1. Sector update 2010 Q3

12 November 2010

Analyst: Einar Kilde Evensen

+47 2294 8232

einar.kilde.evensen@dnbnor.no

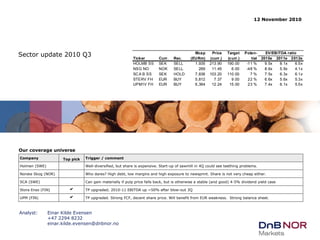

Company Top pick Trigger / comment

Holmen (SWE)

Norske Skog (NOR) Who dares? High debt, low margins and high exposure to newsprint. Share is not very cheap either.

SCA (SWE) Can gain materially if pulp price falls back, but is otherwise a stable (and good) 4-5% dividend yield case

b

b

Well-diversified, but share is expensive. Start-up of sawmill in 4Q could see teething problems.

TP upgraded; 2010-11 EBITDA up ~50% after blow-out 3Q

TP upgraded. Strong FCF, decent share price. Will benefit from EUR weakness. Strong balance sheet.

Stora Enso (FIN)

UPM (FIN)

Our coverage universe

Mcap Price Target Poten- EV/EBITDA ratio

Ticker Curr. Rec. (EURm) (curr.) (curr.) tial 2010e 2011e 2012e

HOLMB SS SEK SELL 1,935 213.90 190.00 -11 % 9.5x 8.1x 6.5x

NSG NO NOK SELL 269 11.45 6.00 -48 % 8.6x 5.9x 4.1x

SCA B SS SEK HOLD 7,836 103.20 110.00 7 % 7.5x 6.3x 6.1x

STERV FH EUR BUY 5,812 7.37 9.00 22 % 6.6x 5.6x 5.3x

UPM1V FH EUR BUY 6,364 12.24 15.00 23 % 7.4x 6.1x 5.5x

2. 2

Sector update

12 November 2010

PULP AND PAPER SECTOR

Paper 3Q 2010 update

What's new 2010 third quarter Pulp & Paper update

Holmen recommendation reduced to Sell (PT unchanged at SEK 190)

NSG reiterated at Sell, NOK 6.00

SCA reiterated at Hold, SEK 110.00

Stora Enso reiterated at Buy, with PT up to EUR 9.00 from EUR 7.00

UPM reiterated at Buy, with PT up to EUR 15.00 from EUR 13.00

Our assessment 1: Newsprint "bull story" of rising 2011 prices is over. It's all over.

The market already expects and has to a large extent discounted NP price

increases in Europe next year of 10%-15%.

European newsprint demand is in structural decline, implying deteriorating

market conditions for 2012 and forward

Investors should avoid NSG and also Holmen who have the highest exposure

to European newsprint (Holmen is also positively exposed to packaging).

Investment conclusion Pair trades recommended

Short Holmen: Trading near historically high multiples. Startup of new SEK 1.1bn

Braviken sawmill in 4Q may have teething problems

Short NSG (if possible): Bullish story on 2011 NP prices is discounted.

Long Stora Enso: Lowest EV/EBITDA multiple, best exposure (packaging)

Long UPM: Lowest EV/EBITDA multiple, strong balance sheet

2: Packaging is the place to be

Market is growing, but with stable prices. If the general economy and consumer

spending remain fair, packaging should be an attractive growth market.

3. 3

Sector update

12 November 2010

PULP AND PAPER SECTOR

3Q roundup: Publication paper disappointed; Pulp and packaging better

Sales EBIT

Company Reported vs DNM vs cons. Reported vs DNM vs cons.

Holmen

Holmen Paper 1,982 -4 % -3 % -129 6 % 10 % On par

Iggesund Paperboard 1,225 0 % 1 % 243 12 % 23 % Better

Holmen Timber 162 2 % - 8 -49 % n.a. Worse

Holmen Skog 1,281 8 % 7 % 212 21 % 27 % Better

Holmen Energi 419 9 % - 96 50 % n.a. Better

Norske Skog

Newsprint Europe 1,374 1 % - -174 -107 % -40 % Worse

Newsprint Ex-Europe 1,495 12 % - 153 220 % 3 % Better

Magazine 1,606 3 % - -90 n.m. -100 % Worse

SCA

Personal Care 6,125 -6 % -5 % 697 -7 % -5 % Worse

Tissue 9,924 -5 % -3 % 753 -14 % -6 % Worse

Packaging 7,392 1 % -2 % 512 47 % 20 % Better

Forest Products 4,415 3 % 2 % 685 -1 % -7 %

Publication Products 2,131 -1 % - -38 n.m. n.a. On par

Pulp, Timber & Wood 2,284 8 % - 723 8 % n.a. Better Better

Stora Enso

Newsprint and Book Paper 323 -0 % -0 % 0 n.m. n.m. On par

Magazine Paper 541 3 % -1 % 46 79 % 69 % Better

Fine Paper 563 7 % 5 % 71 38 % 16 % Better

Consumer Board 594 -2 % 3 % 78 -4 % 21 % On par

Industrial Packaging 225 -12 % -9 % 19 158 % 25 % Better

UPM

Energy 124 4 % 3 % 44 12 % 17 % Better

Pulp 489 10 % 8 % 199 38 % 24 % Better

Forest and Timber 387 5 % 7 % 68 107 % 331 % Better

Paper 1,672 7 % 2 % -64 -195 % -228 % Worse

Label 284 3 % 3 % 24 13 % 17 % Better

Better 2 of 8 3 of 4 2 of 4 2 of 2 3 of 4 2 of 2

On par 3 of 8 1 of 4 - - - -

Worse 3 of 8 - 2 of 4 - 1 of 4 -

* Note: ''On par'' if reported within +/- 5 % range of estimates

Wood &

forest Energy

Publ.

paper

Board &

pack.

Other

paper Pulp

Apart from SCA's

disappointments in

Personal Care and Tissue,

the main disappointments

came within Publication

paper

0

1

2

3

4

5

6

7

8

9

Publ.

paper

Board &

pack.

Other

paper

Pulp Wood &

forest

Worse

On par

Better

4. 4

Sector update

12 November 2010

PULP AND PAPER SECTOR

Agenda

Case: Newsprint

Other key considerations

Valuation

3Q updates and changes of estimates

Appendix

5. 5

Sector update

12 November 2010

PULP AND PAPER SECTOR

The subject of this update

The end of newsprint (as we know it)?

Newsprint is continuously losing advertising market share

Newsprint's key strengths

"Coffee table effect". Multiple readers per paper

Media choice #1 for baby boomers

Purchaser "owns" newspaper

Local

Portability

Newsprint's key weaknesses

Distribution

Heavily dependent upon advertising from real estate, employment

and autos

Declining circulation and subscription

7. 7

Sector update

12 November 2010

PULP AND PAPER SECTOR

An analogy to newspaper as media habits change: Blockbuster Inc.

Blockbuster Inc. facts

First store opened in Dallas,

TX, 1985

IPO in 1999, for USD 560m

5,000 stores in US (Jan 2010)

Peaks

Share price: April 2002, at USD

30 (Market cap: USD 5,300m)

Yearly revenues: 2004, at USD

6,053m

EBIT margin: 2003, at 8%

NIBD: 2005, at USD 882m

BUST

8. 8

Sector update

12 November 2010

PULP AND PAPER SECTOR

Blockbuster is now bust (no pun intended)

Blockbuster Inc filed for

Chapter 11 in September

2010

We believe newsprint is a structural

sunset industry, just like video rental

(with physical stores), and LPs, music

cassettes and CDs.

There will be niche markets, but market

demand is going to continue falling.

9. 9

Sector update

12 November 2010

PULP AND PAPER SECTOR

What's going on with New York Times?

Arthur Sulzberger Jr, CoB of NYT Co.

We will stop

printing the

New York Times

some time in

the future.

(Sept 2010)

Our print

product is alive

and well

(Sept 2010)

Janet Robinson, CEO of NYT

New York Times facts

Published since 1851

Has won 104 Pulitzer prizes,

more than any other media

Current circulation: 950', down

>10% from peak

First major newspaper to

launch iPod/iPhone application

in 2008

Third largest newspaper in US

after WSJ and USA Today

Question:

Will this newspaper bellwether

also be the first to stop printing

on paper?

10. 10

Sector update

12 November 2010

PULP AND PAPER SECTOR

Newsprint demand is falling – North America leads

US demand is now less

than half what it was in

2000.

-51%

-10%

11. 11

Sector update

12 November 2010

PULP AND PAPER SECTOR

Which are the companies most exposed to Newsprint?

Norske Skog most exposed

Newsprint: >50% of revenue (but ~50/50 split Europe vs ex-Europe)

Magazine: ~40% (all in Europe, and ~50/50 split SC/LWC)

Holmen

Significant SC exposure

Note: Magazine grades: SC = ''Un-coated''; LWC = ''Light-weight''; CWF = ''Heavy''

Implicit revenue exposure to paper grades

-

10%

20%

30%

40%

50%

60%

Un-coated Light-weight Heavy

Newsprint Magazine Office paper

Holmen NSG SCA Stora Enso UPM

13. 13

Sector update

12 November 2010

PULP AND PAPER SECTOR

0

20

40

60

80

100

120

140

160

180

02.01.2007

02.04.2007

02.07.2007

02.10.2007

02.01.2008

02.04.2008

02.07.2008

02.10.2008

02.01.2009

02.04.2009

02.07.2009

02.10.2009

02.01.2010

02.04.2010

02.07.2010

02.10.2010

EUR/tonne

OCC

ONP/OMG

But lower RP prices are a positive trigger

Recovered paper prices

-€20?

-€40?

-€60?

-€80??

NSG's 2011 EBITDA to

gain 12% if RP price falls

by EUR 20/tonne (year

average).

We currently do not

model major shifts in the

RP price, which to a large

extent is pulled by strong

demand from China/Asia

Implications from EUR -20/tonne lower RP price:

Exposure: NP RP Chg. cost Revenue Impact EBITDA EBITDA

Long (short) prod. exposure @ €-20/t 2011e (margin 2011e gain

Company (kt/year) (kt/year) (EUR m) (EUR m) impr.) (EUR m)

Holmen 825 -750 -15 1,833 0.8 % 304 5 %

NSG 2,945 -1,300 -26 2,336 1.1 % 213 12 %

SCA 375 -3,800 -76 11,800 0.6 % 1,867 4 %

Stora Enso 2,650 -2,400 -48 10,197 0.5 % 1,451 3 %

UPM 2,090 -3,000 -60 8,900 0.7 % 1,572 4 %

14. 14

Sector update

12 November 2010

PULP AND PAPER SECTOR

Agenda

Case: Newsprint

Other key considerations

Valuation

3Q updates and changes of estimates

Appendix

17. 17

Sector update

12 November 2010

PULP AND PAPER SECTOR

Per end-3Q 2010

EURm Undrawn Funds* / Maturities Average

Company Cash facilites debts 2010e 2011e 2012e Later maturity

Holmen 12 792 117 % 210 63 44 368 2.4

Norske Skog 552 - 33 % 12 266 483 896 5.1

SCA - 3,306 77 % 1,007 972 175 2,155 2.8

Stora Enso 1,121 1,400 69 % 190 650 140 2,700 5.6

UPM 484 1,200 44 % 180 400 1,030 2,180 5.4

Exchange rates used: EURSEK 9.295, EURNOK 8.078

Assuming even spread of maturities over each calendar year

* Cash + undrawn facilities

Maturities: Holmen and SCA have the most solid balances; Stora Enso

and UPM the longest maturities

x

!b

Best:

• Holmen, Stora Enso

Worst:

• Norske Skog – critical

for 2012

x

18. 18

Sector update

12 November 2010

PULP AND PAPER SECTOR

Pulp price seems to have peaked, at 66% over the trough in April 2009

Lower pulp price will help

Norske Skog through

lower costs on magazine

paper production (not

newsprint).

NBSK Europe is down 2%

from the peak in July

2010, which was 7%

above the previous peak

in June 2008

Pulp markets remain

tight due to the absence

of shipments from Chile

and Indonesia as well as

the gradual improvement

in paper demand and

production in Europe

Stora Enso and UPM are

net producers of pulp,

while the rest are net

buyers, SCA being the

largest

0

200

400

600

800

1,000

1,200

03.12.1996

03.12.1997

03.12.1998

03.12.1999

03.12.2000

03.12.2001

03.12.2002

03.12.2003

03.12.2004

03.12.2005

03.12.2006

03.12.2007

03.12.2008

03.12.2009

USD/tonne

-

10

20

30

40

50

60

days

Inventories (right)

NBSK US

NBSK Europe

19. 19

Sector update

12 November 2010

PULP AND PAPER SECTOR

NP prices are higher in US than in Europe by a margin of 7%

It costs EUR 40-50/tonne

to ship newsprint across

the Atlantic

Jan-Apr 2010 European

shipments are up 4% YoY

Announced NP closures in

Europe for 2010 amount

to 295kt or ~2.3% of

total capacity (~13mt),

while demand is up 4.1%

YoY first nine months.

Lower recovered paper

prices (ONP/OMG) will

help P&Ls (9% of NSG's

costs are RP!)

European shipments YTD

-800

-600

-400

-200

0

200

400

600

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

2006 2007 2008 2009 2010 2011

'000tonnes(yearlycapacity)

Volga JSC

UPM

Stora Enso

Solikamsky Pulp & Paper JSC

SCA

Perlen Papier

Papierfabrik Palm

Papeteries de Turckheim

Osnova

Norske Skog Industries

Matussière & Forest

Investlesprom Group

Holmen

Fabryka Papieru Myszków

Burgo Group

Belarus Government

AbitibiBowater

Category Graphic Grade NEWS Region Europe

Sum_Change

Year Q

Parent

European capacity closures 2006-2010

200

300

400

500

600

700

800

06-2001

12-2001

06-2002

12-2002

06-2003

12-2003

06-2004

12-2004

06-2005

12-2005

06-2006

12-2006

06-2007

12-2007

06-2008

12-2008

06-2009

12-2009

06-2010

EUR/tonne

300

350

400

450

500

550

600

650

700

750

800

USD/tonne

NP Europe (EUR)

NP N.Am (EUR)

NP N.Am (USD)

Diff: EUR 31 / ton

(7%)

-8,000

-4,000

0

4,000

8,000

12,000

jmmjsnjmmjsnjmmjsnjmmjsnjmmjsnjmmjsnjmmjsnjmmjs

2003 2004 2005 2006 2007 2008 20092010

'000tonnes

-20 %

-10 %

0 %

10 %

20 %

30 %

growth

YTD Shipments

Acc. YoY Growth

20. 20

Sector update

12 November 2010

PULP AND PAPER SECTOR

-300

-200

-100

0

100

200

300

400

500

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

2006 2007 2008 2009 2010

'000tonnes(yearlycapacity)

Vertaris

UPM

Stora Enso

Saber Paper

Papierfabrik Golzern

Papierfabrik am Neckar

Papeteries des Deux-Guiers

Papeteries des Alpes

Norske Skog Industries

Myllykoski

Matussière & Forest

JIP-Papirny

Holmen

Cartiere Paolo Pigna

Burgo Group

Arctic Paper

Category Graphic Grade UM Region Europe

Sum_Change

Year Q

Parent

-800

-700

-600

-500

-400

-300

-200

-100

0

100

200

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

2006 2007 2008 2009 2010

'000tonnes(yearlycapacity)

UPM

Stora Enso

Sappi Limited

Perlen Papier

Papierfabrik am Neckar

Myllykoski

Matussière & Forest

Kübler & Niethammer

Investlesprom Group

Holmen

Burgo Group

Category Graphic Grade CM Region Europe

Sum_Change

Year Q

Parent

Magazine paper: Picking up … slowly

Jan-Sept 2010 shipments

• SC: +2.0% YoY

• CM: +8.7% YoY

• CWF: +12.1% YoY

Announced 2010 capacity

growth:

• UM: -1.2% of cap.

• CM: +0.3% of cap.

• CWF: none

Largest exposures:

• UM: Holmen, NSG

• CM: NSG, UPM

• CWF: STERV, UPM

European UM capacity closures 2006-2010 European CM capacity closures 2006-2010

400

500

600

700

800

900

1,000

06-2001

11-2001

04-2002

09-2002

02-2003

07-2003

12-2003

05-2004

10-2004

03-2005

08-2005

01-2006

06-2006

11-2006

04-2007

09-2007

02-2008

07-2008

12-2008

05-2009

10-2009

03-2010

08-2010

EUR/tonne

CWF (heavy, coated mag. paper)

LWC (lightweight coated mag. paper)

21. 21

Sector update

12 November 2010

PULP AND PAPER SECTOR

Packaging prices – peaking out already??

Largest exposures:

• Liner: SCA

• Fluting: only minor

• FBB: STERV, Holmen

0

100

200

300

400

500

600

700

13.01.2004

13.06.2004

13.11.2004

13.04.2005

13.09.2005

13.02.2006

13.07.2006

13.12.2006

13.05.2007

13.10.2007

13.03.2008

13.08.2008

13.01.2009

13.06.2009

13.11.2009

13.04.2010

13.09.2010

EUR/tonne

Testliner P

Kraftliner

RB fluting

22. 22

Sector update

12 November 2010

PULP AND PAPER SECTOR

Agenda

Case: Newsprint

Other key considerations

Valuation

3Q updates and changes of estimates

Appendix

23. 23

Sector update

12 November 2010

PULP AND PAPER SECTOR

STERV and UPM have the lowest EV/EBITDAs in the group*, and are also

the cheapest vs own history

Holmen vs rebased peers from jan 1999

Rebased to price per 15.01.1999

#REF!

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

9.0x

10.0x

11.0x

jan99

jul99

jan00

jul00

jan01

jul01

jan02

jul02

jan03

jul03

jan04

jul04

jan05

jul05

jan06

jul06

jan07

jul07

jan08

jul08

jan09

jul09

jan10

jul10

EV/EBITDA

Holmen Norske Skog SCA Stora Enso UPM

EV/EBITDA observation summary

Last, Average

Company 10.11.10 2 year 5 year

Holmen 7.5x 8.3x 7.9x

Norske Skog 5.7x 6.2x 6.4x

SCA 6.1x 6.4x 6.6x

Stora Enso 5.9x 7.3x 6.9x

UPM 5.9x 6.7x 6.8x

Median 5.9x 6.7x 6.8x

Last vs average

Company 2 year 5 year

Holmen 91 % 95 %

Norske Skog 93 % 89 %

SCA 95 % 92 %

Stora Enso 81 % 86 %

UPM 87 % 86 %

Median 91 % 89 %

* Except Norske Skog

27. 27

Sector update

12 November 2010

PULP AND PAPER SECTOR

Agenda

Case: Newsprint

Key considerations

Valuation

3Q updates and changes of estimates

Appendix

28. 28

Sector update

12 November 2010

PULP AND PAPER SECTOR

Changes to estimates and recommendations

Main changes

• Norske Skog PT down

from NOK 8 to NOK 7

• Stora Enso PT down

from EUR 5.00 to EUR

4.60, recommendation

changed from Sell to

Hold

Revenue

(million) New estimates Old estimates Change

Company Curr. 2010 2011 2012 2010 2011 2012 2010 2011 2012

Holmen SEK 17,067 18,067 18,894 17,200 18,317 19,199 -133 -250 -305

Norske Skog NOK 18,848 19,493 19,884 18,382 18,491 18,777 466 1,002 1,107

SCA NOK 109,891 113,489 115,217 110,993 114,207 115,984 -1,102 -718 -767

Stora Enso € 10,211 9,703 9,618 9,106 8,647 8,536 1,105 1,056 1,081

UPM € 8,900 8,904 8,923 8,791 8,766 8,787 109 138 136

EBITDA

(million) New estimates Old estimates Change

Company Curr. 2010 2011 2012 2010 2011 2012 2010 2011 2012

Holmen SEK 2,516 2,830 3,283 2,395 2,825 3,146 121 5 137

Norske Skog NOK 1,295 1,716 2,141 1,461 1,801 2,227 -166 -85 -86

SCA SEK 15,926 17,385 17,422 15,330 17,119 17,226 595 266 195

Stora Enso € 1,256 1,392 1,400 808 992 980 447 400 420

UPM € 1,411 1,572 1,587 1,268 1,357 1,792 143 215 -205

EPS adj.

New estimates Old estimates Change

Company Curr. 2010 2011 2012 2010 2011 2012 2010 2011 2012

Holmen SEK 8.42 11.50 15.98 7.58 11.28 14.66 0.84 0.22 1.32

Norske Skog NOK -3.21 -3.53 1.50 -2.54 -2.99 1.86 -0.67 -0.54 -0.36

SCA SEK 9.16 10.11 9.45 8.19 9.48 9.17 0.97 0.63 0.28

Stora Enso € 0.81 0.76 0.79 0.37 0.40 0.40 0.44 0.36 0.39

UPM € 0.85 1.01 1.08 0.70 0.81 1.34 0.15 0.20 -0.26

Recommendation changes

New Old Change

Company Rec. PT Rec. PT Rec. PT

Holmen SELL 190 HOLD 185 Downgrade + 5.00

Norske Skog SELL 6.00 SELL 6.00 - -

SCA HOLD 110 BUY 110 Downgrade -

Stora Enso BUY 9.00 BUY 7.00 - + 2.00

UPM BUY 15.00 BUY 13.00 - + 2.00

34. 34

Sector update

12 November 2010

PULP AND PAPER SECTOR

Agenda

Case: Newsprint

Key considerations

Valuation

3Q updates and changes of estimates

Appendix

35. 35

Sector update

12 November 2010

PULP AND PAPER SECTOR

P/B: Except NSG, the shares trade very close around 0.90-1.05x

Holmen vs rebased peers from nov 1994

Rebased to price per 18.11.1994

#REF!

-

0.25x

0.50x

0.75x

1.00x

1.25x

1.50x

1.75x

2.00x

nov94

nov95

nov96

nov97

nov98

nov99

nov00

nov01

nov02

nov03

nov04

nov05

nov06

nov07

nov08

nov09

P/B

Holmen Norske Skog SCA Stora Enso UPM

Average

Company

Last,

10.11.10 1 year

nov 94 -

nov 10

Holmen 1.05x 0.98x 1.17x

Norske Skog 0.24x 0.18x 0.77x

SCA 0.98x 0.97x 1.17x

Stora Enso 0.99x 0.88x 1.05x

UPM 0.90x 0.81x 1.10x

Average 0.83x 0.76x 1.05x

Last vs average

Company 1 year

nov 94 -

nov 10

Holmen 107 % 90 %

Norske Skog 134 % 31 %

SCA 101 % 84 %

Stora Enso 114 % 95 %

UPM 111 % 81 %

Average 113 % 76 %

36. 36

Sector update

12 November 2010

PULP AND PAPER SECTOR

5-yr CDS: NSG still considered most risky

0

200

400

600

800

1,000

1,200

1,400

1,600

12-2006

03-2007

06-2007

09-2007

12-2007

03-2008

06-2008

09-2008

12-2008

03-2009

06-2009

09-2009

12-2009

03-2010

06-2010

09-2010

basispoints

NSG

Stora Enso

UPM

SCA

M-real

Last, Average

Comp. 05.11.10 1 yr 5 yr

M-real 451 733 1,129

NSG 790 1,065 712

SCA 72 84 86

STERV 257 321 250

UPM 257 280 209

37. 37

Sector update

12 November 2010

PULP AND PAPER SECTOR

DISCLAIMER AND STATEMENT THAT AFFECTS YOUR RIGHTS

This report must be seen as marketing material unless the criteria for preparing investment research, according to the Norwegian Securities Trading Regulation 2007/06/29 no. 876, are met.

This report has been prepared by DnB NOR Markets, a division of DnB NOR Bank ASA. The report is based on information obtained from public sources that DnB NOR Markets believes to be

reliable but which DnB NOR Markets has not independently verified, and DnB NOR Markets makes no guarantee, representation or warranty as to its accuracy or completeness. Any opinions

expressed herein reflect DnB NOR Markets’ judgment at the time the report was prepared and are subject to change without notice. Confidentiality rules and internal rules restrict the exchange

of information between different parts of DnB NOR Markets/DnB NOR Bank ASA and this may prevent employees of DnB NOR Markets who are preparing this report from utilizing or being

aware of information available in DnB NOR Markets/DnB NOR Bank ASA which may be relevant to the recipients’ decisions. This report is not an offer to buy or sell any security or other

financial instrument or to participate in any investment strategy. No liability whatsoever is accepted for any direct or indirect (including consequential) loss or expense arising from the use of

this report. Distribution of research reports is in certain jurisdictions restricted by law. Persons in possession of this report should seek further guidance regarding such restrictions before

distributing this report. Please contact DnB NOR Markets at +47 22 94 82 72 for further information and inquiries regarding this report, such as ownership positions and publicly

available/commonly known corporate advisory performed by DnB NOR Markets etc, in relation to the Norwegian Securities Trading Act 2007/06/29 no. 75 and the Norwegian Securities Trading

Regulation 2007/06/29 no. 876. This report is for clients only, and not for publication, and has been prepared for information purposes only by DnB NOR Markets - a division of DnB NOR Bank

ASA registered in Norway number NO 984 851 006 (the Register of Business Enterprises) under supervision of the Financial Supervisory Authority of Norway (Finanstilsynet), Monetary

Authority of Singapore, and on a limited basis by the Financial Services Authority of UK. Information about DnB NOR Markets can be found at dnbnor.no.

Additional information for clients in Singapore: This report has been distributed by the Singapore branch of DnB NOR Bank ASA. It is intended for general circulation and does not take

into account the specific investment objectives, financial situation or particular needs of any particular person. You should seek advice from a financial adviser regarding the suitability of any

product referred to in this report, taking into account your specific financial objectives, financial situation or particular needs before making a commitment to purchase any such product.

Recipients of this report should note that, by virtue of their status as “accredited investors” or “expert investors”, the Singapore branch of DnB NOR Bank ASA will be exempt from complying

with certain compliance requirements under the Financial Advisers Act, Chapter 110 of Singapore (the “FAA”), the Financial Advisers Regulations and associated regulations there under. In

particular, it will be exempt from: - Section 27 of the FAA (which requires that there must be a reasonable basis for recom-mendations when making recommendations on investments). Please

contact the Singapore branch of DnB NOR Bank ASA at +65 6212 0753 in respect of any matters arising from, or in connection with, this report. We, the DnB NOR Group, our associates,

officers and/or employees may have interests in any products referred to in this report by acting in various roles including as distributor, holder of principal positions, adviser or lender. We, the

DnB NOR Group, our associates, officers and/or employees may receive fees, brokerage or commissions for acting in those capacities. In addition, we, the DnB NOR Group, our associates,

officers and/or employees may buy or sell products as principal or agent and may effect transactions which are not consistent with the information set out in this report. In the United

States: Each research analyst named on the front page of this research report, or at the beginning of any subsection hereof, hereby certifies that (i) the views expressed in this report

accurately reflect that research analyst’s personal views about the company and the securities that are the subject of this report; and (ii) no part of the research analyst’s compensation was,

is, or will be, directly or indirectly, related to the specific recommendations or views expressed by that research analyst in this report. This report is being furnished upon request and is

primarily intended for distribution to “Major U.S. Institutional Investors” within the meaning of Rule 15a-6 of the U.S. Securities and Exchange Commission under the Securities Exchange Act of

1934. To the extent that this report is being furnished, or will be disseminated, to non-Major U.S. Institutional Investors, such distribution is being made by DnB NOR Markets, Inc., a

separately incorporated subsidiary of DnB NOR that is a U.S. broker-dealer and a member of the Financial Industry Regulatory Authority and the Securities Investor Protection Corporation.

Any U.S. recipient of this report seeking to obtain additional information or to effect any transaction in any security discussed herein or any related instrument or investment should call or write

DnB NOR Markets, Inc., 200 Park Avenue, New York, NY 10166-0396, telephone number 212-681-3800 or fax 212-681-4119. In Canada: This email, and any materials attached with it, has

been distributed in reliance on the International Dealer Exemption pursuant to NI 31-103 subsection 8.18(2) and subsection 8.18(4)(b). Please be advised that: 1. DnB Nor Bank ASA (DnB

NOR Markets) and DnB NOR Markets, Inc. are not registered in Canada. 2. DnB Nor Bank ASA (DnB NOR Markets) and DnB NOR Markets, Inc's jurisdiction of residence is Norway and the

United States, respectively. 3. The name and address of the agent for service of process for DnB Nor Bank ASA (DnB NOR Markets) and DnB NOR Markets, Inc. in the local jurisdiction is:

Alberta: Blake, Cassels & Graydon LLP, Attention: Pat Finnerty/Ross Bentley, 855 – 2nd Street S.W., Suite 3500, Bankers Hall East Tower, Calgary, AB T2P 4J8. British Columbia: Blakes

Vancouver Services, Inc., 595 Burrard Street, P.O. Box 49314, Suite 2600, Three Bentall Centre, Vancouver, BC V7X 1L3. Labrador: Stewart McKelvey, Cabot Place, 100 New Gower Street,

Suite 1100, P.O. Box 5038, St. John’s, NL A1C 5V3. Manitoba: Aikins, MacAulay & Thorvaldson LLP, 30th Floor, Commodity Exchange Tower, 360 Main Street, Winnipeg, MB R3C 4G1.

Newfoundland: Stewart McKelvey, Cabot Place, 100 New Gower Street, Suite 1100, P.O. Box 5038, St. John’s, NL A1C 5V3. New Brunswick: Stewart McKelvey, 10th Floor, Brunswick House,

44 Chipman Hill, Saint John, NB E2L 4S6. Nova Scotia: Stewart McKelvey, Purdy’s Wharf Tower One, 1959 Upper Water Street, Suite 900, P.O. Box 997, Halifax, NS B3J 2X2. Ontario:

Blakes Extra-Provincial Services Inc., Suite 2800, 199 Bay Street, Toronto, Ontario M5L 1A9. Prince Edward Island: Stewart McKelvey, 65 Grafton Street, Box 2140, Charlottetown, PE C1A

8B9. Quebec: Services Blakes Quebec Inc., 600 de Maisonneuve Boulevard Ouest, Suite 2200, Tour KPMG, Montreal, QC H3A 3J2. Saskatchewan: MacPherson, Leslie & Tyerman LLP, 1500

Continental Bank Building, 1874 Scarth Street, Regina, SK S4P 4E9. Northwest Territories: Gerald Stang, Suite 201, 5120-49 Street, Yellowknife, NT X1A 1P8. Yukon: Grant Macdonald,

Macdonald & Company, Suite 200, Financial Plaza, 204 Lambert Street, Whitehorse, YK Y1A 3T2. Nunavut: Terry Gray, P.O. Box 1779, Building 1088C, Iqaluit, NU X0A0H0. 4. There may be

difficulty enforcing legal rights against DnB NOR Bank ASA (DnB NOR Markets) and DnB NOR Markets, Inc. because each is a resident outside of Canada and all or substantially all of their

assets may be situated outside of Canada.