Downloaded 28 times

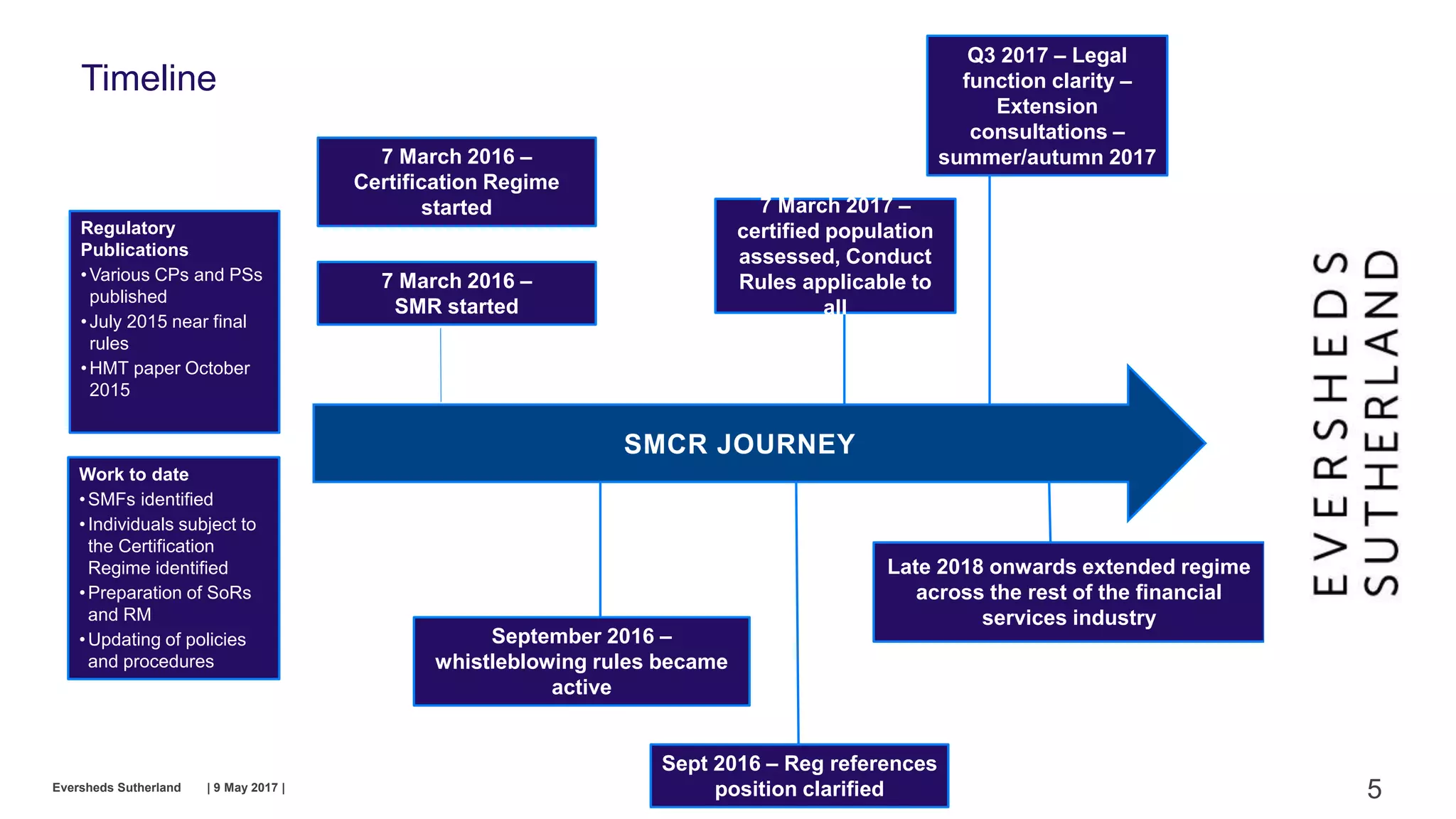

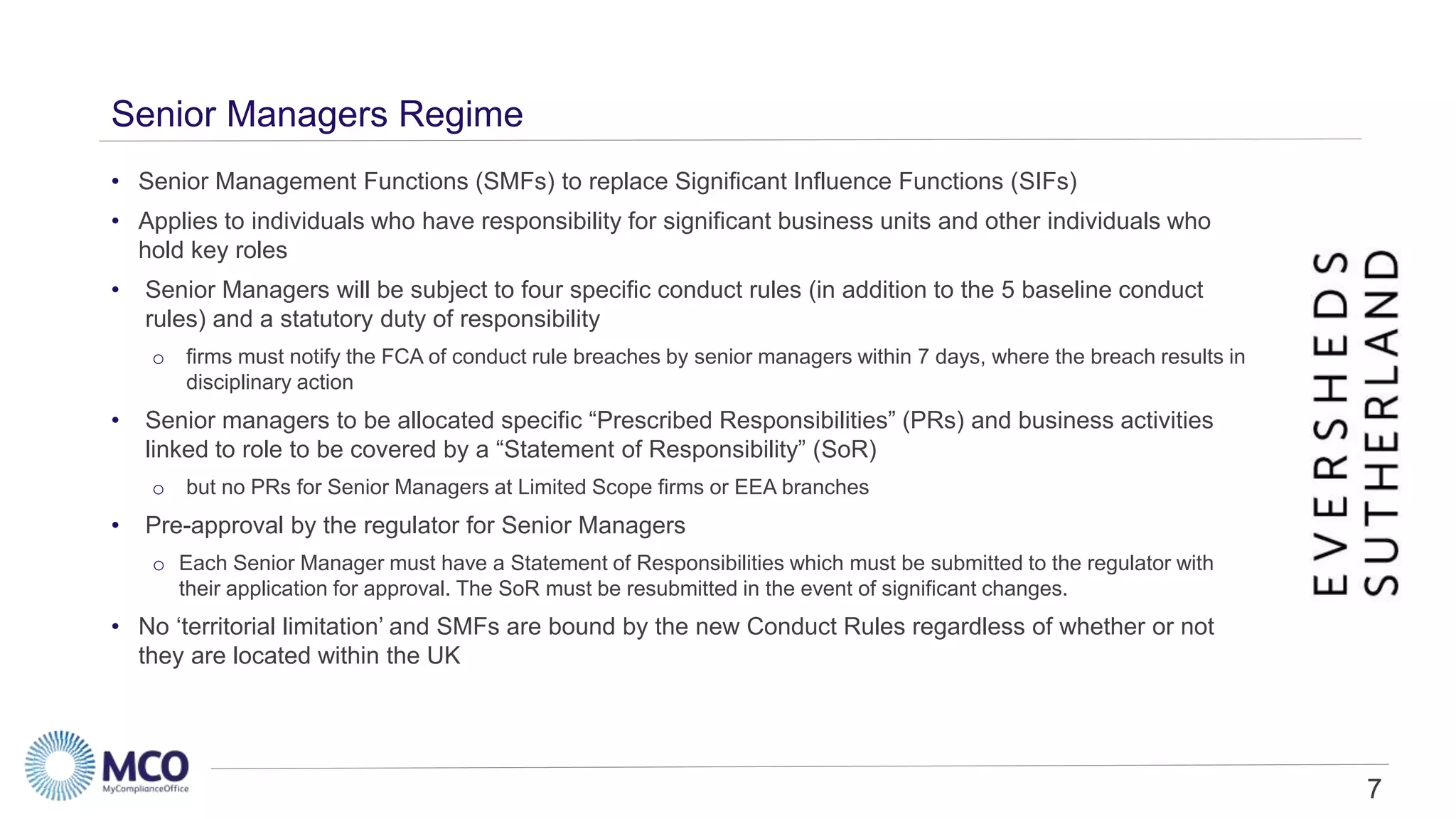

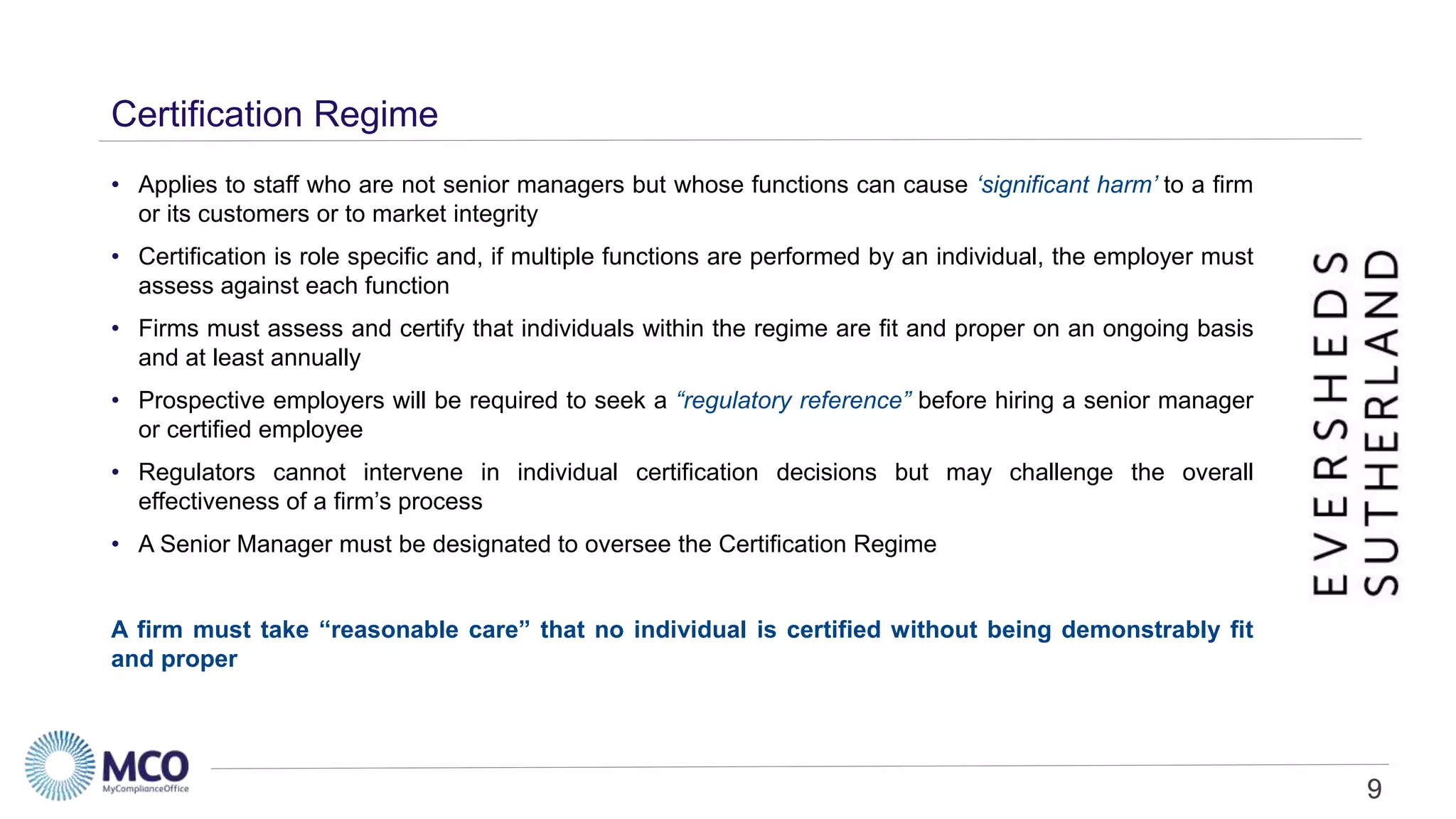

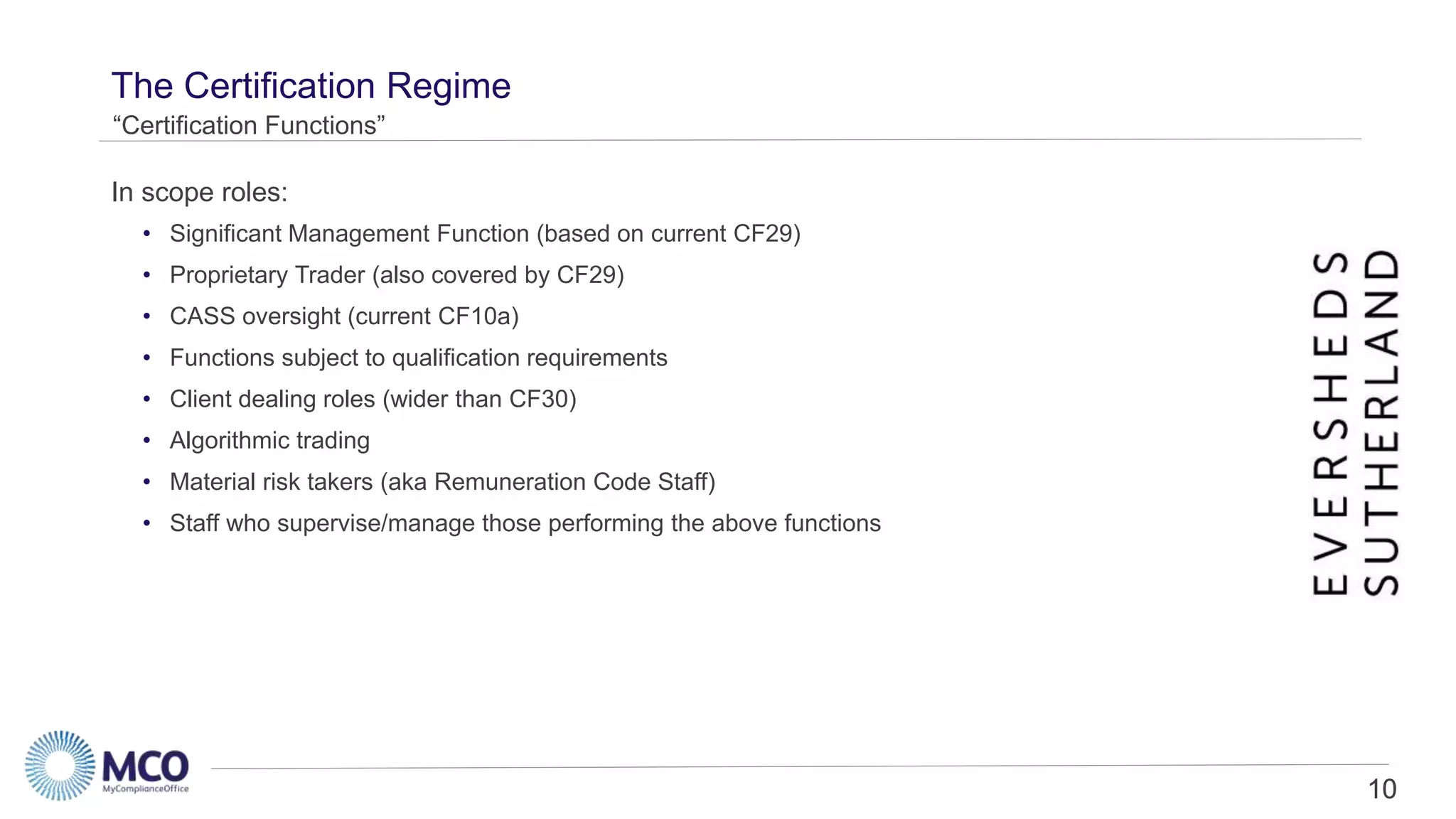

The document provides an overview of the new Senior Managers and Certification Regime and Conduct Rules that will extend individual accountability across the UK financial services industry. Key points: - The new regime aims to increase personal responsibility of senior individuals through prescribed responsibilities, conduct rules, and regulatory references. - Senior managers will be subject to specific conduct rules and responsibilities. Other individuals whose roles could significantly harm the firm are subject to annual certification. - All staff except ancillary workers must follow new conduct rules focused on integrity, skill/care, cooperation, customer interests, and market conduct. Senior managers have four additional rules. - Firms must have processes to assess individuals' fitness and propriety and provide regulatory