending by refinancing their

mortgage loan portfolios. Its main focus is to act as intermediary between originators of

mortgage loans and the capital market who are typically looking for long-dated high quality

securities. The operations of the MRC are expected to enhance the development of the secondary

mortgage market which till date remains largely untapped. Already the World Bank has

committed $300 million of zero interest fund to the project while other local investors have

equally shown optimism. Recently Resort Savings and Loans, a primary mortgage lender says it

would commit N200 million to the proposed MRC.

The implication of these commitments and other interests is increased funding to the

mortgage/housing sector. Our prognosis also indicates there will be a need to access funds from

the capital market if the PMBs and DMBs can pull together more mortgage originations. To a

large extent, this may help to deal with one of the twin issues confronting a viable mortgage

system in Nigeria.

We think the impact of the existing land use act may constrict potential gains that would accrue

from the establishment of the mortgage refinancing mechanism. The Nigerian Land Use Decree

of 1978 nationalised all land in the country and notionally handed over its administration to

committees constituted at state and local government level and these constitute a huge constraint

to business (See Chart 5). This limitation would have to be removed if the level of investments

desired in the housing sector is to be attained.

Source: World Bank 2012

0

50

100

150

200

Senegal Angola Nigeria South Africa Namibia

122

184

82

23

39

20.3

3.2

20.8

5.6 13.7

6 7 13 6 7

Registering a property

No of Days Cost(% of property) Nos of procedures

5. CDL Research

5 August 5, 2013 Mortgage Refinancing Report

Furthermore, there will be a need for institutional and regulatory checks on the operations of the

DMBs and PMBs and their relationships with the Nigerian MRC. The MRC is being positioned

to serve as an off-taker of the loans disbursed by the mortgage lenders. There is a tendency for

DMBs & PMBs to create low quality mortgage risk assets and expect same to be offset by the

MRC which may lead to the US-styled mortgage bust that resulted in what has been described as

the worst economic crash since the 1930s depression. The global economy is yet to fully recover

from this subprime mortgage crisis.

It is equally being anticipated that interest rate on mortgage from lenders to home owners

(borrowers) will be cut by 50% from the present 24% to 12%. However, we think this may not

necessarily translate to affordable housing for the huge low-income population that are the most

affected in Nigeria s housing problems. Also, there have been no comprehensive plans on what

would happen to the entities traditionally entrusted to coordinate mortgage activities in Nigeria.

These are the Federal Housing Authority (FHA), National Housing Fund (NHF) and Federal

Mortgage Bank of Nigeria (FMBN). We think a clear blue-print has to be established on the

operations of the three entities.

Lastly, the operation of the MRC is set to increase activities in the Nigerian capital markets. We

anticipate an increase in the number of Real Estate Investment Trusts (REIT) traded on the

Nigerian bourse from the three names which are Union Homes, Skye Shelter Fund and UPDC

Plc. REITs are pooled capital of investors used to purchase and manage income property and/or

mortgage loans. In addition to REITs, we anticipate the increased creation of financial

derivatives as mortgage-funding needs increase and the market deepens. The proposed N60

billion bond to be issued by MRC confirms our expectation of the impact of the MRC on the

Nigerian bond market.

Barring any predatory and hawkish tendencies of Nigerian entrepreneurs, we expect a

considerable success of the MRC in Nigeria.

MRC could open

a new vista in the

Nigerian capital

market

Land Use Act:

The Achilles

Heels of housing

in Nigeria

World Bank

commits $300m

of zero interest

fund to the

Nigeria MRC

6. CDL Research

6 August 5, 2013 Mortgage Refinancing Report

Notes:

CBN: Mortgage Refinancing Company (MRC) Draft

World Bank Ease of Doing Business 2012

Nigerian Stock Exchange