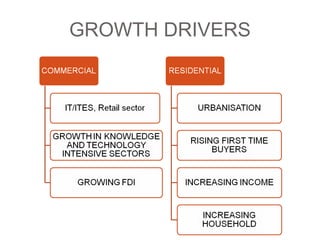

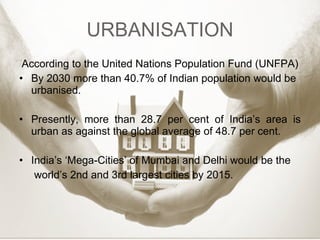

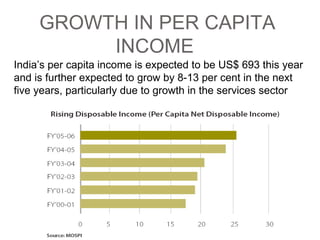

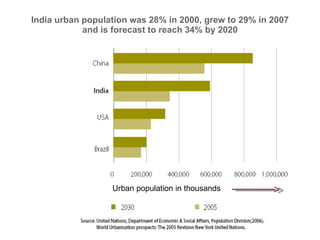

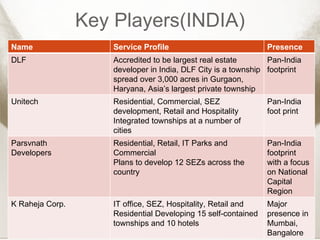

This document discusses the Indian real estate industry. It notes that the industry is the second largest employer in India after agriculture, growing at 30% annually and contributing 5% to India's GDP. Key drivers of growth are increasing urbanization as India's population becomes more urban, and rising per capita incomes. The document also compares India to China in terms of real estate investment and development. It outlines some of the major players in India's real estate market and their areas of focus. Finally, it presents a vision for what the industry may look like in 2020 with a focus on infrastructure, affordable housing, sustainability, and streamlined processes.