Download to read offline

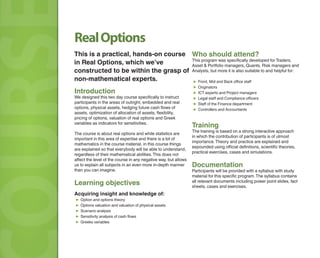

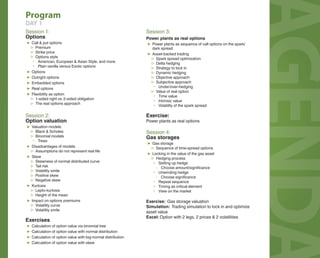

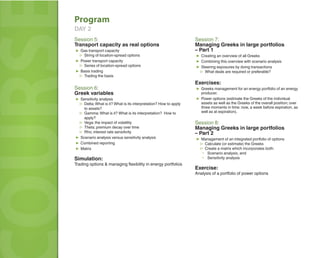

This document outlines a hands-on course on real options, scheduled for September 24-25, 2015, in Amsterdam, led by Jerry de Leeuw. The course aims to educate non-mathematical professionals on various aspects of real options, including valuation, sensitivity analysis, and practical applications in energy markets. Participants will receive comprehensive materials and engage in interactive learning, suitable for traders, risk managers, and other finance professionals.