Downloaded 18 times

![Reinstatement strategy: philosophy, theory, and practice (Richard Hartigan)

5 2 March 2017

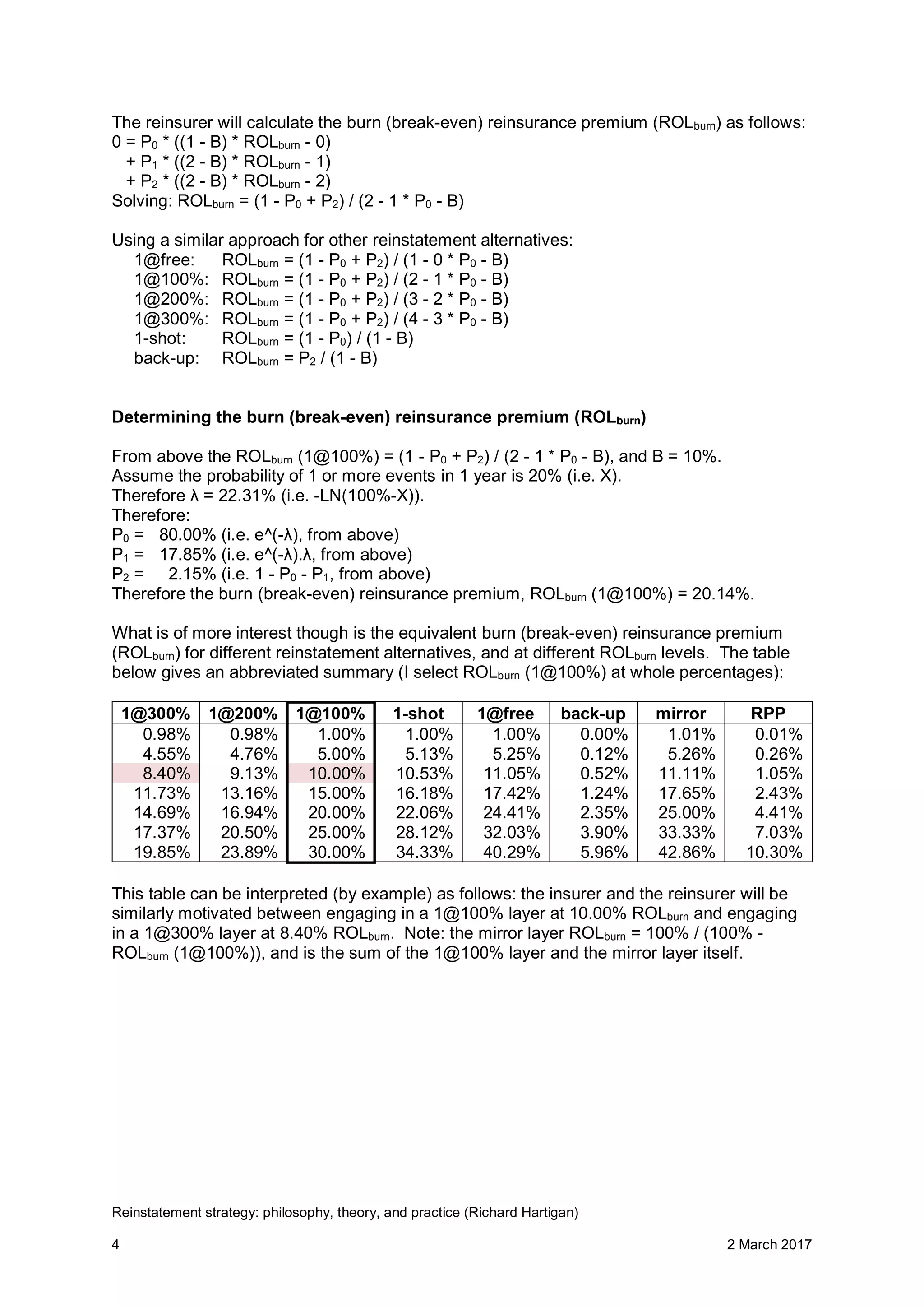

As an aside, one can see (subject to minor rounding errors):

1@free = 1-shot + back-up; and

1@free = 1@100% + RPP (where RPP = 1@100% * 1-shot)

= 1@100% (1 + 1-shot)

Proof (formulae on Page 4):

1@free: ROLburn = (1 - P0 + P2) / (1 - 0 * P0 - B) = (1 - P0 + P2) / (1 - B)

1@100%: ROLburn = (1 - P0 + P2) / (2 - 1 * P0 - B) = (1 - P0 + P2) / (2 - P0 - B)

1-shot: ROLburn = (1 - P0) / (1 - B)

back-up: ROLburn = P2 / (1 - B)

1-shot + back-up= (1 - P0) / (1 - B) + P2 / (1 - B) = (1 - P0 + P2) / (1 - B) = 1@free

1@100% + RPP = 1@100% (1 + 1-shot)

= (1 - P0 + P2) / (2 - P0 - B) * [1 + (1 - P0) / (1 - B)]

= (1 - P0 + P2) / (2 - P0 - B) * [(1 - B + 1 - P0) / (1 - B)]

= (1 - P0 + P2) / (2 - P0 - B) * [(2 - P0 - B) / (1 - B)]

= (1 - P0 + P2) / (1 - B)

= 1@free

Determining the gross (loaded) reinsurance premium (ROLgross)

The reinsurer is naturally profit-seeking. The above ROLburn figures need to be loaded.

Each reinsurer will have their own method for doing so, and therefore I must choose a

simple and sensible method. I simply add the square root of the burn (break-even)

reinsurance premium (ROLburn). For example: the square root of 15% is 3.87%, and

therefore the gross (loaded) reinsurance premium (ROLgross) would be 18.87%. This method

results in sensible expected reinsurance recovery rates (expected total reinsurance

recoveries / expected total reinsurance premium), both by reinstatement alternative and by

ROLgross level.

The table below gives an abbreviated summary (I re-select ROLgross (1@100%) at whole

percentages):

1@300% 1@200% 1@100% 1-shot 1@free back-up mirror RPP

0.99% 0.99% 1.00% 1.00% 1.00% 0.03% 1.01% 0.04%

4.74% 4.86% 5.00% 5.06% 5.12% 0.27% 5.26% 0.43%

8.92% 9.42% 10.00% 10.33% 10.64% 0.78% 11.11% 1.30%

12.59% 13.68% 15.00% 15.82% 16.63% 1.55% 17.65% 2.62%

15.86% 17.67% 20.00% 21.51% 23.11% 2.63% 25.00% 4.44%

18.82% 21.44% 25.00% 27.38% 30.11% 4.05% 33.33% 6.78%

21.54% 25.02% 30.00% 33.43% 37.69% 5.88% 42.86% 9.68%

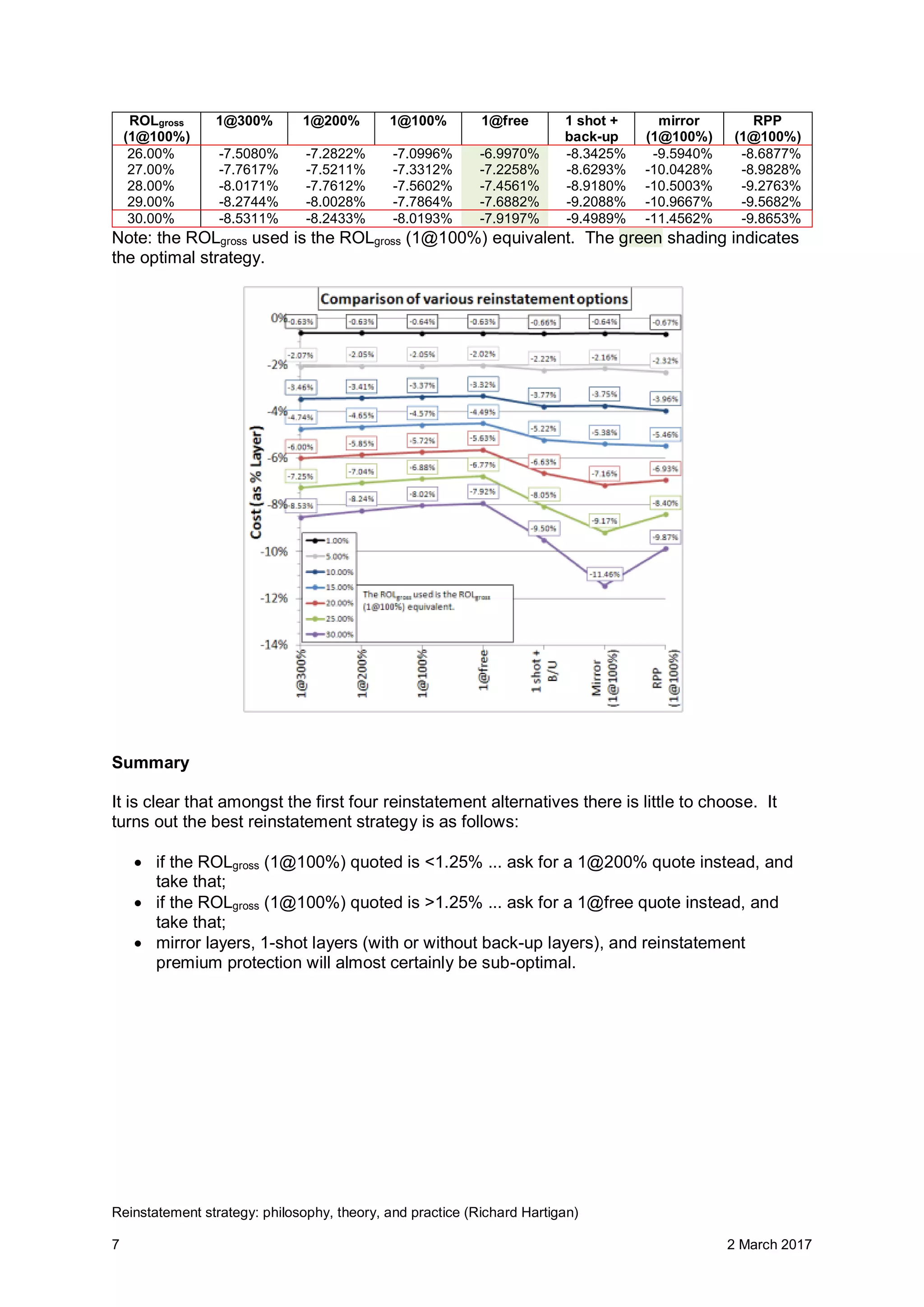

This table can be interpreted (by example) as follows: the insurer and the reinsurer will be

similarly motivated between engaging in a 1@100% layer at 10.00% ROLgross and engaging

in a 1@300% layer at 8.92% ROLgross. Note: the mirror layer ROLgross = 100% / (100% -

ROLgross (1@100%)), and is the sum of the 1@100% layer and the mirror layer itself.](https://image.slidesharecdn.com/reinsurancereinstatementpremiumsv2-170303075301/75/Reinstatement-strategy-philosophy-theory-and-practice-5-2048.jpg)

This paper analyzes optimal reinstatement strategies for short-tail excess of loss reinsurance programs, highlighting that mirror layers and certain reinstatement premium protections are often sub-optimal. It examines the impact of reinstatement alternatives, the calculation of break-even reinsurance premiums, and compares various strategies based on their effectiveness and costs. The findings aim to provide a clearer understanding of how to structure reinsurance in a manner that aligns motivation between insurers and reinsurers.